MNI Eurozone Inflation Insight – November 2024

Dec-02 21:58By: Tim Cooper and 1 more...

Inflation

Softer Services Momentum Fails To Ensure 50bp Dec Cut

PDF ANALYSIS HERE: Nov2024EZCPIReview.pdf

- The November EZ flash inflation round saw the second consecutive reacceleration from cycle lows in September.

- But while an uptick in headline was expected on the back of energy base effects, the core measure remained unchanged at 2.7%, and some analysts now see it undershooting the ECB’s forecast by about 0.2pp in Q4.

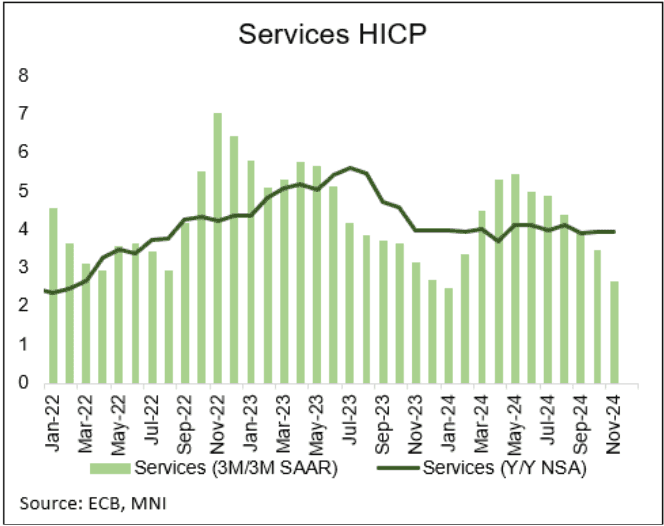

- Services inflation saw softer momentum in November, running at 2.63% 3m/3m SAAR – a YTD low, with the yearly rate decreasing slightly (-0.1pp to 3.9% in Nov).

- But even combined with elevated political uncertainty and a continued subdued growth outlook, the softer services inflation momentum was not able to convince markets to expect an outsized cut at the ECB’s December meeting next week, with meeting-dated OIS pricing around 30bp of cuts for the Dec meeting (vs around 32bp at the beginning of last week).