US CREDIT UPDATE: MNI US CREDIT BDC/Alt Fins: Week in Review

MNI US BDC/Alt Fins: Week in Review

We saw two issuers this week - APODS 5Y and ATWALD 2Y and 7Y - both performed well in the secondary. We got a Q4 update from MAIN and Q4 positive earnings from BLK.

• Apollo Debt Solutions issued $750m in 5Y at +195 off a +220 IPT. Bonds rallied 5bps in the secondary. Atlas Warehouse Lending issued a tap of their 4.625%’28 at +100 off a +125 IPT and a new 7Y at +135 off and IPT of +160. The tap rallied 7bps from issuance and the 7Y rallied as much as 5bps.

• Main Street Capital Corp (MAIN) gave an update on NII/sh guidance that was higher than BBG consensus for Q4 results. MAIN reports on Feb 27.

• BLK Q4’25 earnings were a mild positive as they beat BBG consensus. Revenues/fees were higher in part due to acquisitions. AUM was up more than expected due to strong inflows, with equities and ETFs leading the way. Unadjusted margin was lower on expenses related to the Global Infrastructure acquisition. See our post here. https://www.mnimarkets.com/articles/blackrock-blk-q425-results-1768481582799

• Blue Owl Technology Fund (OTF) held investor calls late this week so look for a new issue from them next week.

• No major earnings in the space expected next week.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

NEW ZEALAND: Mkt Expects Q3 GDP At +0.9%q/q, RBNZ Forecast +0.4%q/q

Coming up shortly we have the NZ Q3 GDP print. The market consensus is for a +0.9%q/q rise, which follows a -0.9% contraction in Q2. In y/y terms this would raise growth to 1.3%y/y, from -0.6% in Q2. Note in its Nov projections the RBNZ had a 0.4%q/q growth forecast for Q3 GDP, so the consensus is comfortably above this. The range of market forecasts is 0.6% to 1.1%, with the local banks around the 0.8-1.0% region. Focus will also likely be on revisions to prior history (Q2 or before).

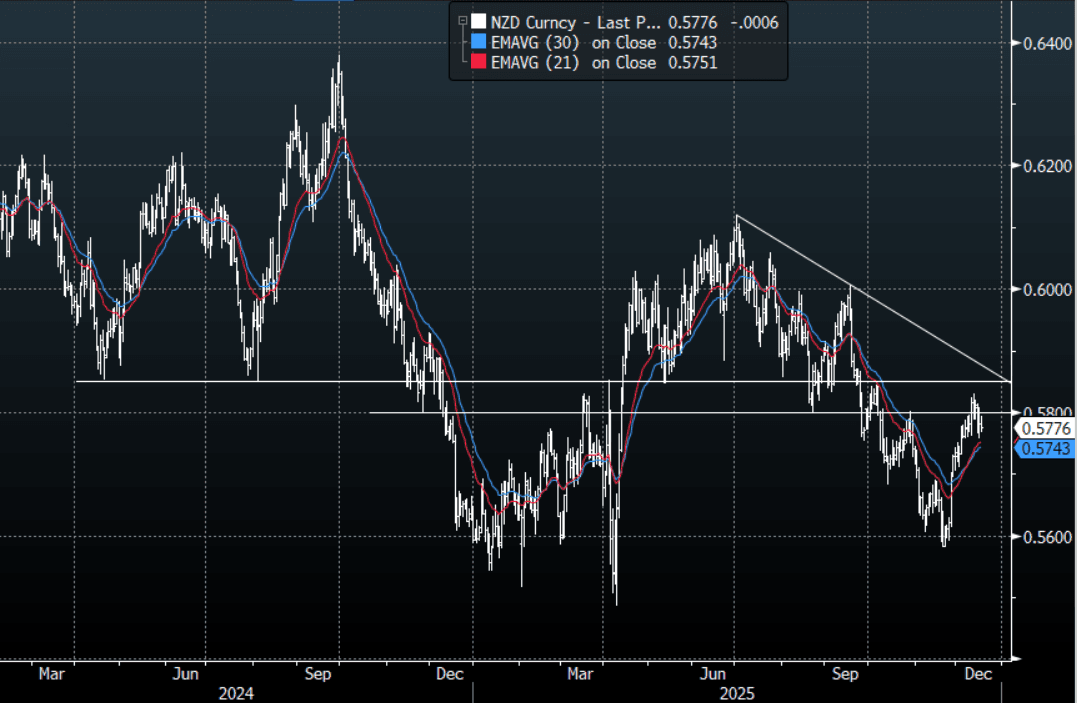

NZD: NZD/USD - Holds Above 0.5750 Ignoring Lower Risk For Now

The NZD/USD had a range overnight of 0.5767 - 0.5794, Asia is trading around {NZD Curncy}. The bounce in AI lasted 1 day and is lower again, the move is starting to turn ugly as sentiment is quickly changing. The NASDAQ and the S&P both look to potentially be putting in double tops and the likes of Nvidia is approaching some pivotal levels as well. This does not augur well for risk and creates significant headwinds for the AUD & NZD which trade with a high correlation to it. The NZD is consolidating its gains above 0.5700-0.5750 and for the most part has been left unscathed by the souring of sentiment. Can it continue to ignore it if the correction builds momentum? On the day, I will be watching the price to see if it can continue to shrug this off, if so then the range will remain, support is back toward 0.5740-0.5760 and resistance is around 0.5810-30. A break through that support could signal the potential for a deeper pullback.

- MNI - NZ Q3 GDP is released Today. After activity contracted 0.9% q/q in Q2, some rebound is expected in Q3 and also into Q4. The RBNZ forecast a 0.4% q/q rise in Q3 GDP in November. The partial data are pointing to a solid outcome with real retail sales rising 1.9% q/q, building volumes +1.5% q/q, manufacturing volumes +1.1%, real merchandise exports up 3.5% q/q while imports were down 1.2% q/q.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5650(NZD410m), 0.5690(NZD531m), 0.5860(NZD471m). Upcoming Close Strikes : 0.5530(NZD475m Dec 23), 0.5630(NZD594m Dec 19), 0.5750(NZD459m Dec 19) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 40 Points

- Data/Event: GDP

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

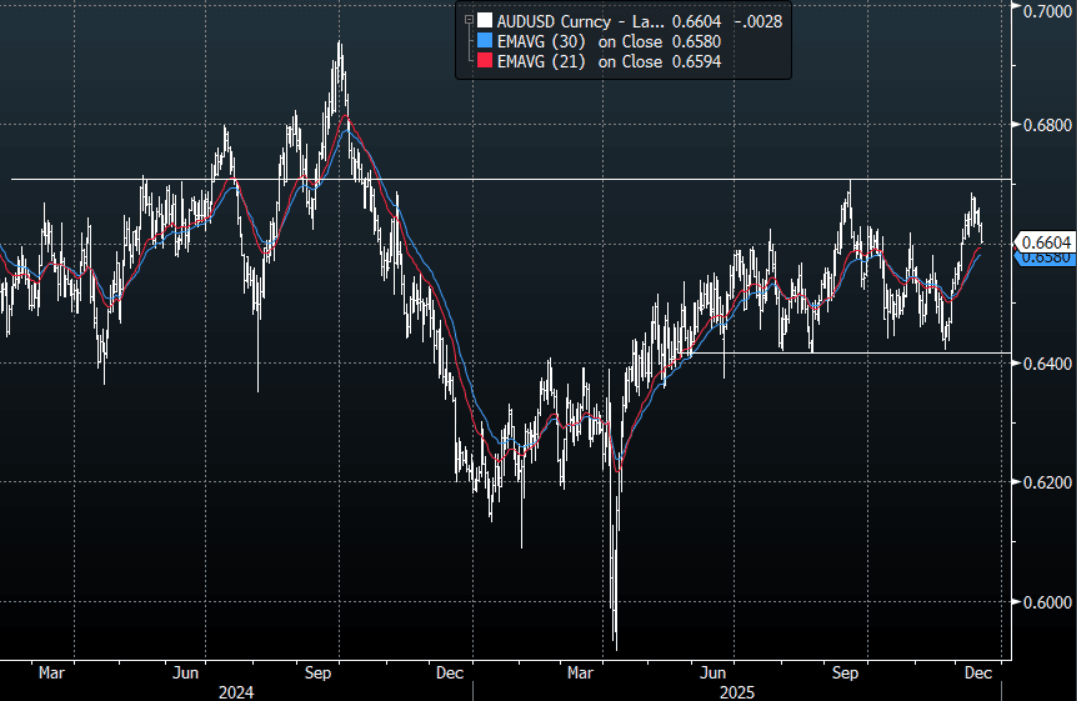

AUD: AUD/USD - Trades Heavy Around 0.6600 As Risk Sentiment Sours

The AUD/USD had a range overnight of 0.6599-0.6629, Asia is trading around {AUDUSD Curncy}. The bounce in AI lasted 1 day and is lower again, the move is starting to turn ugly as sentiment is quickly changing. The NASDAQ and the S&P both look to potentially be putting in double tops and the likes of Nvidia is approaching some pivotal levels as well. This does not augur well for risk and creates significant headwinds for the AUD which trades with a high correlation to it. The AUD price action for the moment remains constructive, but I do remain wary of what seems to be happening in US stocks. Technically while the AUD remains above 0.6500-0.6550 dips should continue to be supported. In the Asian session, watch to see if this 0.6600 area can continue to hold in the face of this souring in sentiment, if not we could see a deeper pullback towards the 0.6500-50 support. On the day I suspect sellers would be looking to fade a bounce back toward the 0.6625-0.6645 area initially looking to see if we can break back below 0.6600.

- Bloomberg reports, “China Vanke asked some commercial banks to accept delayed interest payments on certain borrowings, people familiar said. At least one lender was asked to let the developer delay an interest obligation by one year.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6550(AUD1.07b), 0.6625(AUD849m), 0.6675(AUD989m). Upcoming Close Strikes : 0.6675(AUD1.31b Dec 19), 0.6700(AUD1.57b Dec 19) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 40 Points

- Data/Event: Consumer Inflation Expectation

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P