MNI Eurozone Inflation Insight – May 2025

Jun-03 18:03By: Tim Cooper and 1 more...

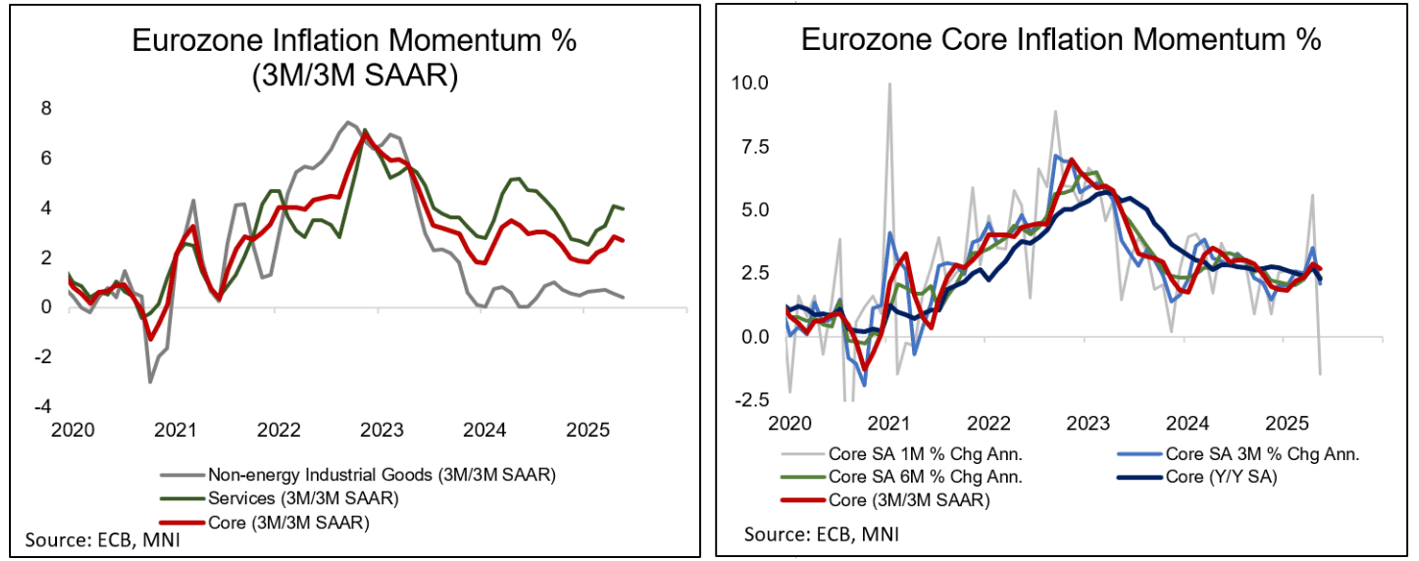

Inflation

Services Y/Y Falls To 3-Year Low

- Eurozone May flash HICP headline and core both printed 0.1pp below consensus expectations, at 1.9% and 2.3%, respectively. Services inflation saw a more meaningful 0.2pp ‘miss’ at 3.2% Y/Y, materially below April’s 4.0% for the lowest reading since March 2022.

- The deceleration seems to have been underpinned by an “Easter Effect” unwind but a medium-term view on the ECB’s seasonally adjusted data suggests that some underlying softening was also likely at play.

- Across the main countries, lower-than-expected readings were observed in France (0.6% Y/Y vs 0.9% cons), Spain (1.9% vs 2.0% cons), and notably the Netherlands (3.0% vs 3.8% cons), while Italy printed inline (1.9% vs 1.9% cons) and Germany was slightly firmer than expected (2.1% vs 2.0% cons). The drag on euro area inflation from the Netherlands was of particular note, as it looks to have contributed significantly to the below-expected EZ reading.

- The inflation data kept market expectations firmly for a 25bp cut at the upcoming June ECB meeting – see our full preview of the decision here.

- MNI published a sources story on May 30 highlighting that the upcoming ECB June meeting is set to see a lower inflation forecast for 2026, from 1.9% in March’s projections to 1.7% or 1.8% in the updated round. “Despite this downward revision, this deviation below 2% will not be considered strong enough to automatically trigger an additional rate cut beyond the June meeting, as some of the drivers of this inflation revision could reverse course given uncertainty over international trade”, the sources piece read (link).