MNI RBA WATCH: Further Easing Likely As Domestic Factors Weigh

The Reserve Bank of Australia is likely to lower the cash rate by a further 25 basis points to 3.6% at its meeting next Tuesday, as domestic conditions continue to soften and inflation falls further into the 2-3% target band amid concerns over global trade.

A cut would bring total easing since February to 75bp, following reductions in both February and May – the latter meeting including discussion of a larger 50bp move driven partly by concerns over international trade. (See MNI RBA WATCH: Board's Dovish Turn Included Debate Of 50bp Cut)

The expected rate cut is likely to be accompanied by more domestically-focused communication, as the Bank awaits further clarity on the global environment, which is not expected to fully materialise until later this year.

Markets have fully priced in a 25bp cut, and are assigning an 80% probability to another reduction at the Aug 12 meeting. Current market pricing implies a 3% cash rate by year-end, suggesting at least one more move lower before December.

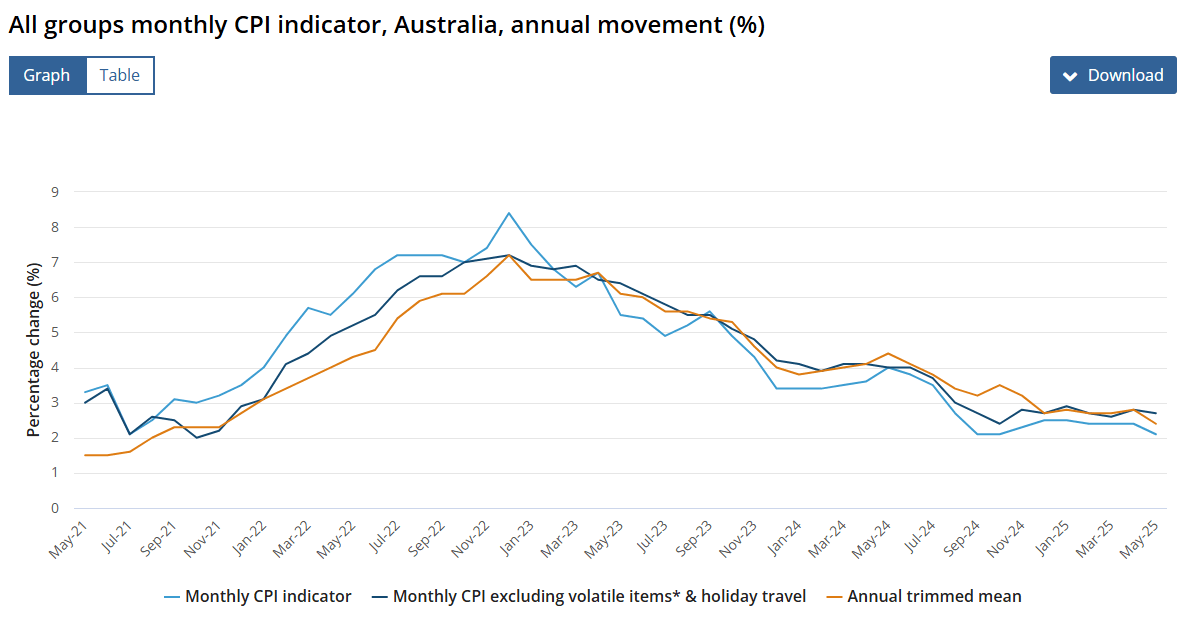

DOMESTIC DATA WEAKENS

May’s monthly CPI indicator came in 20bp below expectations at 2.1%, while the trimmed-mean inflation rate fell 40bp to 2.4%. Importantly, the May print included key Q2 market services inflation, a category the RBA is closely monitoring, while housing cost growth also continued to moderate.

While the Bank puts more weight on quarterly inflation data, the consistent easing in monthly figures adds to the case for a rate cut.

Retail sales rose just 0.2% m/m and 3.3% y/y in May, also below expectations. Though slightly higher than in April, sales growth has not exceeded 0.2% since January’s 0.5% rise, and the year-ended pace has slowed from March’s 4.3% peak.

While labour market conditions remain tighter than the RBA would prefer, with the unemployment rate holding at 4.1%, signs of cooling are emerging. The economy shed 21,000 jobs in May, down sharply from April’s 89,000 gain.

GDP per hour worked, a key productivity indicator, fell 1% y/y in Q1, while real unit labour costs rose 2.6%. The RBA expects productivity growth to improve gradually, reaching 0.9% by the December quarter. Still, the Reserve does not see weak productivity as a reason to delay further easing, as it reflects a drag on both supply and demand. (See MNI POLICY: RBA Trade Concerns Abate, Focus On Domestic Market)

INTERNATIONAL RISKS EASE

The global trade outlook was front and centre at the RBA’s May meeting, and shaped Governor Michele Bullock’s public messaging. While these immediate concerns have since moderated, the RBA believes any adverse impact will take longer to materialise, allowing a renewed focus on domestic trends at the next two policy meetings.

So far, the RBA has not observed significant declines in business or consumer sentiment that would point to spillovers from U.S. actions. Washington’s retreat from its most aggressive trade measures in response to market volatility has helped reduce short-term risks, while China continues to show resilience.

Despite this, the RBA will continue to note the potential for greater uncertainty in the second half, alongside the softer domestic data.