MNI EUROPEAN OPEN: China CPI Points To Benign Domestic Backdrop

EXECUTIVE SUMMARY

- US TO WIDEN SANCTIONS TO CURB CHIP SALES TO RUSSIA’S WAR MACHINE - BBG

- US WEIGHS MORE LIMITS ON CHINA’S ACCESS TO CHIPS FOR AI - BBG

- JAPAN MAY CGPI RISES 2.4% Y/Y, HIGHER IMPORT PRICES - MNI BRIEF

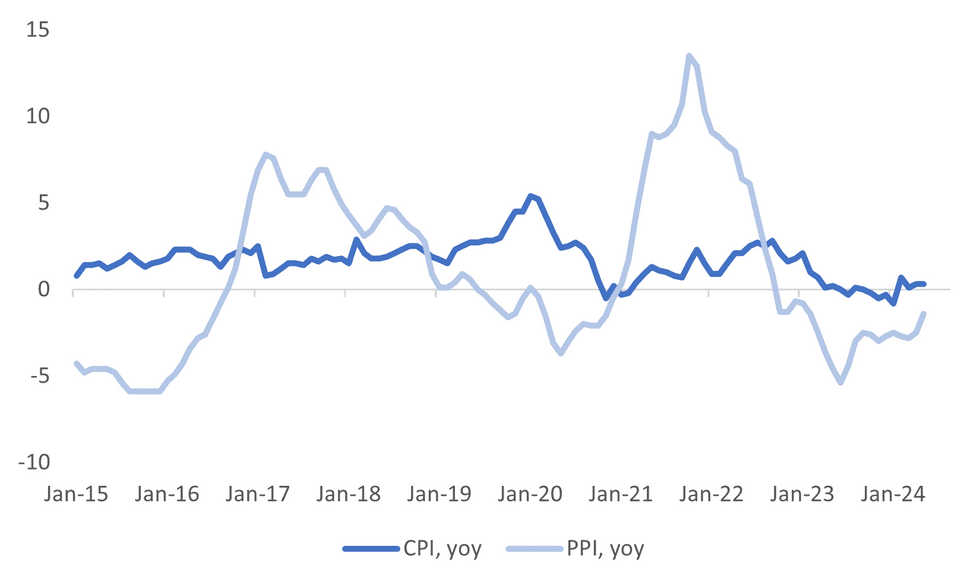

- CHINA MAY CPI FLAT AT 0.3% Y/Y - MNI BRIEF

Fig. 1: China CPI & PPI Y/Y

Source: MNI - Market News/Bloomberg

UK

POLITICS (BBG): Labour Party leader Keir Starmer and his shadow chancellor, Rachel Reeves should leave themselves wriggle room to raise UK taxation if needed, former leader Neil Kinnock suggested, as the party’s current leadership faces increasing pressure to rule out an array of tax rises.

EUROPE

EU (EU NEWS): EU leaders meeting in Brussels next week will start discussing who should get top jobs, including the Commission chief role Ursula von der Leyen has been holding for five years and would like to extend for another term.

FRANCE (BBG): Emmanuel Macron’s decision to plunge into an election campaign with his party unprepared and the French public shunning him is causing consternation among the very people he needs to win.

FRANCE (BBC): The leader of France's right-wing Republicans party, Eric Ciotti, has sparked an outcry after he backed an alliance with the far-right National Rally in snap elections announced by President Emmanuel Macron.

FRANCE (BBG): The Bank of France cut its growth forecasts for the next two years as it included higher assumptions for energy prices and a hit to activity from spending cuts to close down the budget deficit.

FRANCE (BBG): Finance Minister Bruno Le Maire warned that France would be plunged into a debt crisis if far-right leader Marine Le Pen were to win legislative elections slated for the end of the month and implement her economic program.

UKRAINE (POLITICO): Ukraine is to receive hundreds of millions of euros from European banks to buttress its economy and eventually rebuild its infrastructure, according to a series of agreements signed in Berlin on Tuesday.

UKRAINE (DW): Ukrainian President Volodymyr Zelenskyy addressed the German parliament, as Berlin hosted a conference to try to secure billions in funding to boost Kyiv's defense against Russia and rebuild Ukraine.

UKRAINE (DW): Ukraine's military said its air defense systems were repelling the air strikes on Kyiv launched by Russia overnight into Wednesday. Several blasts were heard in and around Kyiv, DW reports, with air raid alerts in place throughout Ukraine.

UKRAINE (DW): The US will provide Ukraine with another Patriot missile system, the New York Times and the Associated Press reported citing officials familiar with the matter.

UKRAINE (DW): German Defense Minister Boris Pistorius announced they will send another 100 Patriot air defense missiles to Ukraine in a joint effort with Denmark, the Netherlands and Norway.

UKRAINE (BBC): The mayor of the Ukrainian city of Kharkiv has said that the situation there has been "calmer" since Russian missile launchers shelling it were hit by Ukrainian fire.

US

GEOPOLITICS (BBG): President Joe Biden’s administration is widening sanctions on the sale of semiconductor chips and other goods to Russia, targeting third-party sellers in China and elsewhere as it looks to further choke off Vladimir Putin’s war machine in Ukraine.

US/CHINA (BBG): The Biden administration is considering further restrictions on China’s access to chip technology used for artificial intelligence, targeting new hardware that’s only now making its way into the market, people familiar with the matter said.

CORPORATE (BBG): Apple Inc. shares rallied to their first record since December on Tuesday, as investor sentiment around the iPhone maker continues to improve.

OTHER

MIDEAST (RTRS): Hamas on Wednesday said its "positive" response to a U.S. ceasefire plan for the eight-month-old war in the Gaza Strip opened a "wide pathway" to reach an agreement, but the outlook was uncertain as neither the Palestinian group nor Israel publicly committed to a deal.

JAPAN (MNI BRIEF): Japan's corporate goods price index rose 2.4% y/y in May, accelerating from April's revised 1.1%, while import price rises also accelerated and posted their fourth straight increase, up 6.9% y/y for the highest level since March 2023 following April's 6.6% gain, data released by the Bank of Japan showed on Wednesday.

AUSTRALIA (DJ): Australian consumer confidence recorded its biggest weekly fall of the year last week following data showing the economy remained largely lifeless in the first quarter, amid recent warnings from the Reserve Bank of Australia that further interest rate increases may still be required.

SOUTH KOREA (BBG): Bank of Korea Governor Rhee Chang-yong called for a balanced approach in considering the timing of a policy pivot, another sign that the central bank is moving toward easing its restrictive interest rate later this year as inflation continues to cool.

CHINA

PRICES (MNI BRIEF): China's Consumer Price Index rose by 0.3% y/y in May, flat from the previous 0.3% increase and slightly missing the market consensus of 0.4%, data from the National Bureau of Statistics showed Wednesday.

MONETARY POLICY (PEOPLE’S DAILY): People’s Bank of China Governor Pan Gongsheng vows to improve the dual-pillar regulatory framework of monetary policy and macro-prudential policy, according to a People’s Daily article on building a modern financial system with Chinese characteristics.

HOUSING (SECURITIES TIMES): China’s daily new home transaction volume increased more than 60% during the Dragon Boat Festival between June 8-10 from the recent May Day holiday, a sign that the market is recovering in the wake of a series of market-boosting policies, Securities Times reported, citing data from China Index Academy.

IPOS (SECURITIES DAILY): A total of 76 Chinese companies have received regulatory approval for overseas initial public offerings this year, exceeding the number for the whole of 2023, Securities Daily reported, citing statistics from the China Securities Regulatory Commission.

SHIPPING (21st CENTURY BUSINESS HERALD): Shipping prices are expected to remain high over the summer peak season, following the China Export Container Freight Index (CCFI) increasing 14.3% over the past month, experts interviewed by the 21st Century Business Herald have said. Industry insiders forecast freight rates to ease after three months, as shipping firms add capacity and the short-term rush for electric vehicles and energy storage equipment cools.

EMISSIONS (21st CENTURY BUSINESS HERALD): China plans to reduce the use of about 32 million tons of standard coal in the steel, oil refining, ammonia, and cement industries through equipment updates from 2024 to 2025, so as to cut carbon dioxide emissions by about 84 million tons, according to the latest documents released by the National Development and Reform Commission.

ELECTRICITY (MNI): MNI looks into China's electricity consumption and its use as a GDP indicator --On MNI Policy MainWire now.

CHINA MARKETS

MNI: PBOC conducts CNY2 bln via Omo weds; liquidity unchanged

The People's Bank of China (PBOC) conducted CNY2 billion via 7-day reverse repo on Wednesday, with the rates unchanged at 1.80%. The operation has led to no change to liquidity after offsetting the CNY2 billion maturity today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.8000% at 09:28 am local time from the close of 1.8093% on Tuesday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 50 on Tuesday, the same as the close marked on the previous trading day. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.1133 on Wednesday, compared with 7.1135 set on Tuesday. The fixing was estimated at 7.2544 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND APRIL NET MIGRATION ESTIMATE +7,380; PRIOR +5620

NEW ZEALAND ANNUAL NET IMMIGRATION SLOWS TO 98,464 – BBG

CHINA MAY CONSUMER PRICES RISE 0.3% Y/Y; EST. +0.4%; PRIOR 0.3%

CHINA MAY CORE CPI +0.6% y/y, PRIOR +0.7%

CHINA MAY PRODUCER PRICES FALL 1.4% Y/Y; EST. -1.5%; PRIOR -2.5%

JAPAN MAY PRODUCER PRICES RISE 0.7% M/M; EST. +0.5%; PRIOR +0.5%

JAPAN MAY PRODUCER PRICES RISE 2.4% Y/Y; EST. +2.0%; PRIOR +1.1%

SOUTH KOREA MAY ADJUSTED JOBLESS RATE 2.8%; EST. 2.8%; PRIOR 2.8%

SOUTH KOREA MAY HOUSEHOLD LENDING RISES TO KRW1,109.6T; PRIOR KRW1,103.6T

MARKETS

US TSYS: Tsys Futures Steady Ahead Of Key US Data Later Today

- Treasury futures are little changed today, as the markets awaits US CPI and the FOMC later tonight. TU is - 00¼ at 101-31⅛, off highs of 101-31¼, while TY is unchanged at 109-17+, off earlier highs of 109-18.

- Volumes are on the low side this morning: TU 15k, FV 30k TY 51k

- Tsys Flows: 1,500 Block likely buyer of FVU4, Large SOFR Strip buyer DV01 $1m

- Cash treasury curve is little changed this morning with the 2Y +0.4bp to 4.838%, the 10Y is -0.6bp at 4.398%, while the 2y10y is -0.998 at -44.210

- Across APAC Rates: ACGBs are 2-3bps lower, Australia's Jim Chalmers said he is cautiously confident the government can bring the economy in for a soft landing. NZGBs are unch to 2bps lower, while JGBs are 2-4bps lower.

- Looking ahead, CPI at 0830ET and FOMC policy announcement at 1400ET, Fed Chairman Powell presser at 1430ET.

JGBS: Richer Ahead Of US CPI Data & FOMC Policy Decision, BoJ Decision On Friday

JGB futures are holding richer and near session highs, +30 compared to settlement levels.

- Today's BoJ Rinban operations saw negative spreads and mostly lower offer cover ratios. At the margin, this generated some slight support for the market in the Tokyo afternoon session.

- Outside of the previously outlined PPI data, there hasn't been much in the way of domestic drivers to flag.

- Looking ahead, we anticipate that the BoJ will maintain its policy rate on June 14. Nevertheless, we expect a generally hawkish tone at the meeting, indicating the possibility of additional policy tightening in subsequent meetings, possibly as soon as July.

- The focus for the June meeting will likely be on the future pace of JGB purchases. It seems increasingly likely that the Policy Board will introduce new guidelines. (See MNI BoJ Preview here)

- Cash US tsys are little changed in today’s Asia-Pac session ahead of today’s US CPI data and the FOMC policy decision.

- Cash JGBs are richer, with yields flat to 3.2bps lower. The benchmark 10-year yield is 3.0bps lower at 0.997% versus the cycle high of 1.101%.

- Swap rates are ~1bp lower. Swap spreads are wider.

- Tomorrow, the local calendar will see Weekly International Investment Flow data and results of the Q2 BSI Large Company Survey. The MoF will also conduct a Liquidity Enhancement Auction for OTR 15.5-39-year JGBs.

AUSSIE BONDS: Early Gains Relinquished, May’s Employment Report Tomorrow

In roll-impacted trading, ACGBs (YM +0.4 & XM +1.6) are largely unchanged after relinquishing the early gains driven by yesterday’s rally in US tsys. With US tsy yields steady during today’s Asia-Pac session and no significant domestic events on the calendar, the retreat from the session's peak levels likely reflects position squaring ahead of US CPI data and the FOMC policy decision.

- Cash ACGBs are 1-2bps richer, with the AU-US 10-year yield differential at -10bps.

- Swap rates are flat to 1bp lower.

- The bills strip is little changed, with pricing flat to +1.

- RBA-dated OIS pricing is unchanged across meetings. 5bps of easing is priced by year-end.

- Tomorrow, the local calendar will see the Employment Report and CBA Household Spending data.

- May jobs data will be watched closely given the RBA’s dual mandate. While the labour market remains tight, there are signs it is gradually easing. The data has been volatile lately so it will continue to be important to look through that volatility to the underlying trends. Bloomberg consensus expects 30k new jobs with the unemployment rate easing by 0.1pp to 4.0%.

- If employment comes in close to consensus at 30k, it will be slightly higher than the 6-month average to April but a lot lower than the 3-month average of around 50k.

NZGBS: Little Changed, Narrow Ranges Ahead Of US CPI & FOMC Decision

NZGBs closed slightly cheaper, with yields flat to 1bp higher and the 2/10 curve steeper. Ranges were relatively narrow ahead of key events in the US later today: CPI is at 0830ET, with the FOMC policy announcement at 1400ET and Fed Chairman Powell’s presser at 1430ET.

- The market ascribes no chance for a rate cut at this meeting but will be seeking guidance on the timing of the first rate cut. The dot plot projections are likely to show the median FOMC member expecting just one or two rate cuts this year (down from three previously projected).

- The NZGB 10-year has underperformed its $-bloc counterparts over the past 24 hours, with the NZ-US and NZ-AU 10-year differentials 5bps and 1bps wider respectively. Nevertheless, both differentials remain close to the narrowest levels seen over the past year.

- Swap rates closed 1bp lower.

- RBNZ dated OIS pricing closed 2bps softer for meetings beyond October. A cumulative 25bps of easing is priced by year-end.

- The local calendar will see Card Spending data tomorrow alongside the NZ Treasury’s planned sale of NZ$250mn of the 3% Apr-29 bond, NZ$200mn of the 2% May-32 bond and NZ$50mn of the 2.75% Apr-37 bond.

FOREX: Dollar Steady, US CPI & FOMC Coming Up

Outside of a modest pop higher in AUD, G10 FX trends have been very quiet ahead of key US event risk later, with CPI due, followed by the FOMC later on.

- The BBDXY sits around 1266.45, little changed for the session, but close to recent highs. US equity futures are up a touch, while US yields are firmer, but gains are less than 1bps.

- Regional equity markets are mixed, Hong Kong and China markets are mostly lower.

- USD/JPY is around 157.15/20 little changed for the session. We had stronger than expected PPI data earlier, but this didn't impact sentiment.

- AUD/USD has recovered from earlier lows, last near 0.6615, which is around option expiry strikes for NY cut later today. So that may be playing a role, while slightly lower USD/CNH levels are another potential positive. China May inflation data was close to expectations, but isn't suggesting a sharp pick up in domestic demand.

- NZD/USD is relatively steady, last around the 0.6145 level.

- Later the Fed is expected to hold rates steady but increase its 2024 and 2025 median rate forecast. US May headline CPI is projected to be steady at 3.4% while core should ease 0.1pp to 3.5%. The ECB’s Tuominen, Schnabel, Buch, de Guindos and McCaul, and BoC’s Macklem speak.

ASIA STOCKS: China & Hong Kong Equities Mixed On Disappointing China CPI Data

Hong Kong and China equity are mostly lower today. The Hang Seng index slipped below the crucial 18,000 level due to disappointing China CPI data and speculation about new US chip restrictions. Despite these losses, mainland Chinese investors continued their buying streak of Hong Kong stocks for the 18th consecutive session, with net purchases reaching HK$321.3 billion this year. Additionally, Chinese regulators are considering stricter rules on how banks sell financial products, which could impact distribution channels for major hedge funds.

- Hong Kong equities are lower today, HSTech Index is down 1.51%, while the Mainland Property Index is down 2.72% and the HS Property Index is down 2.10%, the HSI is down 1.45%

- China onshore equities are mixed today. The CSI300 Real Estate Index is one of the worst performing indices, down 1.24%, small-cap indices are higher with the CSI1000 is up 0.37%, the CSI2000 down 1.32%, while the CSI300 is down 0.17%.

- In the property space, China’s daily new home transaction volume increased by more than 60% during the Dragon Boat Festival (June 8-10) compared to the recent May Day holiday, indicating a market recovery following market-boosting policies, according to Securities Times. However, on a year-on-year basis, the daily transaction volume in 30 major cities declined by 16% during the Dragon Boat Festival.

- PBoC Governor Pan Gongsheng pledged to enhance the dual-pillar regulatory framework of monetary and macro-prudential policy, according to an article in People’s Daily. The PBOC aims to deepen market-oriented reforms of interest rates and exchange rates. Additionally, China Securities Regulatory Commission chief Wu Qing stated that the CSRC will expedite the development of a comprehensive capital market supervision system.

- Earlier, China's PPI for May was -1.4% y/y vs -1.5% est, while May CPI was 0.3% vs 0.4% est.

- (MNI) China Press Digest June 12: PBOC, Shipping Price, Emission (See link)

ASIA PAC STOCKS: Asian Equities Mixed, Ranges Tight Ahead Of US CPI & FOMC Later

Asian equities had a mixed performance this morning. Shares of Apple suppliers in South Korea and Japan advanced after Apple's record high on AI hopes, while Japanese stocks overall fell due to a weaker yen and cautious sentiment ahead of key US inflation data and a Federal Reserve rate decision. Conversely, Australian stocks fell, led by the mining sector, ahead of upcoming jobs data. The MSCI Asia Pacific declined as much as 0.40%.

- Japanese stocks dare lower today, with the downturn following a slip in the US Dow overnight, despite gains in the tech-rich Nasdaq and S&P 500 driven by a surge in Apple shares. Major companies like Toyota Motor, Daiichi Sankyo, and Sony Group contributed to the losses, reflecting investor caution ahead of a busy night for US data with the FOMC and the release of US inflation data. The market's apprehension is further compounded by concerns over the Bank of Japan's potential monetary policy actions to address the weak yen. The Nikkei 225 is 0.63% lower, while the Topix is 0.70% lower.

- South Korean stocks are slightly higher today, with shares of Apple suppliers advancing after Apple's record high on new AI features. The Kospi index saw gains as investors responded to the strong performance of Wall Street's tech sector. Morgan Stanley analysts recommended buying shares in the iPhone supply chain, suggesting that companies like Hon Hai, Largan, Luxshare, Genius, AAC, and Foxconn Industrial Internet could benefit from weak traction in Huawei’s newly launched Pura smartphone. The Kospi is 0.44% higher, while the small-cap Kosdaq is up 0.15%

- Taiwan equities are higher today, led higher by tech names. Foreign investors have been selling local stocks recently, with a large $1b outflow on Tuesday, although domestic investors have been able to easily absorb the supply with the Taiex trading near record highs. Focus will now turn to the central bank rate decision tomorrow. The Taiex is up 1% today.

- Australian stocks are lower today, the decline was primarily driven by weakness in the mining sector, reflecting broader concerns ahead of significant economic data releases. Investors are focused on the Federal Reserve's interest rate decision and US inflation data due tonight, while attention will shift to Australian jobs data on Thursday. The downturn in Australian equities mirrors a mixed performance across the Asia-Pacific region, with broader market volatility anticipated due to these pivotal economic developments. The ASX200 is down 0.60%

- Elsewhere in SEA, New Zealand Equities are unchanged, Singapore equities are 0.16% higher, Malaysian equities are 0.15% higher, Indian equities are 0.50% higher, while Indonesian equities are lower at the currency hits 4 year lows and Morgan Stanley downgrades local stocks to underweight.

OIL: Crude Stronger Ahead Of Fed & US CPI

Oil prices continued rising during APAC trading today ahead of the Fed decision and US CPI data later today. Brent is up 0.4% to $82.27/bbl and has spent most of the session trading above $82. It is close to the intraday high of $82.29. WTI has moved above $78 and is currently around 0.6% higher at $78.35/bbl after a peak of $78.39. The USD index is slightly stronger.

- Bloomberg reported a US crude stock drawdown of 2.4mn barrels last week, according to people familiar with the API data. Gasoline fell 2.5mn but distillate rose 1mn. The official EIA data is out later today.

- Reports on Tuesday showed that OPEC still expects a pickup in crude demand in H2 and a supply shortfall while the US’ EIA revised up its US output projections to a new record high. The global IEA will release its monthly report later today.

- ING expects a large market deficit in Q3 which should support oil prices.

- Later the Fed is expected to hold rates steady but increase its 2024 and 2025 median rate forecast (see MNI Fed Preview). US May headline CPI is projected to be steady at 3.4% while core should ease 0.1pp to 3.5% (see MNI US Preview).

- The ECB’s Tuominen, Schnabel, Buch, de Guindos and McCaul, and BoC’s Macklem speak. UK April trade and monthly GDP print.

GOLD: Steady Ahead Of US CPI & FOMC Decision

Gold is little changed in the Asia-Pac session, after closing 0.3% higher at $2317.01 on Tuesday.

- Bullion was supported by lower US Treasury yields, which in turn were buoyed by haven demand associated with European Parliament elections and the surprise snap election called in France. Solid demand metrics at a 10Y auction added to US Treasuries’ strength.

- The 10-year yield finished 7bps lower at 4.40%, with 2-year was down 5bps to 4.83%.

- Later today, the US calendar delivers US CPI at 0830ET today, with the FOMC policy announcement at 1400ET and Fed Chairman Powell’s presser at 1430ET.

- The market ascribes no chance for a rate cut at this meeting but will be seeking guidance on the timing of the first rate cut. The dot plot projections are likely to show the median FOMC member expecting just one or two rate cuts this year (down from three previously projected).

- According to MNI’s technicals team, the yellow metal cleared support around the 50-day EMA, at $2,315.2, in last week’s sharp sell-off, opening $2,277.4, the May 3 low. Initial resistance to watch is $2,387.8, Friday’s high.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 12/06/2024 | 0600/0700 | ** |  | UK | UK Monthly GDP |

| 12/06/2024 | 0600/0700 | ** |  | UK | Trade Balance |

| 12/06/2024 | 0600/0700 | ** |  | UK | Index of Services |

| 12/06/2024 | 0600/0700 | *** |  | UK | Index of Production |

| 12/06/2024 | 0600/0700 | ** |  | UK | Output in the Construction Industry |

| 12/06/2024 | 0600/0800 | *** |  | DE | HICP (f) |

| 12/06/2024 | 0900/1000 | * |  | UK | Index Linked Gilt Outright Auction Result |

| 12/06/2024 | 0930/1130 |  | EU | ECB's Schnabel at German Finance Committee | |

| 12/06/2024 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 12/06/2024 | - | *** |  | CN | Money Supply |

| 12/06/2024 | - | *** |  | CN | New Loans |

| 12/06/2024 | - | *** |  | CN | Social Financing |

| 12/06/2024 | - |  | UK | Sky News- Election Leaders Event | |

| 12/06/2024 | 1230/0830 | *** |  | US | CPI |

| 12/06/2024 | 1230/0830 | * |  | CA | Intl Investment Position |

| 12/06/2024 | 1300/1500 |  | EU | ECB's De Guindos at MNI Connect Event | |

| 12/06/2024 | 1430/1030 | ** |  | US | DOE Weekly Crude Oil Stocks |

| 12/06/2024 | 1600/1200 | *** |  | US | USDA Crop Estimates - WASDE |

| 12/06/2024 | 1800/1400 | ** |  | US | Treasury Budget |

| 12/06/2024 | 1800/1400 | *** |  | US | FOMC Statement |

| 12/06/2024 | 1915/1515 |  | CA | BOC Governor Macklem speaks at panel in Montreal. |