MNI INTERVIEW: Dollar Flight Risks Global R* Shift

Continued capital outflows from dollar assets will weaken the U.S.'s role as the main driver of the global neutral rate, leading to a more multipolar world where the “r*”s of other open economies are shaped more by local conditions, a leading Australian economist told MNI.

“It takes quite a shock to stop the U.S. being the global currency for trade and capital flows, but we may be seeing this shock,” said James Morley, professor of macroeconomics at the University of Sydney and co-author of a recent paper that studied the U.S.'s relationship with the global neutral rate.

While the U.S.’s influence on global r* will dissipate and its own neutral rate will become more susceptible to domestic idiosyncrasies, open economies could also see a similar effect, leading to a more multilateral world, Morley argued.

The erosion of the dollar’s reserve status will drive lower capital mobility as trades are conducted in a range of less liquid currencies, he said. "Therefore there's more reason for dominance of idiosyncratic movements," he continued. "But I think the first order, the primary effect you would see, is that the U.S. decouples a bit from being the global r*."

Markets have been reassessing whether there is some idiosyncratic risk to U.S. bonds over the past few weeks, he noted. "And if they decide that there is then you could imagine some decoupling between the global r* and U.S. r*. They'll still move together, because the U.S. can be quite representative of global movements, but you would then expect some other idiosyncratic drivers."

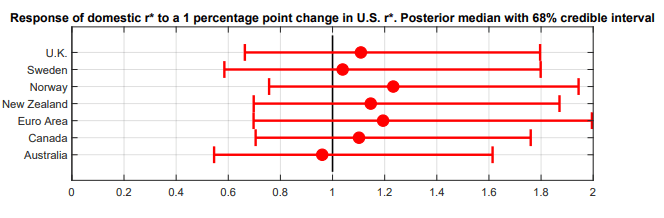

Morley's Hidden PDF paper argued the U.S. neutral rate was the primary driver of global r* and, from a small open economy perspective, “shocks to global r* are essentially equivalent to shocks to U.S. r*" (See chart)

"While local shocks can matter, the long-term decline in r* appears to be due to global forces such as a lower U.S. productivity growth and an increase in safe asset demand," the paper stated.

LOWER GLOBAL R*

However, the global neutral rate could fall should the dollar retain its dominance amid the U.S. administration’s current trade policies and their uncertainty, as trade restrictions act as an efficiency shock and pull American productivity down, Morley argued.

But this does not necessarily mean other open economies will follow, he added, noting the trade chaos will impact each country differently in the short term. Australia, for instance, will be influenced greatly by China’s economy, and could experience the U.S. slow down as a demand shock, he continued.

Real long-term interest rates reflect long-term growth expectations, making it difficult to predict, he added. “But unfortunately, we're being given a bit of a natural experiment here,” he said. “And so you would think that this will show up in productivity numbers for the U.S., which would drive r* back down a bit.”