MNI EXCLUSIVE: Sources On New Bank of Spain Governor Escriva

Sep-04 14:14

MNI speaks to sources in and outside Spain about New Bank of Spain Governor Jose Luis Escriva.- On MNI Policy MainWire now, for more details please contact sales@marketnews.com

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Off Highs As Risk Sentiment Stabilises

Aug-05 14:10

Gilts move further away from session highs on the back of the U.S. ISM services data.

- The space had already pulled back from best levels as e-minis traded away from lows and the latest round of medium-dated APF sales from the BoE saw tepid demand, generating a bid to cover of ~1.5x.

- Futures briefly moved below 100.50, before recovering to 100.70.

- Cash gilt yields unchanged to 5bp lower on the session, with the 7- to 10-Year zone now underperforming (presumably driven by the tepid demand at the APF sale).

- The front end of the curve continues to outperform.

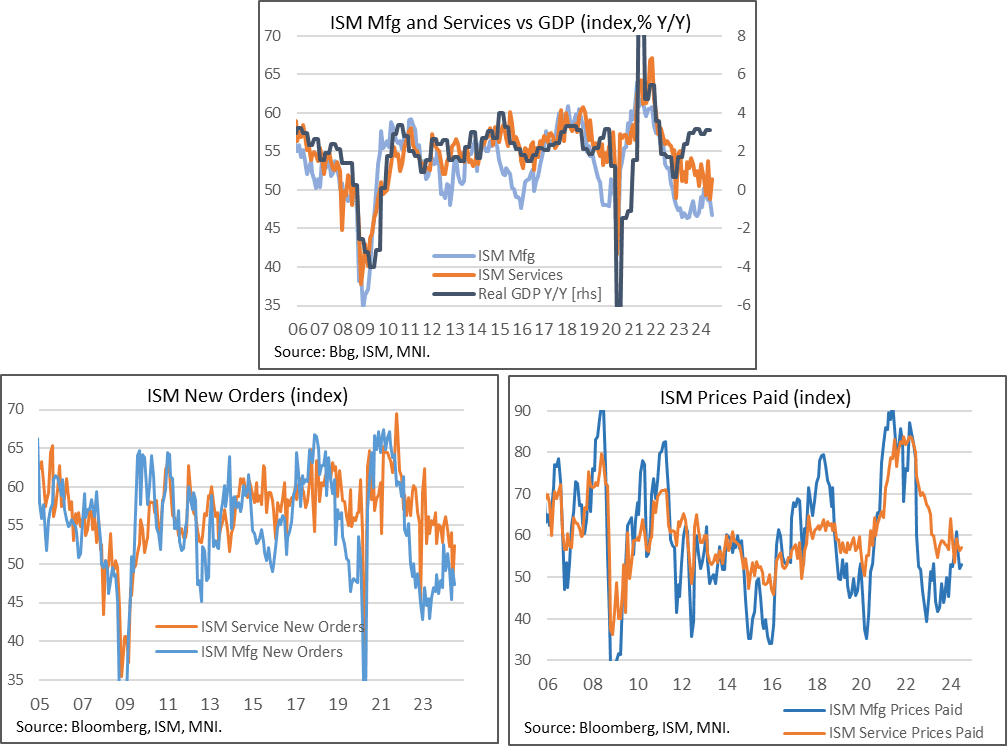

US DATA: ISM Services Pushes Back On Recession Fears

Aug-05 14:09

- ISM services was a little better than expected in July at 51.4 (cons 51.0), confirming a return above 50 after what had been the lowest since early in the pandemic.

- That little better result, especially with firmer underlying details, carries an oversized market impact as it helps dampen an imminent recession angle that appeared to have been priced in.

- New orders: 52.4 (cons 49.8) after 47.3. Still on the lower side of recent months but it sees a reversal from the first sub-50 reading since Dec’22. It also goes against the latest firmly contractionary new orders reading for last week’s ISM manufacturing report.

- Prices paid: 57.0 (cons 55.1) after 56.3, similar to the 58.3 averaged through 1H24 and 57.9 in 2H23.

- Employment: 51.1 (cons 46.4) after 46.1, its highest since Sep 2023.

STIR: SONIA Stabilises Around 60bp Of '24 BoE Cuts, Macro Dominates Domestic Matters

Aug-05 14:09

Some will suggest that the dovish GBP STIR repricing through year end has become stretched.

- ~17bp of cuts are priced into BoE-dated OIS through the Bank’s September decision, with a cumulative ~60bp of easing showing through the Dec MPC.

- Those touting stretched moves will be comparing market pricing to the nature of last week’s “hawkish” BoE rate cut and lack of commitment to further imminent easing in several rounds of post-meeting MPC communique.

- We note that the latest round of dovish repricing is macro driven, with economic uncertainty in the U.S. and pricing of potential intra-meeting Fed action dominating.

- This means broader market sentiment and offshore matters will likely remain at the fore in the very immediate term, particularly with the next BoE decision not due until September 19 and with no tier 1 UK data due this week.

- Next week will see the monthly UK CPI & labour market data cross, reintroducing some local impetus.

| BoE Meeting | SONIA BoE-Dated OIS (%) | Difference Vs. Current Effective SONIA Rate (bp) |

| Sep-24 | 4.781 | -16.9 |

| Nov-24 | 4.535 | -41.5 |

| Dec-24 | 4.360 | -59.0 |

| Feb-25 | 4.141 | -80.9 |

| Mar-25 | 3.993 | -95.7 |

| May-25 | 3.830 | -112.0 |

| Jun-25 | 3.735 | -121.5 |