US TECHNOLOGY: MNI TMT: AI Spending Discourse - MSFT, GOOGL, AMZN, META, ORCL

• Earlier in the year, concerns around AI return-on-investment intensified following DeepSeek’s release and at that time, investors took comfort in two points: first, that most AI infrastructure spending was funded through internal cash flows rather than incremental debt; and second, that lower model costs would ultimately support Jevons-type consumption growth and monetization.

• Today, debt-funded AI capex is accelerating across both public and private markets, and investor skepticism around ROI has not meaningfully abated.

• We look at five large AI infrastructure spenders - Microsoft, Alphabet, Amazon, Meta and Oracle - and address three issues:

• The scale and timing of capacity commitments and their translation into capex;

• Recent debt issuance and spread movement; and

• Resultant credit profiles and rating-agency thresholds, with a particular focus on Meta and Oracle.

• Bottom line: Credit profiles across the group remain solid and, in our view, can absorb continued debt-funded capex while preserving current ratings. That said, Oracle’s credit metrics have deteriorated and its headroom has tightened, and Meta’s combination of elevated capex and shareholder-returns, coupled with what we think could be increased M&A activity, could deteriorate credit metrics. However, Meta is more likely to slow buybacks if AI capex and acquisitions accelerate.

• Capex for the five issuers in calendar year 2026 (as shown in the table below), is expected to grow ~31% YoY, led by Meta (+53%) and Microsoft (+40%).

• Building a 1 gigawatt (GW) AI-optimized data center in the US is estimated at ~$35 billion, although NVIDIA has suggested a higher range ($50–$60B) reflecting next-generation higher-ASP GPUs. This compares with $7–12B for a traditional hyperscale facility. Cost composition typically breaks down into: 45–50% compute, ~15% networking, and the remainder across memory, storage and physical infrastructure like power systems, land, and HVAC.

• This serves as context given Oracle’s Stargate project with OpenAI and SoftBank, which targets 10 GW of cumulative capacity between 2025 and 2029, and Meta’s Hyperion facility in Louisiana, planned to scale to 5 GW by 2029 (expected to be the largest of Meta’s 29 facilities). As of September, Oracle had identified sites representing roughly 7 GW and had brought the first facility (Abilene, Texas) online. For these projects, the operators i.e ORCL, META, bear the compute and networking costs (roughly 60–65%), which appear as cash capex, while physical facility construction typically shows up as lease liabilities or JV-structured off–balance sheet commitments depending on ownership share.

• Given the cost of compute chips is borne by the operators, the risk of accelerated depreciation is an investor concern, but current evidence supports longer economic life than feared. NVIDIA’s A100 chips from 2020 remain fully utilized, and CoreWeave’s early H100 contracts (signed in 2022) were recently recontracted at a low-single-digit discount, suggesting lower risks of capital obsolescence for the chips.

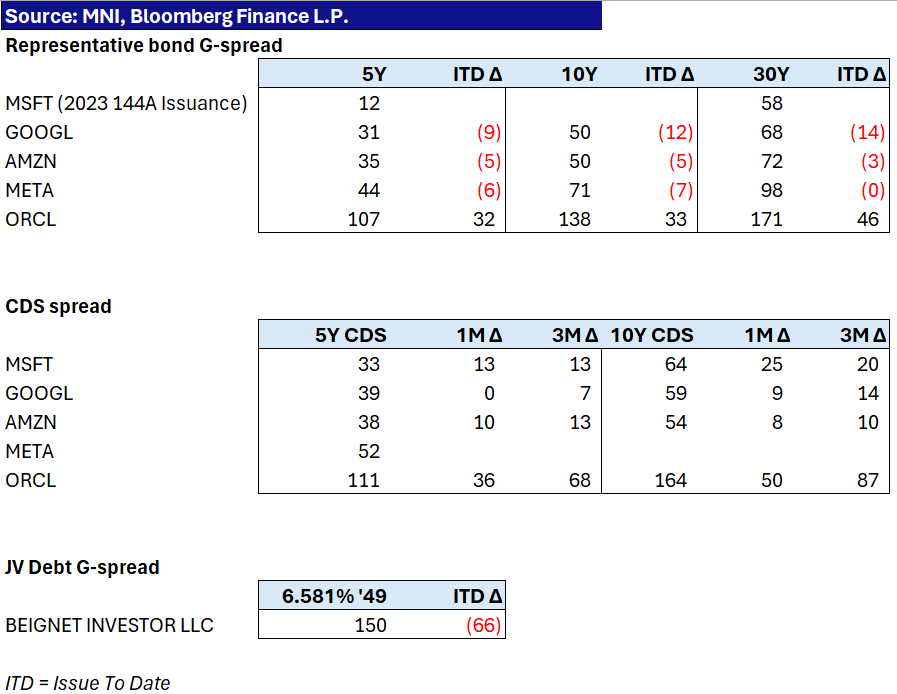

• Four of the five issuers have issued in the public debt markets over the past three months. In addition to this, Meta’s Beignet JV (20% Meta / 80% Blue Owl-managed funds) issued a $27 billion 2049 144A bond following an initial private placement, and Oracle is reported to be arranging two debt packages totaling ~$38 billion. Rating agencies have historically treated such JV structures as neutral to the operator’s credit profile when the economics resemble the Intel–Brookfield foundry JV, where risk-sharing and contractual revenue visibility mitigate off–balance sheet leverage.

• Meta has issued at least annually in the public debt market over the last three years and we view the recent widening in Meta’s curve as technically driven rather than reflective of credit deterioration. Oracle, by contrast, faces a more constrained FCF profile. Although capex is supported by a reported $455B backlog translating into multi-year revenue visibility, spreads have widened in line with weaker FCF projections. Moody’s downgrade threshold of >3.5x gross leverage still provides headroom, and we expect rating agencies to allow execution time. More so, the companies communicating their financial policy would be crucial in maintaining ratings if growth is delayed - which we view as a concern in ORCL’s case given their lack of financial policy clarity.

• Lastly, a more benign regulatory environment, illustrated by recent Meta and Google antitrust legal wins, could embolden hyperscalers to pursue AI-related acquisitions which could pressure credit metrics, although we would expect lower shareholder returns to be an offset.

Sources: MNI, Bloomberg Finance L.P., Bernstein Research

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA: China in Trilateral Currency Swap Talks with Japan and South Korea

- "*CHINA EYES 3-WAY CURRENCY SWAP WITH JAPAN,SOUTH KOREA: SCMP" (BBG)

- “Beijing seeks to strengthen regional financial ties and boost yuan use as US trade pressures weigh on East Asian economies”

- "China is in talks with Japan and South Korea – both US allies – about a possible trilateral currency swap to bolster the region’s financial safety net and deepen economic cooperation amid US President Donald Trump’s trade war, according to a source familiar with the issue."

- Full piece: https://www.scmp.com/news/china/money-wealth/article/3329849/china-eyes-3-way-currency-swap-japan-and-south-korea-amid-trumps-tariff-war-source

LOOK AHEAD: Wednesday Data Calendar

- US Data/Speaker Calendar (prior, estimate)

- 10/22 0700 MBA Mortgage Applications (-1.8%, --)

- 10/22 1130 US Tsy 17W bill auction

- 10/22 1300 US Tsy $13B 20Y Note re-open (91210UN6)

- Source: Bloomberg Finance L.P. / MNI

SECURITY: Ukraine And Europe Working On 12-Point Plan To End Ukraine War - BBG

Bloomberg News reporting that, “European nations are working with Ukraine on a 12-point proposal to end Russia’s war along current battle lines, pushing back against Vladimir Putin’s renewed demands to the US for Kyiv to surrender territory in return for a peace deal.” According to Bloomberg sources, “A peace board chaired by US President Donald Trump would oversee implementation of the proposed plan…” Seemingly a reference to Trump's “Board of Peace” for Gaza.

- The plan stipulates that, “both sides commit to halting territorial advances, the ... return of all deported children to Ukraine and exchanges of prisoners. Ukraine would receive security guarantees, funds to repair war damage and a pathway to rapidly join the European Union. Sanctions on Russia would gradually be lifted though some $300 billion in frozen central bank reserves would only be returned once Moscow agrees to contribute toward Ukraine’s post-war reconstruction.”

- The plan comes ahead of a tentatively scheduled second in-person summit between Trump and Russian President Vladimir Putin in Budapest, Hungary. Likely to take place after Trump returns from the APEC summit in early November, where he is expected to meet with Chinese President Xi Jinping.

- There may be limited optimism in European capitals that such a plan can gain traction with Putin or Trump without including Russian demands for territorial exchanges, regime change, and assurances on Kyiv's NATO aspirations.

- However, the template may be based on the recent US-brokered Gaza peace plan, which managed to achieve a ceasefire between Israel and Hamas without a detailed plan for the next phases of the peace plan.

- Notably, the plan, as reported by Bloomberg, primarily focuses on freezing the war along the current front lines before beginning negotiations towards a broader peace deal. It doesn't refrains from referencing territorial exchanges and only mentions Ukraine's EU membership.