MNI EUROPEAN OPEN: US Strikes Set To Intensify

EXECUTIVE SUMMARY

- TRUMP TELLS CNN THE ‘BIG WAVE’ IS YET TO COME IN WAR WITH IRAN - CNN

- US EMBASSY IN RIYADH ATTACKED AS IRAN STEPS UP SAUDI STRIKES - BBG

- ECB'S LANE SAYS WAR, OIL SUPPLY DROP MAY SEE INFLATION SPIKE - FT

- US, CHINA TRADE CHIEFS TO MEET MID-MARCH BEFORE TRUMP-XI SUMMIT - BBG

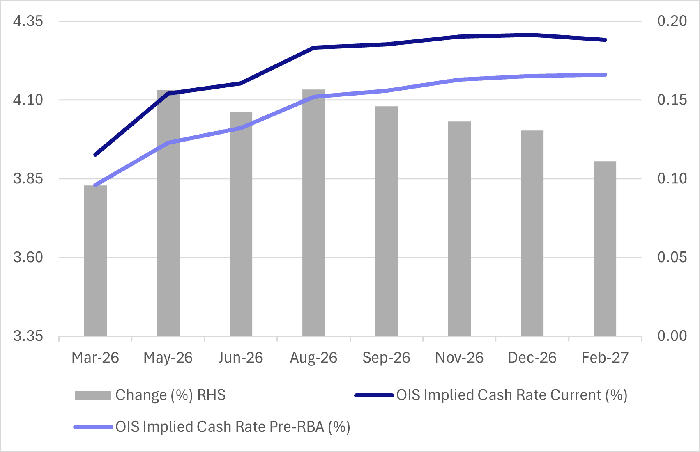

- RBA SAYS INFLATION PATIENCE HAS LIMITS, MARCH MEETING IS ‘LIVE’ - BBG

Fig 1: RBA Market Pricing Firms

Source: MNI - Market News/Bloomberg

UK

INFLATION (MNI BRIEF): UK shop price inflation slowed to 1.1% in February, down from 1.5% in January, the British Retail Consortium said on Tuesday. Food inflation also decelerated, slowing to 3.5% year-on-year against 3.9% in January. Fresh food inflation stood at 4.3% vs 4.4%.

FISCAL (BBG): “ Chancellor of the Exchequer Rachel Reeves will use her economic statement on Tuesday to lament that the world is awash with uncertainty. And she’ll try not to contribute any more of it — by saying as little as possible.”

EU

ECB (FT/BBG): " A prolonged war in the Mideast and a persistent fall in oil and gas supplies could cause a “substantial spike” in inflation and a sharp drop in output, European Central Bank Chief Economist Philip Lane told the Financial Times in an interview."

SHIPPING (BBG): “Shipowners and brokers are demanding more than $200,000 a day for liquefied natural gas tankers in the Atlantic Basin, roughly double what they were commanding less than a day earlier, according to people familiar with the matter.”

ENERGY (MNI BRIEF): The European Commission will meet the International Energy Agency and member states in an "Energy Taskforce" for the first time this week, it said on Monday.

SWEDEN (MNI BRIEF): “The wide gap between the Riksbank's and Norges Bank's policy rates reflect a mix of factors, including Sweden's recent krona strength, lower neutral rate and inflation expectations, Riksbank Deputy Governor Anna Seim said at a Norges Bank conference Monday.”

US

IRAN (CNN): “President Donald Trump told CNN the “big wave” of the US attack on Iran is yet to come. Trump laid out his war objectives for reporters, saying he wanted to destroy Iran’s missile capabilities, annihilate its navy, end its nuclear ambitions and stop it arming militant groups.”

IRAN (BBG): “Secretary of State Marco Rubio said the US military would step up its attacks against Iran, a stark warning after two days of strikes across the country that the Trump administration says took out its leadership and targeted its ballistic-missile program.”

MANUFACTURING (MNI INTERVIEW): The U.S. manufacturing sector's ability to sustain early-year momentum into February provides some hope for the long-dormant sector, though continued tariff uncertainty is still weighing, Institute for Supply Management manufacturing chair Susan Spence told MNI.

FED (FT/BBG): "Federal Reserve Chair nominee Kevin Warsh would only seek to make changes to the the central bank’s balance sheet after extensive talks on its potential effects with banks and the broader public, Financial Times reports, citing unidentified people familiar with his thinking."

JAPAN

FX (BBG): “ Japan is monitoring financial markets with the utmost vigilance and will take any necessary action in response to sharp movements, Finance Minister Satsuki Katayama said, as volatility intensifies following the US and Israeli attack on Iran. “

OTHER

SAUDI ARABIA (BBG): “Two drones struck near the US Embassy in Riyadh, pulling Saudi Arabia into a widening conflict among Iran, the US and Israel, and prompting President Donald Trump to vow retaliation.”

MIDDLE EAST (BBG): “The United Arab Emirates and Qatar are privately lobbying allies to help them persuade President Donald Trump to reach for an off-ramp that would keep US military operations against Iran short, according to people familiar with the matter.

AUSTRALIA (BBG): “ Australia’s central bank chief Michele Bullock issued a warning Tuesday that the interest-rate setting board’s patient approach to inflation has its limits and that policy could be tightened again as soon as two weeks’ time.”

CHINA

US/CHINA (BBG): “US and Chinese trade negotiators are slated to meet in mid-March, according to people familiar with the matter, signaling a planned summit between Donald Trump and Xi Jinping is pushing ahead despite American strikes against Iran.”

US/CHINA (BBG): “ US officials are considering caps on the number of AI accelerators Nvidia Corp. can export to any one Chinese company, which would further constrain the chipmaker’s reentry into a crucial market.”

LNG (YICAI): “The current Middle East conflict poses an overall controllable LNG supply shock to China in the short term, industry insiders told Yicai.”

LNG/IRAN (BBG): "Senior gas executives say China is pressuring Iranian officials to avoid action that would disrupt Qatari gas exports or other energy shipments making their way through the Strait of Hormuz, a key maritime chokepoint."

NPC (21st CENTURY BUSINESS HERALD): “Delegates to the National People’s Congress this week are expected to focus on expanding domestic demand and boosting consumption, the 21st Century Business Herald reported.”

MNI: PBOC Net Drains CNY491.7 Bln via OMO Tuesday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY34.3 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net drain of CNY491.7 billion after offsetting the maturity of CNY526 today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4441% at 09:55 am local time from the close of 1.4639% on Monday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 46 on Monday, compared with the close of 49 on Friday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Lower At 6.9088 Tues; +5.60% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 6.9088 on Tuesday, compared with 6.9236 set on Monday. The fixing was estimated at 6.8839 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND JAN BUILDING PERMITS M/M 1.9%; PRIOR -4.5%

AUSTRALIA Q4 NET EXPORTS OF GDP PPTS -0.1; MEDIAN -0.3; PRIOR -0.1

AUSTRALIA Q4 BOP CURRENT ACCOUNT BALANCE -A$21.1bn; MEDIAN -A$16.5bn; PRIOR -A$18.3bn

AUSTRALIA JAN BUILDING APPROVALS M/M -7.2%; MEDIAN 5.0%; PRIOR -14.9%

JAPAN JAN JOBLESS RATE 2.7%; MEDIAN 2.6%; PRIOR 2.6%

JAPAN JOB-TO-APPLICANT RATIO 1.18; MEDIAN 1.20; PRIOR 1.20

JAPAN Q4 CAPEX Y/Y 6.5%; MEDIAN 3.0%; PRIOR 2.9%

JAPAN Q4 CAPEX EX SOFTWARE Y/Y 7.3%; MEDIAN 3.9%; PRIOR 2.9%

JAPAN Q4 COMPANY PROFITS Y/Y 4.7%; MEDIAN 3.0%; PRIOR 19.7%

JAPAN Q4 COMPANY SALES Y/Y 0.7%; PRIOR 0.5%

JAPAN FEB MONETARY BASE Y/Y -10.6%; PRIOR -9.5%

SOUTH KOREA FEB S&P GLOBAL PMI Mfg 51.1; PRIOR 51.2

MARKETS

US TSYS: Inflation Fears Grip; Watch for 10-Yr to Test 4.10%

The sell off in USTs followed through into Asia Tuesday with the 10-Yr bond future down -01 at 113-01 with volumes relatively high, suggesting decent two way flow.

Cash was weaker again after the overnight lead in with yields up 1 - 2bps. Fears over inflationary pressures are driving yields higher with longer dated treasuries (the most sensitive to inflation) underperforming.

- The 2-Yr was up +0.8bps at 3.486%

- The 5-Yr was up +1.4bps at 3.626%

- The 10-yr was up +1.9bps at 4.057%

- The 30-Yr was up +2.7bps at 4.709%

YIelds remain towards the bottom of the 1 month range, suggesting that there is ample room for further rises. Look for the 10-Yr to test 4.10% in the coming sessions.

Tuesday Calendar:

- 03/03 -- Wards Total Vehicle Sales

- 03/03 0955 NY Fed Williams moderates discussion

- 03/03 1130 US TSY - $90B 6W bill auction

- 03/03 1155 MN Fed Kashkari Bbg investment confernce

Source: Bloomberg Finance L.P. / MNI

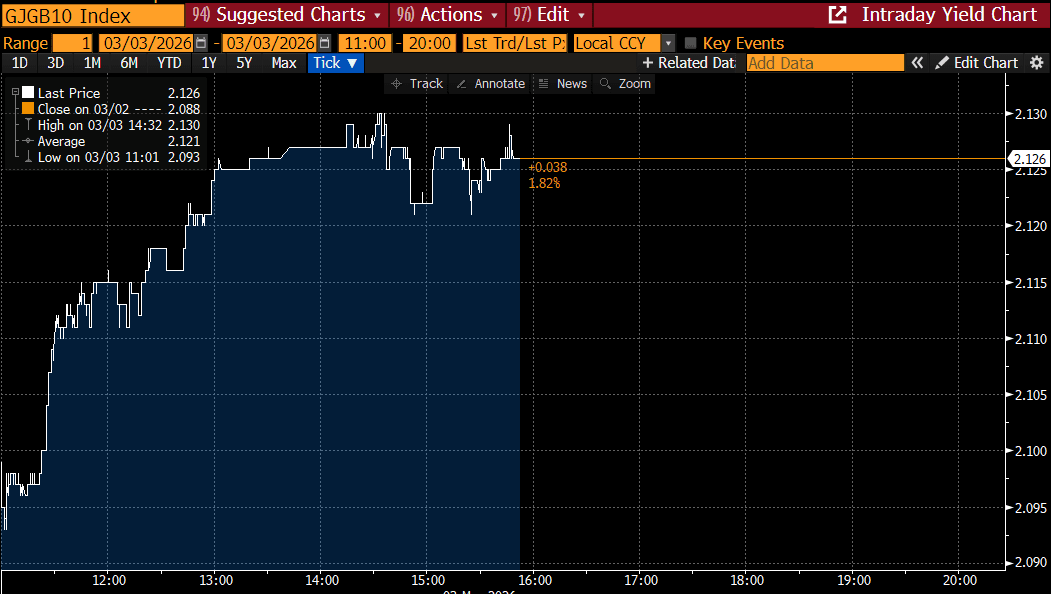

JGBS: At Session Cheaps After 10Y Auction Shows Mixed Results

JGB futures are sharply weaker and at session lows, -64 compared to settlement levels, after today's 10-year supply.

- (Bloomberg) " The Iran war is rekindling inflation concerns across financial markets, sapping the outlook for global bonds. Traders have offloaded government debt since Monday as they game-plan how a prolonged conflict in the Middle East may ramp up oil and supercharge inflation."

- The 10-year JGB auction delivered mixed results, with the low price failing to meet expectations at 99.77, according to the Bloomberg dealer poll. However, the cover ratio increased to 3.3043x from 3.0196x. The tail also lengthened slightly to 0.06 from 0.05.

- This performance came with an outright yield that was 10-15bps below than the level of last month's auction and ~25bps lower that the cycle high. The 2s/10s yield curve was also ~10bps flatter last month’s auction and around 35bps below its a cycle high.

- Cash US tsys are flat to 3bps cheaper, with a steepening bias, in today’s Asia-Pac session after yesterday’s heavy losses.

- Cash JGBs are 2-6bps cheaper across benchmarks out to the 30-year, and 1.5bps richer beyond.

- Swap rates are 1-3bps higher.

- Tomorrow, the local calendar will see S&P Global Composite & Services PMIs and Consumer Confidence Index.

Source: Bloomberg Finance LP

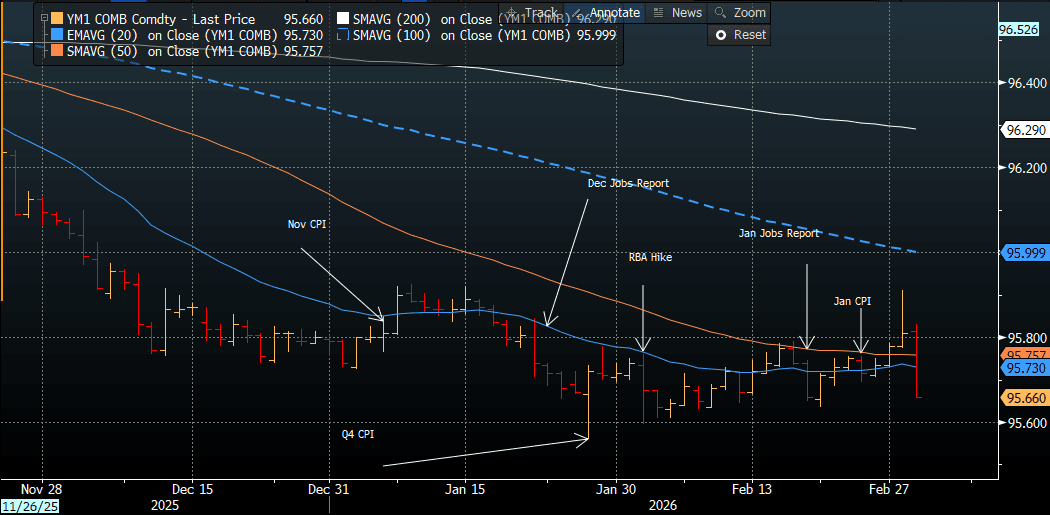

AUSSIE BONDS: Sharply Weaker With Global Bonds, RBA Gov Comments Also Weigh

ACGBs (YM -10.0 & XM -9.0) are sharply weaker in line with global bonds, as the haven bid sparked by the weekend's US and Israel strikes on Iran faded.

- The market was also under pressure following RBA Governor Bullock’s comments today. In the Q&A after today’s speech, she noted that every central meeting is live and that she didn't want people to assume that the central bank would only move after quarterly inflation prints.

- The latest ACGB Mar-47 auction saw strong demand, with the weighted average yield coming in 0.99bps through mid-yields. Moreover, the cover ratio was high at 4.7167x. The AOFM plans to sell A$900mn of the 4.75% 21 October 2037 bond on Wednesday and A$800mn of the 1.50% 21 June 2031 bond on Friday.

- Cash US tsys are flat to 2bps cheaper, with a steepening bias, in today’s Asia-Pac session after yesterday’s heavy losses.

- Cash ACGBs are 8-10bps cheaper with the AU-US 10-year yield differential at +68bps.

- The bills strip has bear-steepened, -5 to -9.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 30% for March to 121% by June and 182% by December 2026.

- Tomorrow, the local calendar will see Q4 GDP.

Bloomberg Finance LP

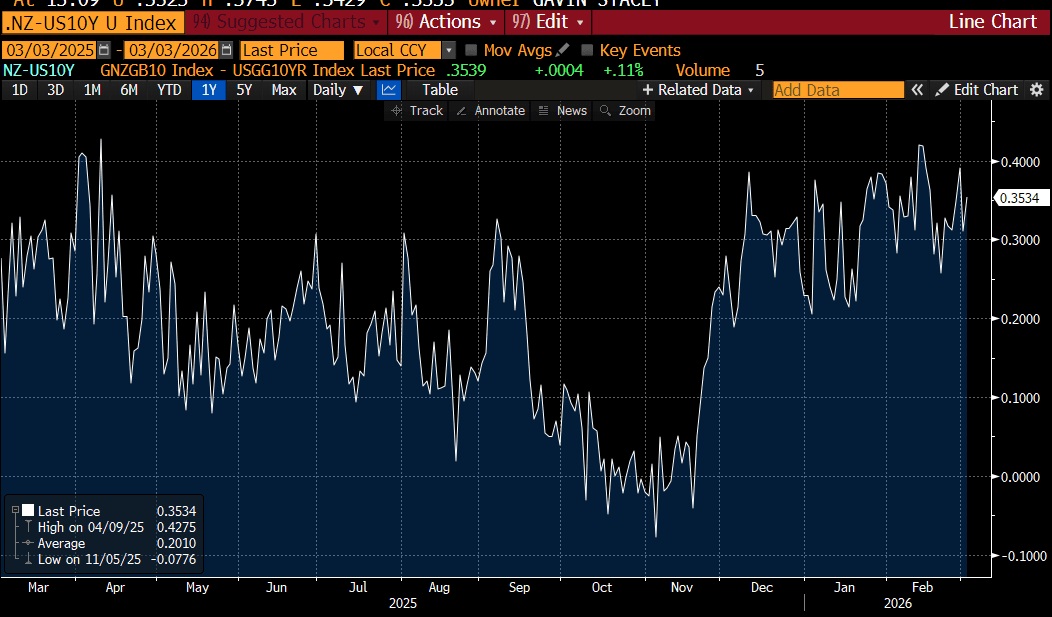

BONDS: NZGBS: Cheaper With Global Bonds Haven Bid Is Unwound

NZGBs closed 4–5bps cheaper in line with global bonds, as the haven bid sparked by weekend strikes — with the United States and Israel attacking Iran early Saturday — faded amid a sharp rise in oil prices and renewed inflation concerns.

- In relative terms, NZ-US and NZ-AU 10-year yield differentials closed 1bp and 3bps lower, respectively.

- (Bloomberg) “RBNZ Governor Anna Breman will deliver a keynote speech to Business NZ’s CEO Forum in Auckland on March 24. The speech will touch on the current economic outlook, drawing on insights from the February Monetary Policy Statement. Chief Economist Paul Conway will deliver a speech to the Financial Adviser Conference on March 25.”

- NZ Finance Minister Willis, in response to questions, said history suggests that global conflict tends to cause short term volatility in markets, but that over time they settle back close to previous level. - BBG

- Swap rates closed 3-4bps higher.

- RBNZ-dated OIS pricing closed little changed across meetings. No tightening is priced for April, while December 2026 assigns 31bps.

- Tomorrow, the local calendar will see Terms of Trade and ANZ Commodity Price data.

- On Thursday, the NZ Treasury plans to sell NZ$250mn of the 1.50% May-31 bond and NZ$200mn of the 4.5% May-35 bond.

Bloomberg Finance LP

FOREX: USD - BBDXY Looking To Challenge 1195-1200

The BBDXY has had a range today of 1195.13 - 1196.96 in the Asia-Pac session; it is currently trading around 1196. The BBDXY built on the move that started in Asia yesterday as the USD pushed higher, challenging the 1195-1200 resistance. The market has been very bearish the USD especially against EM so it was interesting to see the USD remain well supported against EM and Oil affected currencies, even as US stocks reversed their earlier losses to close flat on the day. The market is not positioned for this, especially in EM where liquidity is at a premium. USD/Asia has moved higher today led by USD/KRW(+1.61%). On the day, watch to see if the USD can continue to build on this strong start to the week and potentially break above the important 1195-1200 area in the coming days. A sustained break above 1200 could potentially signal a deeper pullback.

- EUR/USD - Asian range 1.1683-1.1707, Asia is currently trading 1.1690. The pair remained heavy as the USD built on its gains and oil added to the pair's headwinds. The price does not look great for the bulls now and a sustained close below 1.1700 could signal the potential for a deeper pullback toward the 1.1400-1.1500 area. On the day, having clearly broken out of its recent range I would be looking for rallies to now be faded initially. The first sell-zone is back toward 1.1725-1.1745 and then the 1.1800 area, looking for the move lower to now build for a potential test back toward 1.1500.

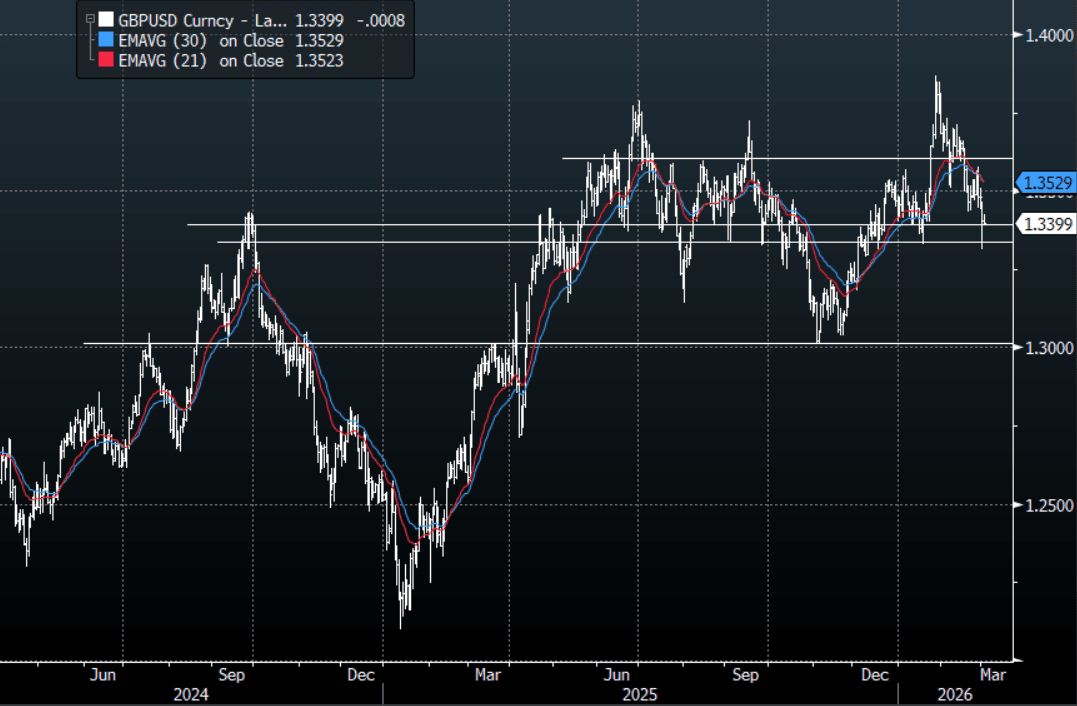

- GBP/USD - Asian range 1.3392-1.3425, Asia is currently dealing around 1.3400. GBP broke through 1.3400 and collapsed lower but could not maintain the move and is back around the breakout level once more. It really needs to hold above the pivotal 1.3300 area for any chance of a base to form. On the day, I suspect rallies toward 1.3450-1.3500 will continue to be faded as the USD looks to build on its gains. Sellers will be looking for the 1.3300 to be challenged, a break could signal a potential top is on place.

- Cross asset : SPX -0.65%, Gold $5375, US 10-Year 4.045%, BBDXY 1196, Crude Oil $62.62

- Data/Events : 11:00 a.m.: Italy February CPI, 11:00 a.m.: Eurozone February CPI, 3:55 p.m.: Fed’s Williams Speaks, 4:30 p.m.: ECB’s Kocher Speaks, 4:40 p.m.: ECB’s Sleijpen Speaks, 5:45 p.m.: Fed’s Kashkari Speaks, UK Chancellor Rachel Reeves delivers her Spring Statement.

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

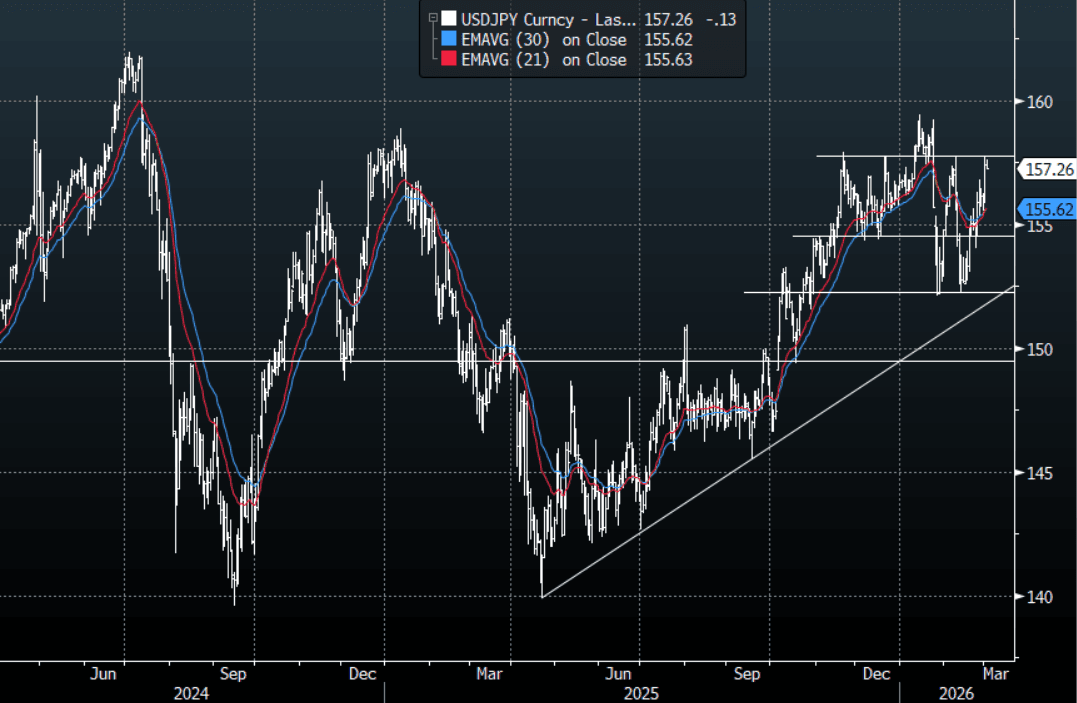

JPY: USD/JPY - Consolidates Gains As It Looks To Test 157.50-158.00

The USD/JPY range today has been 157.18-157.60 in the Asia-Pac session, it is currently trading around 157.25, -0.10%. USD/JPY has been consolidating its recent gains as it looks to challenge this 157.50-158.00 area. The days of the Yen being a safe-haven looks like they have passed, and the momentum higher has been re-asserted as it reacts to the combination of higher oil and a reinvigorated USD. The Yen has even underperformed in the crosses in this environment which just underlines its current malaise. On the day, with the upward momentum reasserted dips are likely to again be supported, first support is back toward 156.40-156.80 and then 155.50. A break above 158.00 and the market will again be looking toward the 160.00 area and then beyond. Expect the jaw-boning by officials to get louder but for now I think we are still a fair way away from them getting involved.

- "JAPAN FINMIN KATAYAMA: HAVING SEEN DOLLAR BEING BOUGHT AS SAFE HAVEN CURRENCY. WILL TAKE APPROPRIATE ACTION WHEN MONITORING SITUATIONS. INTERVENTION IS INCLUDED IN THE JOINT STATEMENT WITH US LAST YEAR” - [RTRS]

- MNI AU - Japan Unemployment Rate & Job-To-Applicant Ratio Show Weaker Trends: Japan's Jan jobless rate edged up to 2.7%, versus a 2.6% forecast (which was also the prior outcome). The job-to-applicant ratio fell to 1.18, versus 1.20 forecast (which was also the prior outcome). The focus will be on improving the growth outlook, which is a key focus point for the Takaichi government. A softening labour market backdrop points to less upside pressure in wage outcomes.

- "TAKAICHI: CHANCE OF SUPPLEMENTARY BUDGET ISN'T ZERO" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 155.00($532m), 155.50($699m), 157.00($1.36b). Upcoming Close Strikes : 153.00($1.16b March 5), 153.25($1.27b March 6) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 128 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

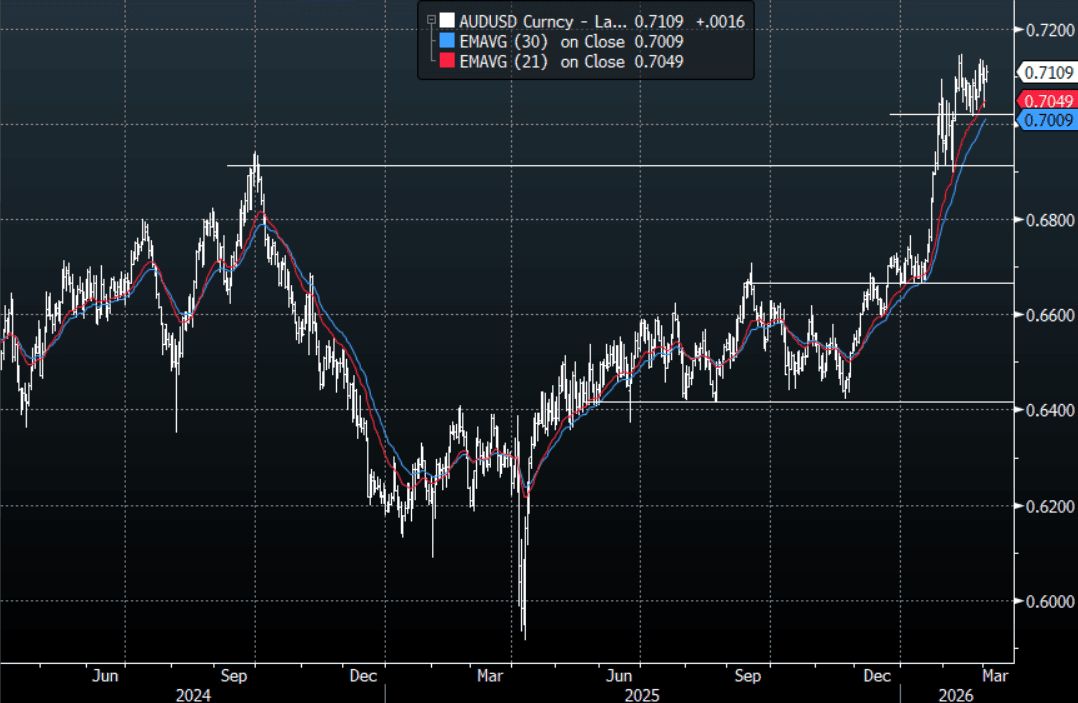

AUD/USD - Bullock Adds Tailwind To AUD Demand As It Holds Above 0.7100

The AUD/USD has had a range today of 0.7087-0.7123 in the Asia- Pac session, it is currently trading around 0.7110,+0.25%%. The AUD has continued its impressive ability to ignore the turmoil happening in the market as it continues to outperform particularly in the crosses, Bullock's speech added to the support. Asian markets got hit hard today being led by a large collapse in the KOSPI which was down over 5% at one point. The AUD has been a favoured long and continues to see strong buying on dips. On the day, it looks like 0.7040-0.7120 as the market tries to get a handle on the geopolitical fallout. A sustained break below 0.7000 is needed to signal a potential deeper pullback, but back above 0.7120-0.7130 and the bulls will have regained control and they would be looking to retest the pivotal 0.7150/0.7200 area.

- MNI AU - RBA-Dated OIS Firms After RBA Governor Speech And Q&A: RBA-dated OIS are firmer today after RBA Governor Bullock, in the Q&A after today's speech, noted that every central meeting is live and that she didn't want people to assume that the central bank would only move after quarterly inflation prints.

- MNI AU - AU Net Export Drag To Q4 GDP Less Than Forecast, Govt Spend To Add: Australia's Q4 net exports contribution to GDP cut -0.1pps off growth, the same as the Q3 drag. The market expected a -0.3ppts drag, so a slightly better than expected outcome. The ABS also notes that total public demand will contribute 0.3ppt to Q4 growth. This comes ahead of tomorrow's Q4 GDP print. The market consensus is a 0.7%q/q rise (prior 0.4%) and y/y pace of 2.2% (prior 2.1%). The q/q forecast range is 0.5-1.0% at this stage. The focus will be on the domestic demand impulse, particularly as the economy bumps up against capacity constraints.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6934(AUD830m), 0.6950(AUD551m), 0.7020(AUD585m). Upcoming Close Strikes : 0.6950(AUD933m Mar 5), 0.7000(AUD1.39b Mar 5), 0.7150(AUD1.35b Mar 5) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 65 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

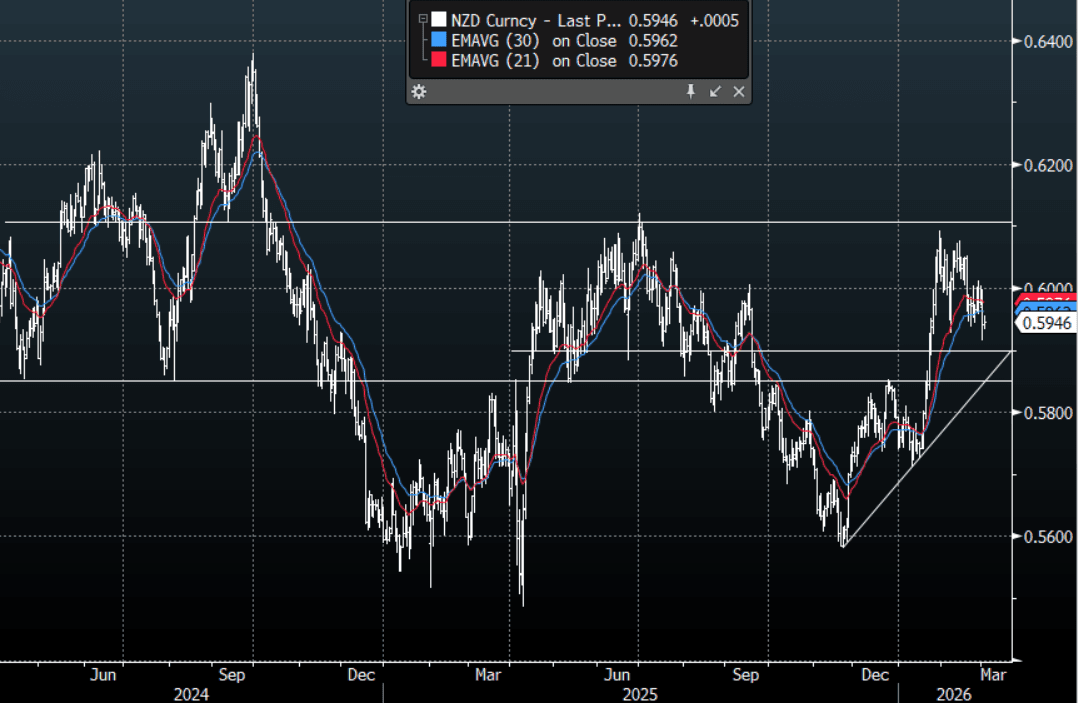

NZD/USD-Trades In The Middle Of Its Range, Albeit With A Heavy Tone

The NZD/USD had a range today of 0.5934-0.5956 in the Asia-Pac session, it is currently trading around 0.5945. The NZD has traded sideways still within its recent range even as Asia saw risk come under big pressure with the KOSPI leading the move lower. The pivotal resistance toward 0.6100-0.6150 continues to cap for now and the dovish read of the RBNZ has delayed its challenge in the short-term and the global turmoil has just added to its headwinds. On the day, price still remains in its 0.5885-0.6015 range albeit with a heavy tone. I suspect rallies will continue to be faded while the USD gets bought as a safe haven, a sustained break below 0.5885/0.5900 could potentially signal a deeper pullback.

- MNI AU - NZ Jan Jobs Filled Up, But Stop/Start Nature Of Job Rises Continues: The stop/start nature of the NZ jobs recovery continued in Jan. Filled jobs rose 0.2%m/m, after a revised 0.3% fall in Dec (which was originally reported as a flat outcome). In y/y terms filled jobs were down 0.2%. The m/m profile has been -0.2% in Oct last year, +0.5% in Nov, -0.3% in Dec and now +0.2% in Jan. Hence there isn't clear signs of a consistent pick up in labour demand. This will feed into RBNZ thinking around holding rates lower as it waits for firmer evidence of economic recovery feeding into the labour market (before it tightens rates). The central bank did state at its last meeting that a rate hike was possible by year end but this wasn't set in stone in terms of its OCR outlook.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5950(NZD894m March 5), 0.6000(NZD322m March 6) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 53 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: KOSPI Back Below 6k; Regional Tourism, Travel, Autos all Struggle

As Korea reopened after yesterday's holiday the catch up was brutal with falls of -5.2%, taking the KOSPI back below 6,000. High flying AI stocks which are up 50-60% year to date fell heavily with SK Hynix down over 8% and Samsung Electroncis 9%. The euphoria for AI tech stocks has seen retail buying in South Korean tech stocks increase significantly in 2026, marking a reversal from the heavy selling seen in 2025. Investors have been encouraged by authorities to redirect capital away from US tech into local names to support the industry.

China's bourses are all down despite earlier attempts by the Hang Seng to rally. Falls are modest for the major indexes, the exception being the tech heavy Shenzhen down -1.3%. Technology & Semiconductor names saw sharp losses. Investors are pivoting away from growth-heavy tech stocks due to fears that rising energy costs will fuel global inflation, potentially delaying anticipated interest rate cuts.

Oil price rises hit the NKY today with airlines and autos hit hard whilst refiners fell over 5% on news that the Straits of Hormuz was shut. Banks continued where they left off Monday with heavy falls whilst defense stocks saw a sharp reversal as traders locked in profits after massive gains on hopes of increased military spending.

SE Asian bourses are outperforming the region today with modest gains. The FTSE Malay is up +0.8% given the surge in oil prices dragging Singapore, and Jakarta with it. The SE Thai in Malaysia ignored the signals falling as rising oil prices are expected to hit an already struggling tourist industry.

OIL: Brent Nears $80, US Strikes Set to Intensify

- After declining modestly at the open, oil prices have surged throughout the day in Asia with the rapid escalation of conflict in the Middle East following U.S. and Israeli strikes on Iran over the weekend.

- The most critical factor is the effective closure of the Strait of Hormuz, a narrow waterway through which roughly 20% of the world's daily oil supply (approximately 20 million barrels) flows. Reports of drone strikes damaging Amazon data centres and other critical infrastructure in the region have further spooked markets. Two drones struck near the US Embassy in Riyadh, pulling Saudi Arabia into a widening conflict among Iran, the US and Israel, and prompting President Donald Trump to vow retaliation.

- WTI opened lower in the Asia trading day trading down to $70.41 before a mid morning surge up to new intraday highs of US$72.77 bbl - a gain of +2.05%

- Brent had traded down at the open to $78.38 before strong gains saw it reach US$79.74 bbl - a gain of +2.6%.

- Senior U.S. officials have indicated that a significant expansion of strikes targeting Iranian missile and naval assets is prepared for the next 24 hours which could see further, significant appreciation of prices as Trump vows 'Whatever it Takes'

Gold Nears January Highs, Readies Test of $5,400 Again

- Gold has traded in a $5,329 - $5,380 range Tuesday drawing close to the January high of $5,417.

- Currently near 5,367 / 5,369 gold has gained +0.80% Tuesday as it appears ready to test $5,400 again having failed in its attempt Monday.

- Following the January 28 high gold fell almost 14%, sending shockwaves through commodity markets and sending multiple online trading platforms bust.

- Singapore is intensifying its focus of being a regional gold hub, tapping local and international banks including JPMorgan Chase & Co. and UBS Group AG to help boost liquidity and make the most of demand from wealthy investors. (per BBG)

- Hong Kong’s Mandatory Provident Fund Schemes Authority is looking into allowing mandatory retirement funds’ investment in gold-backed exchange-traded funds, Sing Tao Daily reports, citing Chairwoman Ayesha Macpherson Lau as saying during a committee meeting at the city’s legislature. (per BBG).

- The gold-to-oil ratio is currently at a historically extreme level of approximately 75:1, nearly five times the long-term historical average of 16:1. Historically, when this ratio exceeds 30:1, it tends to revert violently. For the ratio to normalize to its 16:1 average with gold at current levels, oil would need to almost quadruple.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 03/03/2026 | 0700/0200 | * | Turkey CPI | |

| 03/03/2026 | 0745/0845 | Budget Balance | ||

| 03/03/2026 | 1000/1100 | *** | EZ HICP Flash | |

| 03/03/2026 | 1000/1100 | *** | EZ HICP Flash | |

| 03/03/2026 | 1000/1100 | *** | EZ HICP Flash | |

| 03/03/2026 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 03/03/2026 | 1000/1100 | *** | EZ HICP Flash (2dp) | |

| 03/03/2026 | 1000/1100 | *** | Italy Flash Inflation | |

| 03/03/2026 | - | OBR Spring Forecast | ||

| 03/03/2026 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 03/03/2026 | 1455/0955 | New York Fed's John Williams | ||

| 03/03/2026 | 1510/1010 | Kansas City Fed's Jeff Schmid | ||

| 03/03/2026 | 1655/1155 | Minneapolis Fed's Neel Kashkari | ||

| 04/03/2026 | 2200/0900 | * | S&P Global Final Australia Services PMI | |

| 04/03/2026 | 2200/0900 | ** | S&P Global Final Australia Composite PMI | |

| 04/03/2026 | 0030/1130 | *** | Quarterly GDP | |

| 04/03/2026 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 04/03/2026 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 04/03/2026 | 0130/0930 | *** | CFLP Manufacturing PMI | |

| 04/03/2026 | 0130/0930 | ** | CFLP Non-Manufacturing PMI | |

| 04/03/2026 | 0145/0945 | ** | S&P Global Final China Services PMI | |

| 04/03/2026 | 0145/0945 | ** | S&P Global Final China Composite PMI | |

| 04/03/2026 | 0145/0945 | ** | S&P Global Final China Manufacturing PMI | |

| 04/03/2026 | 0730/0830 | *** | CPI | |

| 04/03/2026 | 0815/0915 | ** | S&P Global Services & Composite PMI (f) | |

| 04/03/2026 | 0845/0945 | ** | S&P Global Composite & Services PMI (f) | |

| 04/03/2026 | 0850/0950 | ** | S&P Global Composite & Services PMI (f) | |

| 04/03/2026 | 0855/0955 | ** | S&P Global Composite & Services PMI (f) | |

| 04/03/2026 | 0900/1000 | ** | S&P Global Composite & Services PMI (f) | |

| 04/03/2026 | 0900/1000 | Unemployment | ||

| 04/03/2026 | 0930/0930 | ** | S&P Global Composite & Services PMI (Final) | |

| 04/03/2026 | 1000/1100 | ** | EZ PPI | |

| 04/03/2026 | 1000/1100 | ** | EZ Unemployment | |

| 04/03/2026 | 1000/1100 | *** | GDP (f) | |

| 04/03/2026 | 1045/1145 | ECB Cipollone Panel at European Investment Bank Group Forum | ||

| 04/03/2026 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 04/03/2026 | - | Chinese People's Political Consultative Conference | ||

| 04/03/2026 | 1330/1430 | ECB de Guindos Remarks at American Academy, Berlin |