US: MNI POLITICAL RISK - Trump's NatSec Pivot To The Western Hemisphere

Dec-05 13:25

Download Full Report Here

- President Donald Trump will attend the FIFA World Cup draw at 11:40 ET 16:40 GMT. He is expected to meet with co-hosts, Canadian Prime Minister Mark Carney - for the first time since trade talks collapsed - and Mexican President Claudia Sheinbaum - for the first time ever.

- The ad hoc North American leaders’ summit comes as the USTR concludes a three-day public hearing on the USMCA. USTR Jamieson Greer warned this week that the US may walk away from the trade bloc.

- The Trump administration released its National Security Strategy, outlining ‘corrections' to strategies that have “fallen short” since the end of the Cold War. The strategy, billed as a “corollary” to the Monroe Doctrine, focuses heavily on the Western Hemisphere.

- House Speaker Mike Johnson (R-LA) will discuss healthcare strategy with House Republicans this weekend ahead of next week's Senate vote on expiring ACA subsidies.

- Republican leaders are unlikely to release the final text of the annual Pentagon spending bill today, amid intraparty fights over policy.

- The Supreme Court handed Trump a major win by releasing a new Texas Congressional map.

- Vice President JD Vance expects “good news” over the next weeks on a Ukraine peace deal. German Chancellor Friedrich Merz is leading emergency talks on using frozen Russian assets.

- A US trade delegation is expected to visit New Delhi next week.

- Poll of the Day: Trump’s approval rating has stabilised following a November decline.

Full Article: US DAILY BRIEF

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: MNI POLITICAL RISK - 'Blue Wave' Fuels Democratic Optimism

Nov-05 13:20

Download Full Report Here

- President Donald Trump will deliver remarks to a breakfast for Republican Senators at 08:30 ET 13:30 GMT, before departing for Miami, where he will deliver remarks at the American Business Forum Florida. Secretary of State Marco Rubio will brief lawmakers on the Trump administration's anti-narcotics operations in Latin America before hosting his counterparts from Central Asia ahead of a landmark leaders' summit tomorrow.

- Voters delivered a rebuke to Trump with a 'blue wave' of Election Day results. While Republicans will stress that off-year elections are not predictive of future elections, bettors saw enough in yesterday’s results to invert their outlook for the midterms.

- The election results may temper growing optimism for a quick resolution to the government shutdown by appearing to endorse Senate Minority Leader Chuck Schumer’s (D-NY) hardline strategy to extract concessions on healthcare. The Virginia results, in particular, may buoy Democrats as the state is home to a high proportion of federal government workers directly impacted by the shutdown.

- At 10:00 ET 15:00 GMT, the Supreme Court will hear arguments on the legality of Trump’s reciprocal tariffs. Prediction markets assess a rougly 60% chance Trump loses the case, which may be pessimistic considering the court’s recent rulings on issues relating to executive authority.

- Trump announced that trade talks with Switzerland have restarted after a meeting with executives.

- Poll of the Day: Trump’s approval for his handling of the shutdown has fallen faster than that of Democrats and Congressional Republicans.

Full Article: US DAILY BRIEF

US TSYS: Post-ADP React

Nov-05 13:18

- Treasuries declining after larger than expected Oct ADP jobs gain. Currently, the Dec'25 10Y contract trades 0.0 at 112-25, 10Y yield 4.0929% (+.0077), curves mildly steeper (2s10s +.136 at 50.865; 5s30s +.312 at 97.021).

- A short-term bearish threat in Treasuries remains present. Recent weakness has resulted in a breach of the 50-day EMA, currently at 112-26+. This highlights potential for a deeper retracement near-term. A continuation lower would open 112-06, the Sep 25 low and the next key support. The contract needs to trade above 113-18+, the Oct 28 high to signal a possible bullish reversal. Key resistance and the bull trigger is at 114-02, the Oct 17 high.

- USD only marginally gains on the back of the stronger-than-expected headline - helping both EURUSD and GBPUSD edge away from any test on earlier highs. All-in-all the reaction is largely contained, however USDJPY is pressuring 153.84 and the best levels of the day.

- Next up: US Tsy Quarterly Refunding annc at 0830ET followed by S&P Global US Services/Composite PMI at 0945ET.

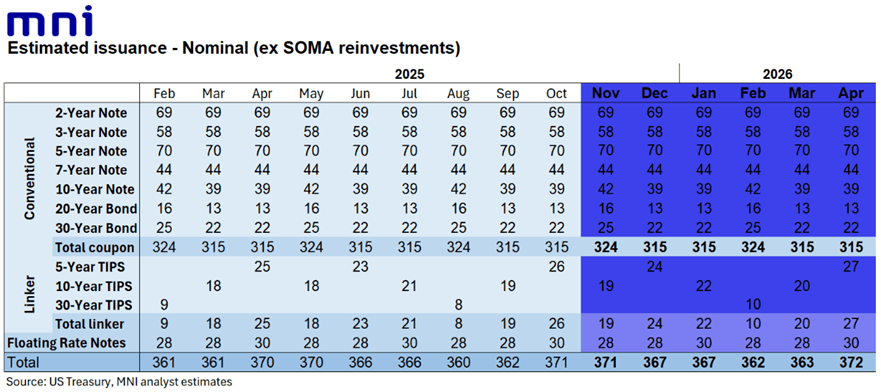

US TSYS/SUPPLY: No Change To Coupon Size Guidance, But Bills Eyed in Refunding

Nov-05 13:11

A few areas to watch in today's 0830 Refunding announcement - MNI's full preview is here

- Guidance: We do not expect Treasury’s guidance on coupon issuance to change in this Refunding round ("Treasury anticipates maintaining nominal coupon and FRN auction sizes for at least the next several quarters.")

- Coupon sizes for upcoming quarter (Nov-Jan): As seen in table below. The Refunding itself will be $58B in new 3Ys, $42B in new 10Y, and $25B in new 30Y for next week.

- Buybacks: After being in some focus in August's Refunding, we don’t expect any changes to buyback program parameters this time, following the last round’s amendments that included higher-frequency operations/increasing the size of long-end buybacks. There are some risks that buyback sizes could be slightly increased, or that Treasury announces that the list of eligible counterparties will be expanded.

- Bill guidance: This will be of some interest given that borrowing expectations for the coming quarter were at the lower end of the expected range - one thing to watch will be if Treasury guides to reducing bill auction sizes soon having increased them significantly in late September/early October, helping push the TGA cash pile to the $1T mark. Last time that guidance read: "Treasury anticipates further marginal increases in short-dated Treasury bill auction sizes in the coming days and then maintaining sizes at or near those levels through the end of September. Additional increases to Treasury bill auction sizes are anticipated in October. Treasury will carefully monitor market conditions and adjust its bill issuance plans as appropriate. "