MNI Riksbank Review: March 2026 - Ready to Act If Needed

Mar-20 13:20By: Emil Lundh

Sweden

Hidden PDF

EXECUTIVE SUMMARY:

- The Riksbank held the policy rate at 1.75% in a unanimous decision. Guidance re-iterated that the rate is likely to remain at this level “for some time to come” (a moderate surprise versus our expectations), but uncertainty around the baseline projections was stressed throughout.

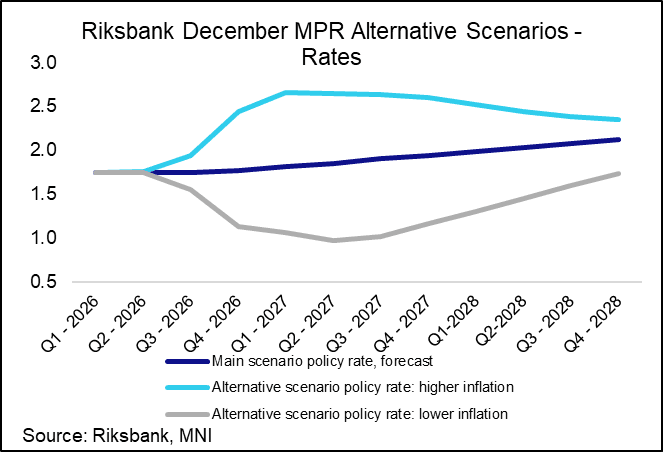

- The March MPR rate path was unchanged relative to December, with the Riksbank noting that it was too early to see how the Iran war was affecting the outlook. In that light, the two alternative scenarios presented are worth particular attention.

- Clearly, the stagflationary scenario is most important in the current context, and Governor Thedeen noted in the press conference that we are already starting to move away from the “short lived” shock scenario. If the Board gains confidence that this scenario is playing out, we don’t think it would hesitate in raising rates

- That said, we think the bar to Riksbank hikes is higher than that of the ECB.

- The only analyst forecast change we have seen following the March decision has been Morgan Stanley, who now expect a single rate hike in June

- Market reactions following the decision were limited, with Swedish rates impacted more by movements in foreign rates on the day. At the time of writing, the Dec26-Mar27 FRA is at 2.62%, 55bps above the 3m STIBOR rate. This seems quite aggressive given the starting position for the Swedish economy, but it is difficult to have confidence in fading the move while the Iran war continues flaring.