MNI Fed Preview - January 2026: New Year, Same Divisions

Jan-23 22:15By: Tim Cooper

US

Hidden PDF

EXECUTIVE SUMMARY

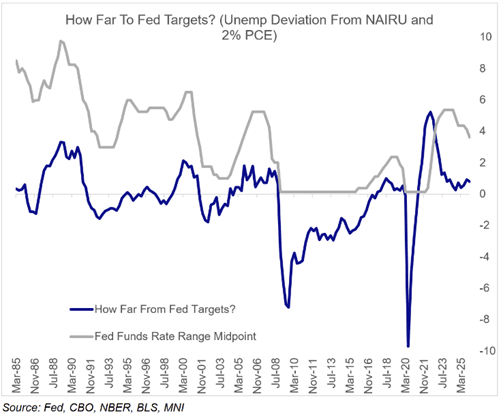

- The FOMC's January meeting appears poised to deliver a neutral hold, with heated debate continuing about the appropriate pace of easing over the coming year.

- Divisions within the FOMC over the way forward are unlikely to have narrowed much since the December cut. The center of the Committee is likely to hold sway in maintaining an easing bias, albeit with no rush to make the next move now that rates have been brought down to within plausible estimated ranges of neutral policy.

- If anything, the Committee may be even more patient now than it was 6 weeks ago.

- Recent data have done little on net to affirm the case for another near-term cut, with the unemployment rate steadying and economic activity proving more resilient than expected.

- With government shutdown-related distortions failing to clarify the overall picture, Chair Powell is likely to repeat his message from the December meeting that the FOMC is "well positioned to wait to see how the economy evolves", with plenty of data to consider before the next decision in March.

- The new Statement is likely to see only limited changes, but should acknowledge both reduced near-term concerns over the labor market as well as the above-expected economic activity since the last meeting. It will maintain the rather vague forward guidance adopted in December that the “extent and timing” of future easing will depend on the data.

- That would likely be taken in stride by rate markets which price only around a 3% implied probability of a 4th consecutive 25bp cut, with the next easing expected only by July.

Trending Top

Jun-25 06:23