MNI EUROPEAN MARKETS ANALYSIS: Yen Whipsawed On BoJ Rhetoric, US CPI Coming Up Later

- G10 FX and rates have been mostly subdued ahead of the upcoming US CPI print. The exception has been USD/JPY. The pair dipped in early trade but has more than recouped those losses following more balanced comments from BoJ Governor Ueda around the current economic backdrop.

- Equity sentiment has been buoyant in Hong Kong today, led by property and tech names. The tone for mainland shares has been much more mixed though. There hasn't much positive spill over elsewhere, although higher US equities have been evident.

- Looking ahead, Labour market data in the UK kicks off the Tuesday docket before all attention turns to US CPI. Consensus puts core CPI inflation at 0.3% M/M in February with little skew either side. OER inflation will be watched particularly closely, with a surprisingly narrow range across analysts considering the surprise divergence with primary rents data in last month’s report.

MARKETS

US TSYS: Treasury Futures Trade Steady And In Tight Ranges Ahead of US CPI

- Treasury futures have traded in very tight ranges today with Jun'24 10Y making lows of 111-18 and highs of 111-21, to currently trade + 01 for the day at 111-20, while 5Y futures are +00¼ to 107-20¼

- Looking at technicals, 10Y futures initial supports holds at 111-02 (20-day EMA), below there 110-21 (Mar 4 low), to the upside, initial resistance is 112-04+ (Mar 8 highs) while above is 112-04+ (61.8% retracement of the Feb 1 - 23 bear leg)

- Treasury curves are mostly unchanged on Tuesday, the 2y yield is -0.4bp to 4.532%, the 10y yield is -0.6bps at 4.092%, while the 2y10y is -0.143 to -44.347

- Earlier, JPMorgan CEO Jamie Dimon spoke acknowledging a robust US economy bordering on a boom but remains cautious, citing a possible equity market bubble and not ruling out a recession. He emphasizes the need for the Federal Reserve to be data-dependent, suggesting a delay in rate cuts beyond June. Dimon notes AI's crucial role in management discussions and suggests most US banks could navigate challenges if rates remain stable, but he doesn't dismiss the possibility of a recession, even at 6% rates.

- Looking ahead: US CPI

JGBS: Futures Holding A Down Tick, Off Worst Levels After A Strong 5Y Auction

JGB futures are holding in negative territory, -4 compared to the settlement levels, but have pared early losses.

- (Bloomberg) -- Bank of Japan Governor Kazuo Ueda reaffirmed that the economy continues to recover gradually, sending a signal that the central bank is still on track to end its negative interest rate in the near future. (See link)

- There hasn’t been much in the way of domestic data drivers to flag, outside of the previously outlined PPI data.

- Cash US tsys are dealing little changed in today’s Asia-Pac session ahead of US CPI data later today. There will be heightened sensitivity to any deviation from the consensus which sits at 0.3% m/m and 3.7% y/y for CPI ex food and energy. MNI US CPI Preview here (ICYMI)

- Cash JGBs are dealing slightly mixed, with the 10-year (+1.6bps) and 40-year (+1.8bps) zones underperforming. The benchmark 10-year yield earlier hit 0.779%, a fresh high for the year.

- The 5-year yield is 0.7bp lower at 0.377% after today’s supply saw strong demand metrics. The auction's low price beat dealer expectations, the cover ratio increased to 3.991x from 3.435x at February’s auction and the tail shortened. Today’s cover was the highest since November.

- The swaps curve is slightly richer, with rates ~1bp lower. Swap spreads are tighter.

- Tomorrow, the local calendar is empty.

AUSSIE BONDS: Little Changed, Subdued Session Ahead Of US CPI Data

In roll-impacted dealings, ACGBs (YM -0.6 & XM -0.4) are slightly cheaper, after dealing in narrow ranges in today’s Sydney session.

- (Brisbane Times) Former Reserve Bank governor Philip Lowe has joined the chorus of voices warning that stubborn inflation could lead to interest rates staying higher for longer than many expect. (See link)

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined NAB Business Survey for February.

- Cash US tsys are dealing little changed in today’s Asia-Pac session ahead of US CPI data later today. There will be heightened sensitivity to any deviation from the consensus which sits at 0.3% m/m and 3.7% y/y for CPI ex food and energy.

- Cash ACGBs are flat to 1bp cheaper, with the AU-US 10-year yield differential 4bps lower at -14bps.

- Swap rates are little changed.

- Bills are flat to +2.

- RBA-dated OIS pricing is little changed. A cumulative 48bps of easing is priced by year-end.

- Tomorrow, the local calendar sees the release of the CBA Household Spending data, which represents the final data update before the forthcoming RBA Policy Decision scheduled for next Tuesday.

NZGBS: Closed Little Changed Ahead Of US CPI Data Later Today

NZGBs closed little changed after dealing in narrow ranges during today’s session. NZGBs did however underperform their $-bloc counterparts, with the NZ-US and NZ-AU 10-year yield differentials 3bps and 2bps wider respectively.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined Card Spending data. The Light Traffic Index rose 1.9% m/m in February, while the Heavy Traffic Gauge gained 2.4% m/m, according to ANZ Bank.

- Local investors appeared content to sit on the sidelines ahead of US CPI data later today. There will be heightened sensitivity to any deviation from the consensus which sits at 0.3% m/m and 3.7% y/y for CPI ex food and energy.

- Cash US tsys are dealing little changed in today’s Asia-Pac session.

- Swaps are little changed.

- RBNZ dated OIS pricing is flat to 2bps softer across meetings, with November leading. A cumulative 65bps of easing is priced by year-end.

- Tomorrow, the local calendar sees Food Prices, ahead of REINZ House Sales and Net Migration data on Thursday.

- On Thursday, the NZ Treasury plans to sell NZ$275mn of the 0.25% May-28 bond and NZ$225mn of the 2% May-32 bond.

FOREX: USD Index Recoups Earlier Losses, As Ueda Comments Weigh On Yen

The USD index (BBDXY) sits unchanged versus end NY levels on Monday, last near 1229.20. We are up from earlier lows (1228.46), after the yen pared its earlier gains, after more balanced comments from BoJ Governor Ueda.

- Overall ranges in the USD index have been fairly tight, with limited volatility outside of USD/JPY moves. In the cross asset space, US equity futures are higher at this stage, led by tech (Nasdaq futures +0.55%). US yields are closed to unchanged.

- USD/JPY dipped in earlier trade, falling to 146.62, which was still above both Friday and Monday intra-session lows just under 146.50. This dip followed news wire headlines from Jiji stating the BoJ would end NIRP if the first round of wage negotiations delivered a 'significantly' bigger rise than last year (3.8%). Friday should see these results known.

- BoJ Governor Ueda though tempered hawkish sentiment at the margins. Appearing before parliament he stated consumption of non-durables was weak, but the economy was gradually recovering. He added the central bank will mull changes if the inflation goal is in sight. USD/JPY sits back near 147.40 in latest dealings, just below session highs (147.44).

- AUD and NZD sit close to unchanged for the session so far. AUD/USD last near 0.6610/15. Earlier comments from RBA Assistant Governor Hunter noted households are under pressure but she didn't touch on the monetary policy outlook. The Feb NAB business survey was mixed, with confidence back to flat, while conditions improved to 10 from 7 in Jan.

- NZD/USD was last at 0.6170. Earlier data showed weak card spending trends for Feb, in line with a softer consumer spending backdrop.

- Looking ahead, Labour market data in the UK kicks off the Tuesday docket before all attention turns to US CPI. Consensus puts core CPI inflation at 0.3% M/M in February with little skew either side. OER inflation will be watched particularly closely, with a surprisingly narrow range across analysts considering the surprise divergence with primary rents data in last month’s report.

ASIA EQUITIES: Hong Kong Equities Surge Higher, China Equities Underperform

- Hong Kong equity markets are higher today, the Hang Seng Biotech Index has erased all of last weeks losses trading up another 2.77% today, the Mainland Property Index has shrugged off China Vanke's downgrade to trade up 4.20%%, while the HSTech index is up 3.00% and the wider HSI is up 1.70%

- In China, equity markets only slightly higher for the day with concern around whether there will be enough government support to help the troubled property market, investors are concerned after two of China's largest banks have refused to sign off on a syndicated loan to Vanke. The CSI1000 up 0.15%, ChiNext 0.22%, and the large cap CSI300 now 0.03% lower.

- China Northbound flows were 10.3 billion yuan on Thursday, with the 5-day average at 2.84 billion, while the 20-day average sits at 2.87 billion yuan.

- In the property space, China Vanke was downgraded to junk by Moody's. Bloomberg reported that ICBC and China Construction Bank have yet to sign off on a syndicated loan after asking Vanke to provide sufficient collateral to back the new loan, but the developer was unwilling to do so. It should be noted that China Vanke has repaid nearly half of its maturing offshore debts this year and plans to repay the two remaining offshore debts due in May and June with its funds and offshore syndicated loans.

- US Commerce Secretary Gina Raimondo has indicated that the United States may tighten controls on China's access to advanced semiconductor technologies to prevent Beijing from advancing in military capabilities, emphasizing the need to protect sophisticated technology and suggesting a willingness to expand controls as necessary. The Biden administration is reportedly considering new sanctions on Chinese tech companies and urging allies to curb the export of advanced technology to China.

ASIA PAC EQUITIES: Equities Mixed Today, Japan Lower Amid Speculation BoJ To Move

Regional Asian equities are mixed, with Japanese equities underperforming amid speculation about the Bank of Japan (BoJ) ending its negative interest rate policy. The Bloomberg Asia-Pacific Developed Markets (APAC DM) Index is down close to 1%, while iron ore prices are weighing on the mining sector.

- Japanese equities have fallen for the second day amid speculation that the BoJ will end its negative interest rate policy as early as next week. Banks are the worst performers, with the Topix Bank Index down 2.25% today and 6.26% over the past two days, while the Topix is down 0.95%, and the Nikkei 225 is trading slightly better, down just 0.35%.

- South Korean equities are higher today, with the small-cap index Kosdaq up 1.00%, led higher by gains in EV battery suppliers, while the Kospi is up 0.40%.

- Taiwan equities are higher today, with tech names outperforming. Taiwan equities saw their largest foreign investor inflow on Friday in about a month, with net flows of 1,470 billion entering the market. The Taiex is up 0.90%.

- Australian equities are slightly higher today, with banks and miners as the worst performers, offsetting gains in healthcare and tech; the ASX200 is up 0.06%.

- Elsewhere in Southeast Asia, New Zealand equities are down 0.56%, the worst performer, while Thailand, India, Singapore, and Malaysia are unchanged to 0.20% higher.

ASIA EQUITY FLOWS: Asian Equity Flows Turn Negative As Tech Falls, China The Exception

- China equities closed Monday higher helped by higher than expected CPI data, while China Vanke depositing money to repay a bond due this week helped push the property sector higher. The 5-day average is now 2.84b, inline with the 20-day average at 2.87b

- South Korean equities stocks were lower after semiconductor names fell on worries about Nvidia's lofty valuations, the stock is down close to 10% over the past two days. SK saw net flows of -141m on Monday, taking the 5-day average to -90m, while the 20-day average sits in positive territory at $165m

- Taiwan equities fell on Monday, largely due to global semiconductor equity prices falling, while Taiwan also saw equity outflows. The Philadelphia semiconductor Index fell 1.36^ overnight, so it would be expected outflows to continue today. Taiwan Equities 5-day average at $431m still sits above the 20-day average at $348m

- Thailand equities were lower on Monday and again saw foreign equity outflows now at 9 of the past 11 days. It is important to note that the SET has bounced off the yearly lows marking the third fail attempt to break below 1350. The 5-day average is now -$24m while the 20-days is at -$8m

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| China (Yuan bn)* | 10.3 | 14.2 | 48.1 |

| South Korea (USDmn) | -142 | -451 | 8665 |

| Taiwan (USDmn) | -125 | 2159 | 8382 |

| India (USDmn)*** | 1279 | 2199 | -459 |

| Indonesia (USDmn)** | 80 | 43 | 1199 |

| Thailand (USDmn) | -66 | -122 | -950 |

| Malaysia (USDmn) ** | -17 | -320 | 60 |

| Philippines (USDmn) | -5 | 11.6 | 246 |

| Total (Ex China USDmn) | 1004 | 3519 | 17144 |

| * Northbound Stock Connect Flows | |||

| ** Data Up To March 8 | |||

| *** Data Up To March 7 |

OIL: Up Modestly, Awaiting US CPI & OPEC+ Report Later.

Brent (K4) has risen modestly in the first part of Tuesday trade. The benchmark was last at $82.50/bbl, up 0.35%, building on a small gain from Monday's session. WTI (J4) is up by a similar magnitude, last near $78.15/bbl. Both markets appear to be largely treading water ahead of key event risks later.

- Brent sits comfortably above Monday's lows near $81/bbl. Equally we are still some distance away from early March highs of $84.34/bbl.

- Earlier headlines crossed from Houthis stating they had attacked a US vessel in the Red Sea. The US stated that no damage has been reported and that the missiles did not strike the vessel. This follows joint US/UK strikes against Houthi controlled areas in Yemen (BBG).

- Like markets elsewhere, oil traders are awaiting the print of the US CPI later. Also out will be the OPEC+ monthly report, along with industry figures on US crude stockpiles.

- OPEC+ crude oil production rose to 34.62mbpd in February, up from 34.54mbpd in January and 0.30mbpd above the pledged output target according to Argus estimates.

GOLD: Consolidates After Its Record-Breaking Run

Gold is 0.2% weaker in the Asia-Pac session, after closing 0.2% higher at $2182.75 on Monday.

- Monday’s gain expanded bullion winning streak to nine consecutive sessions and came despite US Treasury yields pushing higher with a flattening bias. US yields finished the NY session 1-6bps higher.

- There were no headline or data-driven factors but $26bn of corporate and $56bn of 3-year Treasury issuance weighed.

- The market’s focus now shifts to CPI data later today, and PPI and Retail Sales on Thursday. There will be heightened sensitivity to any deviation from the consensus which sits at 0.3% m/m and 3.7% y/y for CPI ex food and energy.

- According to MNI’s technicals team, the yellow metal last week traded above resistance at $2135.4, the Dec 4 high, signalling scope for a climb towards $2206.6 next, a Fibonacci projection. Short-term conditions are overbought; however this does not appear to be a concern for bulls - for now.

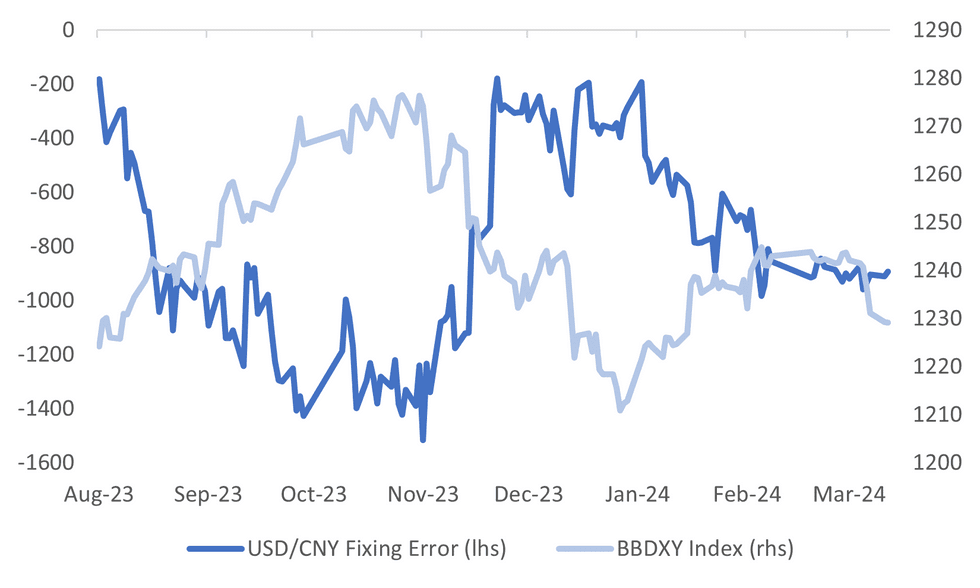

CNH: USD/CNY Fixing Error Stays Wide Despite Recent USD Weakness

USD/CNH sits near 7.1800 in recent dealings, slightly up from session lows. Earlier we got to 7.1763, fresh lows back to end Jan of this year.

- CNH was largely following earlier yen gains, albeit with a lower beta. The surging yen backdrop has likely aided CNH in recent sessions, as historical correlations between the pair remain reasonable in the past 3-6 months (around 55-60%).

- It's also noteworthy the USD/CNY fixing error (the difference between the actual fixing and the consensus Bloomberg estimate) has stayed wide, even in the face of recent USD weakness.

- The chart below plots the fixing error against the BBDXY index. In the past 6 months or so, the fixing error has tended to tighten (or trend closer to 0pips) when the USD has weakened and vice versa when the USD has rallied.

- It may be the case the fixing error tightens in coming sessions if the USD trend stays weak. If not, the intent of the authorities may be to further support the yuan via the fixing mechanism and guard against any renewed moves above 7.2000 (particularly for onshore spot).

Fig 1: USD/CNY Fixing Error Versus BBDXY Index

Source: MNI - Market News/Bloomberg

ASIA FX: CNH Steady, Upticks In USD/KRW & USD/PHP Sold

USD/Asia pairs are mixed in the first part of Tuesday trade. USD/CNH couldn't extend sub 7.1800, while the 1 month USD/KRW NDF got close to Monday lows near 1305, but we there was no follow through. USD/THB has rebounded though, while steadier trends are evident elsewhere. No doubt there is some degree of cautiousness ahead of the upcoming US CPI print later. Later on, India CPI and IP prints as well. In EM Asia markets tomorrow, we have South Korean unemployment and bank lending to households. Indonesia consumer confidence is also out.

- USD/CNH tested lower earlier, amid a round of USD/JPY weakness. The pair got to 7.1763, fresh lows, but we since back above 7.1800 now. Yen gains have been pared, while onshore equities have been mixed and haven't seen much positive spill over from the surge in Hong Kong bourses. the USD/CNY fixing error stayed wide, despite the recent correction lower in the USD.

- 1 month USD/KRW has generally been sold on upticks so far today, although we haven't made fresh lows sub 1305 at this stage. The pair was last near 1307, still slightly firmer in won terms versus end NY levels on Monday. Higher USD/JPY levels also hasn't weighed on the yen. Equity sentiment has helped, with the rise in US equity futures a positive (led by the tech side). Onshore equities are firmer as well, up 0.5%, although offshore investor flows have been negative so far today (-$178.7mn).

- USD/THB sits back at 35.53, around 0.4% weaker in baht terms for the session so far. Like elsewhere in the region, we are seeing some modest signs of USD consolidation post the recent sharp sell-off. For USD/THB today's rebound, if sustained, would end an as strong run of downside momentum seen since over the past week. Outside of broader USD shifts, focus will remain the domestic economy and the respective BOT and tourism outlooks. We haven't got much on the data calendar though until the latter stages of March when trade figures are due.

- USD/PHP has had a somewhat volatile session so far, although the market bias is to fade upside USD moves. Earlier highs at 55.50 were sold and we sit near fresh lows back to late last year, last near 55.32. On the data front, Jan trade figures. The trade deficit printed at -$4.22bn, slightly better than expected (-$4.7bn was the forecast). It was still wider than the prior month's outcome, with the deficit largely trending sideways in recent months.

PHILIPPINES: Philippines Sov Curve Flatter, Trade Balance Beats Estimates

The Philippines USD sovereign debt curve has flattened today with yields 0-2bps higher, underperforming the move by US treasuries. Eyes will be on US CPI data due out later today.

- The 2Y yield is unchanged at 4.78%, 5Y yield is 0.5bps higher at 4.855% the 10Y yield is 1bp higher at 4.95%, while 5yr CDS is down 0.25bps to 60.50bps

- The Philip to US Treasury spread difference widen late last week, but have been able to close the gap slightly to start this week with he spread difference for the 2y is 23bps, the 5yr is 32bps, while the 10yr is 85bps.

- Cross-asset moves: the USD/PHP is down 0.02%, PSEi Index is 0.53% higher, Corporate Credit curve is 2-6bps tighter over the week with better buying at the 4-5yr maturity, while US Tsys are 0-1bps lower

- On the data front, Jan trade figures. The trade deficit printed at -$4.22bn, slightly better than expected (-$4.7bn was the forecast). It was still wider than the prior month's outcome, with the deficit largely trending sideways in recent months. Exports surprised modestly on the topside, +9.1% y/y (+7.4% forecast), with electronic exports up over 16%y/y.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 12/03/2024 | 0700/0800 | *** |  | DE | HICP (f) |

| 12/03/2024 | 0700/0700 | *** |  | UK | Labour Market Survey |

| 12/03/2024 | 0800/0900 |  | EU | ECB's De Guindos participates in ECONFIN meeting | |

| 12/03/2024 | 1000/0600 | ** |  | US | NFIB Small Business Optimism Index |

| 12/03/2024 | 1000/1000 | ** |  | UK | Gilt Outright Auction Result |

| 12/03/2024 | 1100/1100 |  | UK | BOE's Mann on NIESR Panel | |

| 12/03/2024 | - | *** |  | CN | Money Supply |

| 12/03/2024 | - | *** |  | CN | New Loans |

| 12/03/2024 | - | *** |  | CN | Social Financing |

| 12/03/2024 | 1230/0830 | *** |  | US | CPI |

| 12/03/2024 | 1230/0830 | * |  | CA | Intl Investment Position |

| 12/03/2024 | 1255/0855 | ** |  | US | Redbook Retail Sales Index |

| 12/03/2024 | 1445/1545 |  | EU | ECB's Elderson at 'banking sector and climate...' workshop | |

| 12/03/2024 | 1530/1130 | * |  | US | US Treasury Auction Result for Cash Management Bill |

| 12/03/2024 | 1700/1300 | ** |  | US | US Note 10 Year Treasury Auction Result |

| 12/03/2024 | 1800/1400 | ** |  | US | Treasury Budget |