US: MNI POLITICAL RISK - Trump Meets Netanyahu Amid Iran Tensions

Feb-11 13:15

Download Full Report Here: https://media.marketnews.com/MNIPOLRISKUS_Daily110226_50f10badb3.pdf * P...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EFSF ISSUANCE: Dual Tranche 3/10-year Syndication: Allocations

Jan-12 13:14

New 3-year Benchmark

- Size: E3bln

- Spread set at MS+5bps (guidance was MS +6bps area)

- Books closed in excess of E18bln (inc E1.3bln JLM interest)

- HR: 94% vs 2.10% Apr-29 Bobl

- Coupon: Long first

- Maturity: Feb 2, 2029

- ISIN: EU000A2SCAW0

New 10-year Benchmark

- Size: E4bln

- Spread set at MS+30bps (guidance was MS +33bps area)

- Books closed in excess of E37.5bln (inc E2.1bln JLM interest)

- HR: 94% vs 2.90% Feb-36 Bund

- Coupon: Long first

- Maturity: Feb 1, 2036

- ISIN: EU000A2SCAX8

For both:

- Total Size: MNI expected E5-7bln with upside risks. The combined size is therefore the top of our expected range.

- Bookrunners: BARCLAYS (DM/B&D) / DB / GSBE SE

- Settlement: Jan 19, 2026 (T+5)

- Timing: Hedge deadline 13:30GMT / 14:30CET

From market source / MNI colour

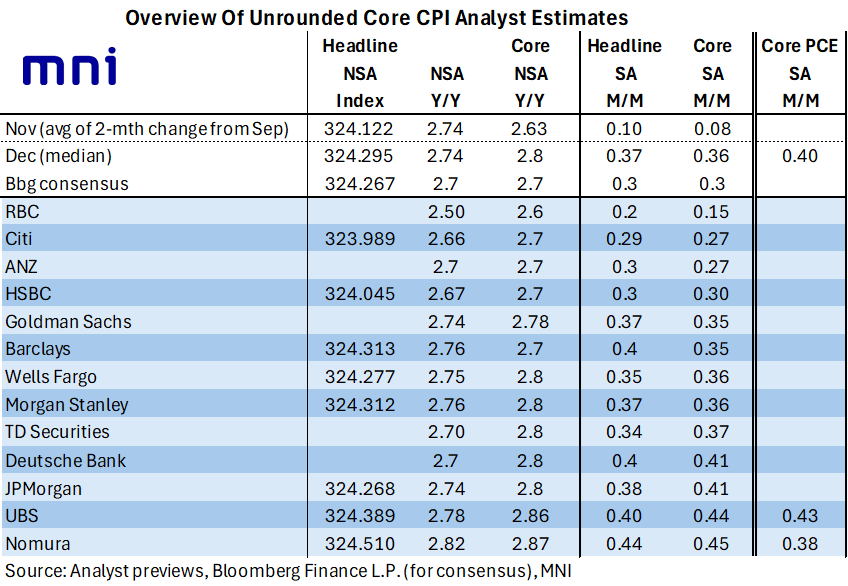

US OUTLOOK/OPINION: Unrounded CPI Estimates Point To Upside Surprise In Dec

Jan-12 13:05

- The below unrounded analysts estimates for headline and core CPI in December point to an upward surprise to Bloomberg consensus looking for 0.3% M/M for both.

- We see a median core CPI estimate of 0.36% M/M in Dec, with an unusually wide range of 0.15-0.45%, following the implied average increase of 0.08% M/M between Sept and Nov.

- Similarly, we see a median headline CPI estimate of 0.37% M/M in Dec after the average 0.10% M/M in the prior two months [noting that this Dec estimate necessarily includes some rounded figures].

- Core CPI is seen at 2.8% Y/Y across this selection of analysts, albeit 2.76% on average, to remain consistent with some light upside risk to consensus of 2.7% Y/Y.

- Recall that core CPI surprisingly slipped to 2.63% Y/Y in November after 3.02% Y/Y in September, with methodological approaches and a later than usual survey seen playing a large role in weakness.

STIR: Repo Reference Rates

Jan-12 13:03

- Secured Overnight Financing Rate (SOFR): 3.64% (+0.00), volume: $3.166T

- Broad General Collateral Rate (BGCR): 3.61% (+0.00), volume: $1.323T

- Tri-Party General Collateral Rate (TCR): 3.61% (+0.00), volume: $1.296T

- (rate, volume levels reflect prior session)