MNI EUROPEAN OPEN: Hong Kong COVID Restriction Rollback Rumours Do The Rounds

EXECUTIVE SUMMARY

- CHINA ASKS INSURERS TO BUY BONDS AS RETAIL INVESTORS PULL BACK (BBG)

- MOST CHINESE MAY END UP WITH COVID, SENIOR HEALTH ADVISER WARNS (BBG)

- CHINA HEALTH OFFICIALS TO HOLD PRESS CONFERENCE ON COVID MEASURES (RTRS)

- HONG KONG MAY END OUTDOOR MASK RULE, RELAX COVID TESTS, REPORT SAYS (BBG)

- AUSTRALIA’S TREASURER SAYS RBA REVIEW TO GUIDE LOWE DECISION (BBG)

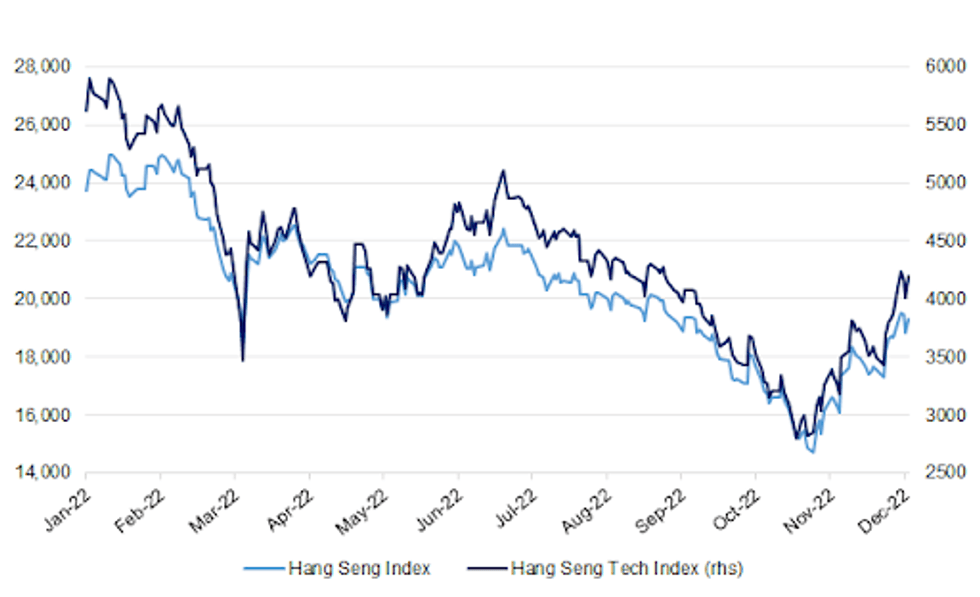

Fig. 1: Hang Seng & Hang Seng Tech Indices

Source: MNI - Market News/Bloomberg

UK

FISCAL: Britain’s biggest business group has urged ministers to quickly decide which industries will receive energy support from next spring as hundreds of companies brace for their bills to more than double. (Guardian)

ECONOMY: Britain's labour market cooled noticeably last month, with demand for staff and pay growth easing, and staff shortages became less acute, a survey showed on Thursday. (RTRS)

ECONOMY/POLITICS: The government is exploring the idea of significantly restricting or even banning the right of ambulance workers and firefighters to go on strike. (BBC)

PROPERTY: The Treasury and the Financial Conduct Authority have told lenders to act flexibly if their customers get into difficulties repaying their mortgages, as the UK looks to soften the impact of rising interest rates and a spluttering economy. (BBG)

EUROPE

ECB: European Central Bank staff will discuss protest action and even potential strikes after rejecting a pay offer well below the rate of eurozone inflation, a union official has warned. (FT)

EU: The Polish government will “quickly” push through legislation to meet the European Union’s demands on judicial independence if it secures guarantees from Brussels, a top official said. (BBG)

U.S.

ECONOMY: Treasury Secretary Janet Yellen and members of the Global Business Alliance discussed the domestic and world economic recovery, according to a readout from the department. (BBG)

ECONOMY: The U.S. economy is showing “continued resilience” despite a predictable slowdown, a top White House economic advisor said Wednesday. (CNBC)

INFLATION: Wholesale prices of used vehicles reached their lowest level in more than a year last month, as retail sales decline amid interest rate hikes, rising new vehicle availability and recessionary fears. (CNBC)

EQUITIES: Elon Musk’s bankers are considering providing the billionaire with new margin loans backed by Tesla Inc. stock to replace some of the high-interest debt he layered on Twitter Inc., according to people with knowledge of the matter. (BBG)

OTHER

GLOBAL TRADE: Dutch officials are planning new controls on exports of chipmaking equipment to China, according to people familiar with the matter, potentially aligning their trade rules with US efforts to restrict Beijing’s access to high-end technology. (BBG)

JAPAN: Managers at nearly two-thirds of Japanese companies have lost confidence in the administration of Prime Minister Fumio Kishida, citing dissatisfaction over his effectiveness and handling of inflation, according to a Reuters monthly survey. (RTRS)

RBA: Australian Treasurer Jim Chalmers said an independent review of the Reserve Bank will help guide his decision next year on whether to reappoint Governor Philip Lowe, whose term expires in September. (BBG)

RBA: The RBA has said in its submission to the Review into the central bank that it believes that flexible inflation targeting remains "appropriate" and that it regularly looks at other policy frameworks. It also believes that the 2-3% target band should not be changed as that could "damage long-term credibility if it were not done in an appropriate way". (MNI)

NEW ZEALAND: New Zealand's Fonterra Co-operative Group Ltd on Thursday lowered its farmgate milk price forecast range for the second time for the 2022/23 season on higher costs and softening demand for whole milk powder. (RTRS)

BOK: South Korea's central bank said on Thursday it would change its aggressive policy tightening stance when it becomes more certain that inflation and economic growth are slowing, without giving any hint on the likely timing. (RTRS)

BOK: The Bank of Korea is ready to provide more liquidity to stabilize short-term money markets if needed, said Deputy Governor Lee Sang-hyeong, after credit markets there became strained following a surprise default by a developer earlier this year. (BBG)

SOUTH KOREA: Prime Minister Han Duck-soo said Thursday that the government issued an order for striking truckers serving the petrochemical and steel industries to return to work, as their strike entered its 15th day amid growing disruptions of supply chains. (Yonhap)

SOUTH KOREA: South Korean government asked National Pension Service to carry out FX hedging on 10% of its overseas investment, in an effort to help stabilize the won, Maeil Business Newspaper says, citing unidentified investment banking sources. (BBG)

HONG KONG: Hong Kong is considering scrapping its outdoor mask mandate as part of a suite of major relaxations in the city’s Covid rules, pro-China newspaper Wen Wei Po reported. (BBG)

CANADA: The Canadian government is proposing to toughen scrutiny of foreign takeovers, citing national security concerns, just weeks after a new Indo-Pacific policy identified China as an “increasingly disruptive” power. (Globe & Mail)

MEXICO: Mexico's financial system has a resilient and solid position despite global economic and market volatility, the country's central bank said on Wednesday during the launch of its financial stability report. (RTRS)

MEXICO: Mexican central bank deputy governor Gerardo Esquivel has a fair chance of keeping his job once his term expires at the end of the year, as the government is more open to renominating him than it had initially signaled, people with knowledge of the matter said. (BBG)

MEXICO: Mexico has submitted proposals aimed at resolving a sizeable part of an energy dispute with the United States, and wants to give companies confidence they can invest in the country, the economy ministry said on Wednesday. (RTRS)

BRAZIL: Brazil's central bank on Wednesday kept interest rates at 13.75% for the third consecutive policy decision, highlighting fiscal uncertainties arising from a spending boost planned by leftist President-elect Luiz Inacio Lula da Silva. (RTRS)

BRAZIL: Brazilian President-elect Luiz Inacio Lula da Silva's transition team believes it's necessary to reform how state-run development bank BNDES charges interest rates to lenders, a change that could dilute the impact of the central bank's rate-setting decisions. (RTRS)

BRAZIL: Brazil's Senate approved on Wednesday a constitutional amendment to increase the government spending cap, allowing the incoming administration of President-elect Luiz Inacio Lula da Silva to fund an extension of social welfare payments for poor families. (RTRS)

RUSSIA: Ukrainian officials and lawmakers have in recent months urged the Biden administration and members of Congress to provide the Ukrainian military with cluster munition warheads, weapons that are banned by more than 100 countries but that Russia continues to use to devastating effect inside Ukraine. (CNN)

RUSSIA: The risk of Russian President Vladimir President Putin using nuclear weapons as part of his war in Ukraine has decreased in response to international pressure, German Chancellor Olaf Scholz said in an interview published on Thursday. (RTRS)

RUSSIA: European Union officials proposed a new round of sanctions on Russia on Wednesday over its invasion of Ukraine, including a ban on exports of drone engines to Russia and other potential suppliers of the machines to its military, a prohibition on investing in Russia’s mining sector and new financial restrictions. (WSJ)

RUSSIA: Consumer prices in Russia rose sharply in the week to Dec. 5, driven by higher electricity and gas tariffs, data published on Wednesday showed, a little over a week before the central bank will meet on interest rates for the final time this year. (RTRS)

SOUTH AFRICA: Power plant breakdowns at South Africa’s state power utility are at the highest in at least a year, affecting two-fifths of generation capacity and exacerbating outages that are hindering economic growth. (BBG)

PERU: Peru has a female president for the first time, after ex-president Pedro Castillo was impeached - hours after he tried to dissolve parliament. (BBC)

PERU: Peru's central bank increased its benchmark interest rate 25 basis points to 7.5% on Wednesday, the 17th consecutive hike as monetary policymakers in the copper-producing Andean nation battle stubbornly high inflation. (RTRS)

METALS: The London Metal Exchange has attracted takeover interest from rivals as the historic institution wrestles with its future in the wake of March’s nickel crisis. (BBG)

OIL: U.S. Deputy Treasury Secretary Wally Adeyemo told Turkish Deputy Foreign Minister Sedat Onal in a call on Wednesday that the price cap on Russian oil does not necessitate additional checks on ships passing through Turkish territorial waters, the U.S. Treasury Department said. (RTRS)

OIL: Transit times for oil tankers to cross the Turkish Straits from the Black Sea to the Mediterranean have jumped to the highest in a year amid a spat over recent Turkish demands for proof of insurance cover ahead of the G7 price cap on Russian crude. (Platts)

OIL: Amos Hochstein, Special Presidential Coordinator for Global Infrastructure and Energy Security, told Bloomberg today the Administration's plans for refilling the Strategic Petroleum Reserve, what to make of record profits by energy producers and how the administration is pivoting for China's reopening. (BBG)

CHINA

CORONAVIRUS: China’s health authorities will hold a press conference on COVID-19 prevention and control measures at 3 p.m. local time (0700 GMT), an official notice said on Thursday. (RTRS)

CORONAVIRUS: The vast majority of China’s population may eventually contract Covid-19, a senior health-policy adviser warned, as Beijing makes concerted steps toward dismantling its zero-tolerance approach to the virus and living with higher case levels. (BBG)

BONDS: Chinese regulators asked the nation’s biggest insurers to buy bonds being offloaded as retail customers pull their cash from fixed-income investments, according to people familiar with the matter. (BBG)

FISCAL: China may maintain relatively large deficits and debt next year to cope with weakening external demand and insufficient domestic demand, as the Politburo meeting this week called for a step up in proactive fiscal policy for 2023, Yicai.com reported. (MNI)

FOREX: China’s FX reserves increased 2.13% m/m in November to USD3.11 trillion, and are expected to remain stable in the near term, according to the Securities Daily. November's increase reflected changes in asset prices and favorable conversion of non-USD reserves into USD. (MNI)

PROPERTY: Leading property developers saw home sales recover in November amid intensive policy support to ease funding pressures, China Securities Journal reported. (MNI)

REITS: China will study expanding REITs pilot scheme to long- term rental properties and commercial real estate projects, China Securities Regulatory Commission Deputy Chairman Li Chao says at a forum via video. (BBG)

CHINA MARKETS

PBOC NET DRAINS CNY8 BILLION VIA OMOS THURSDAY

The People's Bank of China (PBOC) on Thursday injected CNY2 billion via 7-day reverse repos with the rates unchanged at 2.00%. The operation has led to a net drain of CNY8 billion after offsetting the maturity of CNY10 billion reverse repos today, according to Wind Information.

- The operation aims to keep liquidity reasonable and ample, the PBOC said on its website.

- The 7-day weighted average interbank repo rate for depository institutions (DR007) rose to 1.8833% at 9:29 am local time from the close of 1.6363% on Wednesday.

- The CFETS-NEX money-market sentiment index closed at 49 on Wednesday vs 45 on Tuesday.

PBOC SETS YUAN CENTRAL PARITY AT 6.9606 THURS VS 6.9975 WEDS

The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 6.9606 on Thursday, compared with 6.9975 set on Wednesday.

OVERNIGHT DATA

JAPAN Q3, F GDP -0.2% Q/Q; MEDIAN -0.3%; PRELIM -0.3%

JAPAN Q3, F GDP ANNUALISED -0.8% Q/Q; MEDIAN -1.0%; PRELIM -1.2%

JAPAN Q3, F NOMINAL GDP -0.7% Q/Q; MEDIAN -0.4%; PRELIM -0.5%

JAPAN Q3, F GDP PRIVATE CONSUMPTION +0.1% Q/Q; MEDIAN +0.3%; PRELIM +0.3%

JAPAN Q3, F GDP BUSINESS SPENDING +1.5% Q/Q; MEDIAN +1.6%; PRELIM +1.5%

JAPAN Q3, F GDP DEFLATOR -0.3% Y/Y; MEDIAN -0.5%; PRELIM -0.5%

JAPAN OCT BOP CURRENT ACCOUNT BALANCE -Y64.1BN; MEDIAN +Y621.7BN; SEP +Y909.3BN

JAPAN OCT ADJUSTED BOP CURRENT ACCOUNT BALANCE -Y609.4BN; MEDIAN +Y352.7BN; SEP +Y670.7BN

JAPAN OCT BOP TRADE BALANCE -Y1.8754TN; MEDIAN -Y1.8257TN; SEP -Y1.7597TN

JAPAN NOV BANK LENDING INCLUDING TRUSTS +2.7% Y/Y; OCT +2.6%

JAPAN NOV BANK LENDING EXCLUDING TRUSTS +3.0% Y/Y; OCT +3.0%

JAPAN NOV ECONOMY WATCHERS SURVEY CURRENT 48.1; MEDIAN 50.6; OCT 49.9

JAPAN NOV ECONOMY WATCHERS SURVEY OUTLOOK 45.1; MEDIAN 46.8; OCT 46.4

AUSTRALIA OCT TRADE BALANCE +A$12.217BN; MEDIAN +A$12.000BN; SEP +A$12.444BN

AUSTRALIA OCT EXPORTS -1% M/M; MEDIAN +1%; SEP +7%

AUSTRALIA OCT IMPORTS -1% M/M; MEDIAN +2%; SEP 0%

SOUTH KOREA NOV TOTAL BANK LENDING TO HOUSEHOLDS KRW1057.8TN; OCT KRW1058.8TN

UK NOV RICS HOUSE PRICE BALANCE -25%; MEDIAN -10%; OCT -2%

MARKETS

SNAPSHOT: Hong Kong COVID Restriction Rollback Rumours Do The Rounds

Below gives key levels of markets in the second half of the Asia-Pac session:

- Nikkei 225 down 135.61 points at 27550.79

- ASX 200 down 53.886 points at 7175.5

- Shanghai Comp. down 2.23 points at 3197.389

- JGB 10-Yr future down 13 ticks at 149.02, yield unchanged at 0.255%

- Aussie 10-Yr future down 1.0 tick at 96.635, yield up 1.00bp at 3.366%

- U.S. 10-Yr future down 0-12+ at 114-24+, yield up 4.16bp at 3.4585%

- WTI crude up $0.66 at $72.67, Gold down $3.05 at $1783.24

- USD/JPY up 37 pips at Y136.99

- CHINA ASKS INSURERS TO BUY BONDS AS RETAIL INVESTORS PULL BACK (BBG)

- MOST CHINESE MAY END UP WITH COVID, SENIOR HEALTH ADVISER WARNS (BBG)

- CHINA HEALTH OFFICIALS TO HOLD PRESS CONFERENCE ON COVID MEASURES (RTRS)

- HONG KONG MAY END OUTDOOR MASK RULE, RELAX COVID TESTS, REPORT SAYS (BBG)

- AUSTRALIA’S TREASURER SAYS RBA REVIEW TO GUIDE LOWE DECISION (BBG)

US TSYS: Cheapening Observed As Asia Fades NY Move

TYH3 deals at 114-26, -0-11, a little above the base of its 0-10+ session range, on volume of 115K. Cash Tsys run 0.5-4.0bp cheaper across the curve, with the belly leading the weakness. The 2-/10-Year yield spread hovers just off inverted cycle extremes, which were registered on Wednesday.

- With broader macro headline news flow on the light side, early overnight dealing saw Asia-Pac participants lean against Wednesday’s richening, with block sales in TY (-10,674) & FV (-3K) futures aiding the direction of travel. Other notable rounds of overnight flow included TY screen sales and demand for TY downside exposure via TYF3 114.00 puts and TYG3 111/110 put spreads.

- Reports pointing to the potential roll back of COVID restrictions in Hong Kong, fuelling a rally in Hong Kong equities, would have aided the cheapening momentum further.

- We have a light European docket, with comments from ECB’s Lagarde, Villeroy & de Cos slated. Further out, weekly initial jobless claims headline a thin NY calendar. Also note that both China & Hong Kong are scheduled to hold COVID related press conferences over the next couple of hours.

JGBS: Curve Twist Flattens

JGBs twist flattened, as the early catch-up bid in the longer end remained sticky (potentially pointing to life insurer/pension fund demand), while paper out to 7s struggled as U.S. Tsys softened in Asia-Pac hours.

- That leaves the major cash JGB benchmarks running 2bp cheaper 3bp richer, pivoting around 10s.

- 7s lead the shorter end the curve lower after futures more than unwound all of their overnight rally, leaving the contract -17 ahead of the bell.

- Local headline flow has been fairly subdued (final GDP and monthly BoP data headlined the data docket), with the broader impulse from swings in wider core global FI markets in the driving seat.

- The latest round of 5-Year JGB supply saw an uptick in the cover ratio (printing virtually in line with the 6-auction average of 3.59x), with the tail holding tight, while the low price matched wider dealer expectations (as proxied by the BBG poll). This suggested that outright yield levels were enough to promote smooth takedown of supply, although the previously alluded to speculation re: a BoJ policy tweak in ’23 likely capped demand.

- Looking ahead, Friday’s domestic docket is very limited, with only money stock and 3-month Bill supply due.

JGBS AUCTION: 5-Year JGB Auction Results

The Japanese Ministry of Finance (MOF) sells Y2.0309tn 5-Year JGBs:

- Average Yield: 0.121% (prev. 0.060%)

- Average Price: 99.90 (prev. 100.19)

- High Yield: 0.125% (prev. 0.064%)

- Low Price: 99.88 (prev. 100.17)

- % Allotted At High Yield: 18.5385% (prev. 80.1910%)

- Bid/Cover: 3.579x (prev. 3.306x)

JGBS AUCTION: 6-Month Bill Auction Results

The Japanese Ministry of Finance (MOF) sells Y3.26498tn 6-month Bills:

- Average Yield: -0.1322% (prev. -0.1148%)

- Average Price: 100.066 (prev. 100.057)

- High Yield: -0.1162% (prev. -0.1007%)

- Low Price: 100.058 (prev. 100.050)

- % Allotted At High Yield: 33.4036% (prev. 48.3438%)

- Bid/Cover: 4.109x (prev. 3.665x)

AUSSIE BONDS: Early Richening Gives Way

Aussie bonds finally gave way to the move lower in U.S. Tsys during Asia-Pac hours, as futures relinquished their overnight bid and cash ACGBs gave back their early catch-up richening. That left YM +1.0 & XM -1.0 at the bell, while wider cash ACGB trade saw the major benchmarks running 1bp richer to 1bp cheaper late on.

- Local data had little impact on the space, with a marginally wider than expected monthly trade surplus accompanied by softer than expected import and export prints.

- NSW TCorp sold a cumulative A$600mn of Apr-29, Feb-30 & March-31 paper, which could have applied some hedging pressure to XM futures early in the day.

- Local news flow saw Treasurer Chalmers note that a decision will be made whether to reappoint RBA Governor Lowe in mid-2023 after consultations with the PM and cabinet. Chalmers said that the RBA review, set to be published in March, will be "relevant" to the decision.

- Bills were -2 to +1 through the reds, while RBA dated OIS was little changed, pricing 16bp of tightening for the Bank’s Feb ’23 meeting, alongside a terminal cash rate of ~3.65%.

- Friday’s local docket will be headlined by the release of the weekly AOFM issuance slate and A$700mn of ACGB Nov-25 supply.

NZGBS: Firm Demand At Auctions Helps Support Space

NZGBS were a little more resilient than U.S. Tsys after adjusting to Wednesday’s firming in core global FI markets. The major benchmarks were 2bp cheaper to 4bp richer at the close, withs 2s a touch cheaper and 10s outperforming as the curve twist flattened.

- A solid round of NZDM auctions (covering NZGB May-28, May-32 & Apr-37) aided NZGBs even after Tsy cheapening weighed, with cover ratios across the 3 offerings ranging from the low 2s to the mid 4s, allowing the space to correct from cheapest levels of the session.

- The early swap spread tightening impulse faded, with the major swap rates finishing 1bp higher to 2bp lower as that curve also twist flattened, leaving swap spreads little changed to a touch wider. Note that the flattening of the 2-/10-Year swap spread moved to fresh cycle extremes, pushing below the -90bp mark. That moves it closer to its GFC inverted extreme as participants weigh up the prospect of continued RBNZ tightening into a recession.

- RBNZ dated OIS was little changed/marginally firmer, with ~65bp of tightening priced for the Bank’s Feb ’23 meeting, while the strip continues to eye a terminal OCR of 5.35-5.40%.

- The monthly BNZ-SEEK report revealed an 8.1% M/M fall in job adverts in November, with BNZ noting that “there is now clearer evidence that NZ job advertising is coming off the boil,” although they flagged that “advertisement levels are still relatively high, roughly where they were a year ago.”

- Looking ahead, Friday’s local docket is headline by manufacturing activity data for Q3 and monthly card spending readings.

EQUITIES: Hong Kong Equities Pull Higher On COVID Restriction Speculation

MNI (London) - Hong Kong equities were the notable Asia-Pac mover on Thursday as press reports alluded to the potential for the rollback of some COVID restrictions, with a press conference to be held this afternoon (local time) subsequently scheduled. That leaves the Hang Seng +3% as we work through the latter rounds of Asia-Pac dealing. Nomura turned more positive on HK equities before the aforementioned reports did the rounds.

- Elsewhere, the major regional equity indices were little changed to marginally softer, with the rally in HK equities helping take the edge off some early weakness.

- The same could be said for e-minis, with the 3 major contracts running little changed after spill over from the HK rally unwound the bulk of the early downtick that was linked to firmer USD and an uptick in U.S. Tsy yields.

GOLD: Prices Down Slightly Today, Risk-off Supportive Going Forward

Gold prices are down slightly on the NY close level at around $1783.40 after rising 0.9% on Wednesday, as the DXY is up 0.2%. Prices remain below their December 5 peak of almost $1810/oz but have been range trading since then. Bullion reached a high of $1788.10 during today’s session and a low of $1781.51.

- The risk-off environment with recession fears growing is likely to be positive for gold prices going forward. Key resistance is at $1807.90, the August 10 high.

- The fall in Australian October exports was driven by a 20.5% drop in non-monetary gold (overall exports to India were down 37.8% y/y).

- There is little of note overnight with the Fed in blackout ahead of its December 14 meeting. The US jobless claims data are the only major release.

OIL: Prices Trending Down But Today Found Support From China Reopening

MNI (Australia) - Oil prices are trading in a narrow range again today of less than a dollar. December has seen range trading at continually lower levels driven by recession fears. WTI and Brent are up around 1% on their NY close at around $72.75/bbl and $77.85 respectively, but remain close to January’s levels.

- WTI reached a high of $72.85 today and a low of $72.27. While Brent’s high was $77.99 and low $77.34. Crude’s move lower over the last few days now opens up $70 as a key support level for WTI and $77.04 for Brent.

- Oil during today’s session found some support from the improved demand outlook from China, the world’s largest oil importer, as it gradually reopens.

- While the EIA US inventory data overnight showed another crude drawdown it reported an increase in distillate and gasoline suggesting weaker demand in the US. The government is monitoring demand and supply factors before deciding whether to increase the strategic reserves.

- Currently, the cap on Russian seaborne oil that began at the start of the week doesn’t seem to have had a significant impact but there is a growing hold up of tankers around Turkey (bbg).

- There is little of note overnight with the Fed in blackout ahead of its December 14 meeting. The US jobless claims data are the only major release before the PPI and Michigan consumer sentiment on Friday.

FOREX: USD Firmer In Asia Alongside Higher Tsy Yields

The greenback benefitted from an uptick in U.S. Tsy yields as Asia-Pac participants faded yesterday’s richening in the Tsy space (and resultant weakness in the USD), with a firmer Hang Seng Index, linked to press reports pointing to a potential loosening of Hong Kong’s COVID restrictions, doing little to dent the early rally in the greenback. E-mini futures are weaker on the uptick in the USD, but off lows on the bid in the Hang Seng.

- Regional headline flow was limited, with Australian trade balance data having little impact on the AUD.

- The JPY finds itself at the bottom of the G10 FX table, with a surprise Japanese BoP current account deficit perhaps applying further pressure to the JPY, on top of the U.S. Tsy yield-derived USD bid.

- USD/CNH has coiled, with a lack of meaningful inputs observed. Participants now await the latest Chinese press briefing on COVID matters (due at 07:00 London) after the country outlined its home quarantine guidelines. The press conference is set to focus on COVID prevention & control measures.

- Central bank communique headlines on Thursday, with comments from ECB President Lagarde, as well as ECB’s de Cos & Villeroy, Riksbank’s Ingves & Floden and SNB’s Maechler all slated.

FX OPTIONS: Expiries for Dec08 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0400-20(E798mln), $1.0450(E810mln), $1.0732(E800mln)

- USD/JPY: Y137.00($761mln), Y141.15($900mln), Y142.00($909mln)

- AUD/USD: $0.6700(A$787mln), $0.6800-15(A$1.2bln)

- USD/CAD: C$1.3650($715mln)

- USD/CNY: Cny6.9700($900mln)

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 08/12/2022 | 1200/1300 |  | EU | ECB Lagarde Intro at European Systemic Risk Board Conf | |

| 08/12/2022 | 1330/0830 | ** |  | US | Jobless Claims |

| 08/12/2022 | 1330/0830 | ** |  | US | WASDE Weekly Import/Export |

| 08/12/2022 | 1500/1000 | * |  | US | Services Revenues |

| 08/12/2022 | 1530/1030 | ** |  | US | Natural Gas Stocks |

| 08/12/2022 | 1630/1130 | * |  | US | US Bill 08 Week Treasury Auction Result |

| 08/12/2022 | 1630/1130 | ** |  | US | US Bill 04 Week Treasury Auction Result |

| 08/12/2022 | 1730/1230 |  | CA | BOC Deputy Kozicki speech |