MNI EUROPEAN MARKETS ANALYSIS: Yen Lags Risk Off Signals

- Metals weakness remains in focus from a broader cross-asset standpoint. Gold and silver seeing further sharp losses today.

- Equity sentiment has been weaker, with key bourses and US futures weaker. In the FX space, sentiment has been volatile. Yen has lagged the risk off signals, while AUD is the weakest performer.

- Safe haven demand has emerged for bonds as the session progressed.

MARKETS

US TSYS: Weak Global Sentiment Builds Case for Lower Yields

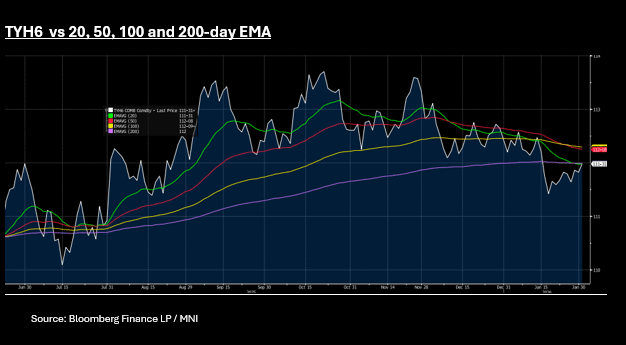

US treasury futures trended lower during the morning, but as the afternoon progressed and equities got heavier turned positive. The move lower could be reflective of portfolio re-balancing on account of the huge falls in commodities, but the trend was clear in the afternoon as all major futures turned up. The 10-Yr is up +04+ at 111-31+ and is near to the 20-day EMA of 111-31 and the 200-day EMA of 112. A sustained break above could bring the 50-day EMA into play at 112-08.

Market sentiment continues to be weak with US equity futures pointing to a weak start tonight and could feed into further gains for bonds.

Cash is strong with yields down by -.07bps to -2.0bps with the front end outperforming.

- The 2-Yr is down -2bps 3.506%

- The 5-Yr is down -1.9bps at 3.771%

- The 10-Yr is down -1.6bps at 4.224%

- The 30-Yr is down -0.7bps at 4.867%

The risks are that Warsh's previous comments about rates are the playbook, despite what the White House wants. The uncertainty around a balance sheet unwind will create volatility but for now as risk sentiment weakens, the bias for lower yields seems building.

JGBS: Reverse Stronger Amidst Risk-Off Sentiment, 10Y Supply Tomorrow

JGB futures are stronger after reversing early weakness, +6 compared to settlement levels.

- MNI: BOJ Opinions: Early Rate Hikes, Upside Risks to Prices. Several Bank of Japan board members saw the need to raise the policy interest rate relatively early, with one favouring hikes at intervals of a few months, according to the summary of opinions

- Bloomberg - "Japan's ruling bloc is poised to win 300 out of 465 seats in the upcoming election, an Asahi poll showed."

- Cash US tsys are flat to 2bps cheaper, with a steepening bias, in today's Asia-Pac session. US ISM Manufacturing PMI data will take focus on Monday, while markets will be attentive to developments over the US government shutdown and any potential comments from both Fed's Powell and Warsh ahead. The employment report for January on Friday.

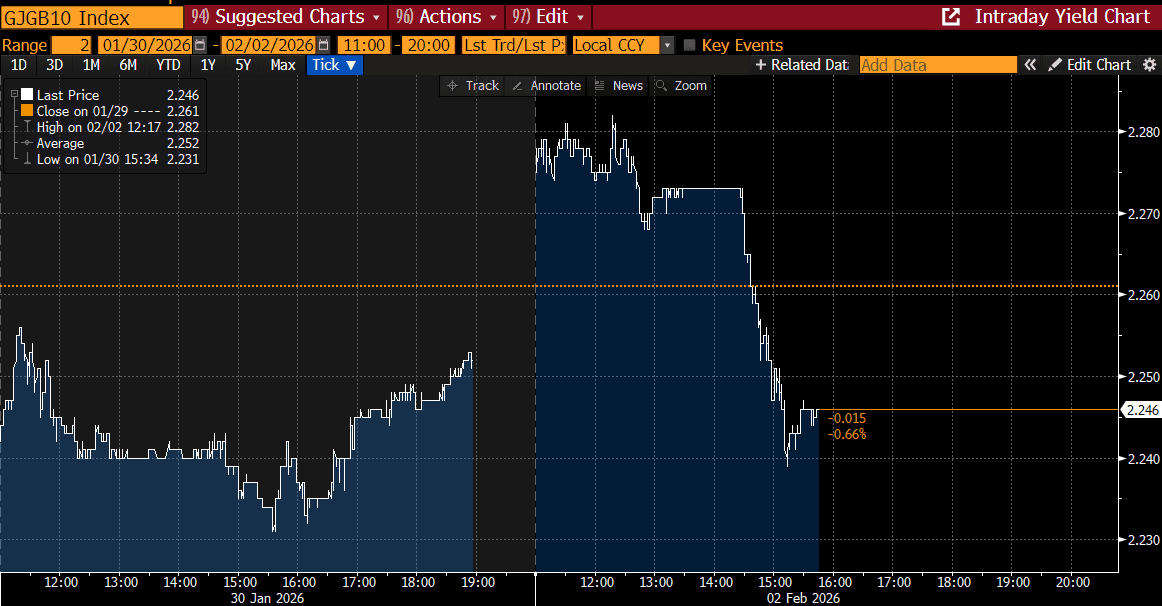

- Cash JGBs have reversed early weakness across benchmarks, with the 10-year yield now 0.7bp lower at 2.245% after the morning’s high of 2.282% amidst risk off sentiment.

- Swap rates are flat to slightly higher, with a flattening bias.

- Tomorrow, the local calendar will see Monetary Base data alongside 10-year supply.

Source: Bloomberg Finance LP

AUSSIE BONDS: Subdued Trading Ahead Of Tomorrow's RBA Policy Decision

ACGBs (YM +1.5 & XM -0.5) are slightly mixed after a relatively subdued start to the trading week.

- Cash US tsys are flat to 2bps richer, with a steepening bias, in today's Asia-Pac session.

- Cash ACGBs are slightly richer with the AU-US 10-year yield differential at +58bps, a few bps below its recent high.

- The bills strip has bull-steepened across contracts, with pricing flat to +2.

- RBA-dated OIS pricing has firmed by around 11–20bps across meetings since the release of December’s stronger-than-expected labour market data on 22 January.

- Last week’s firmer-than-expected Q4 trimmed mean CPI print reinforced the repricing ahead of tomorrow’s RBA policy decision.

- The combination of a resilient labour market and stronger than expected Dec/Q4 inflation has the sell-side consensus expecting an RBA rate hike tomorrow. If delivered, focus will be on how much follow up action the central bank sees as needed to ensure inflation returns to target (see MNI RBA Preview here)

- A 25bp hike tomorrow is priced at a 76% probability, with cumulative tightening probability of 161% by June and 223% by December 2026.

- This week, the AOFM plans to sell A$1200mn of the 4.25% 21 October 2036 bond on Wednesday and A$800mn of the 1.00% 21 December 2030 bond on Friday.

Bloomberg Finance LP

RBA: MNI RBA Preview-Feb 2026: +25bps Likely, Focus On Outlook

EXECUTIVE SUMMARY:

- The combination of a resilient labour market and stronger than expected Dec/Q4 inflation has the sell-side consensus expecting an RBA rate hike tomorrow. If delivered, focus will be on how much follow up action the central bank sees as needed to ensure inflation returns to target. The trimmed mean CPI y/y has been trending up since mid last year and is now comfortably above the top end of the RBA's 2-3% target band. We expect the RBA to leave the door ajar for another hike, albeit one that remains dependent on data outcomes.

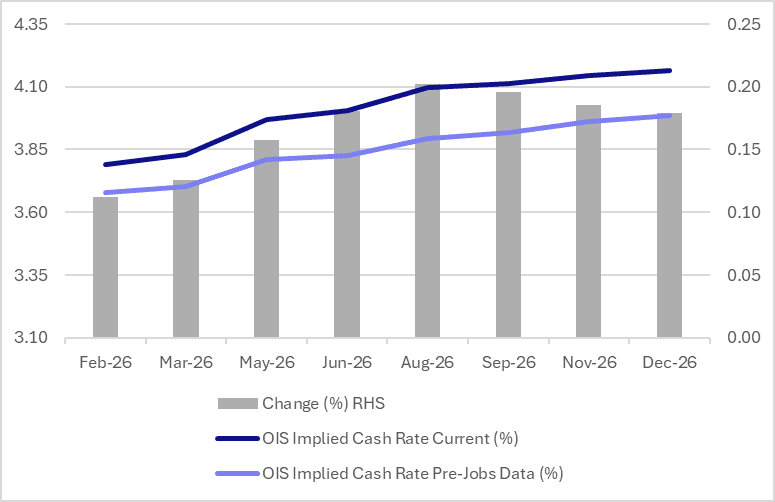

- OIS now reflects materially tighter policy expectations across the curve. A 25bp hike tomorrow is priced at a 77% probability (up from 32% pre-jobs data), with cumulative tightening probability of 166% by June (vs 88% pre-jobs) and 229% by December 2026 (vs 152% pre-jobs).

FOR THE FULL PUBLICATION PLEASE USE THE FOLLOWING LINK:

BONDS: NZGBS: Little Changed, Global Bonds Buoyed By Risk Off Sentiment

NZGBs closed little changed across benchmarks, with yields flat to 1bp higher.

- Cash US tsys are flat to 2bps richer, with a steepening bias, in today's Asia-Pac session after reversing early weakness amidst risk-off sentiment. US ISM Manufacturing PMI data will take focus on Monday, while markets will be attentive to developments over the US government shutdown and any potential comments from both Fed's Powell and Warsh ahead. The employment report for January on Friday.

- "NZ TREASURY SAYS INFLATION DATA DOESN'T SUGGEST OVERSTIMULATION" - BBG

- The 2-year swap rates closed slightly higher at 3.16%, the highest since July. For context, the rate sits some 70bps higher than mid-October levels.

- RBNZ-dated OIS pricing closed little changed across meetings. No tightening is priced for February, while December 2026 assigns 51bps.

- Tomorrow, the local calendar will see Building Permits data, ahead of Q4 Employment data on Wednesday.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond, NZ$175mn of the 4.25% May-34 bond and NZ$50mn of the 5.00% May-54 bond.

Bloomberg Finance LP

FOREX: USD - Trying To Push Higher, BBDXY Eyes 1195-1200

The BBDXY has had a range today of 1187.52 - 1190.03 in the Asia-Pac session; it is currently trading around 1189. The Dollar continued to pull back on Friday night as the move in Metals resulted in biblical pullbacks and the so-called “debasement trade” was put under pressure. The nomination of Warsh to Fed Chair has been of particular interest to the market due to his strong views on a smaller balance sheet and echoing Bessent's belief that the Fed has been involved in matters way outside of its purview. Warsh believes he can reduce the balance sheet and get interest rates lower, the market will be eagerly watching how he performs this magic trick. For the USD the market is left scratching its head a little as the break below 1180 proved to be false, it looks an ugly rejection below there and could imply the pullback has further to go. I suspect though that a bounce will find sellers again as the USD still has few friends. On the day, the first resistance is in the 1190-1195 area and then back towards 1200 where I suspect sellers would return in earnest.

- EUR/USD - Asian range 1.1840-1.1875, Asia is currently trading 1.1865. Price action has left an ugly bearish shadow on the weekly chart, and we might still get further retracements. On the day, the first support is between the 1.1800-1.1840 area initially a move through here would open up a deeper reversion back to the important 1.1700 area where I suspect buyers would again return. I suspect a bounce back toward the 1.19220-1.1950 area would find sellers first up as some risk is pared back across the board after such a big move.

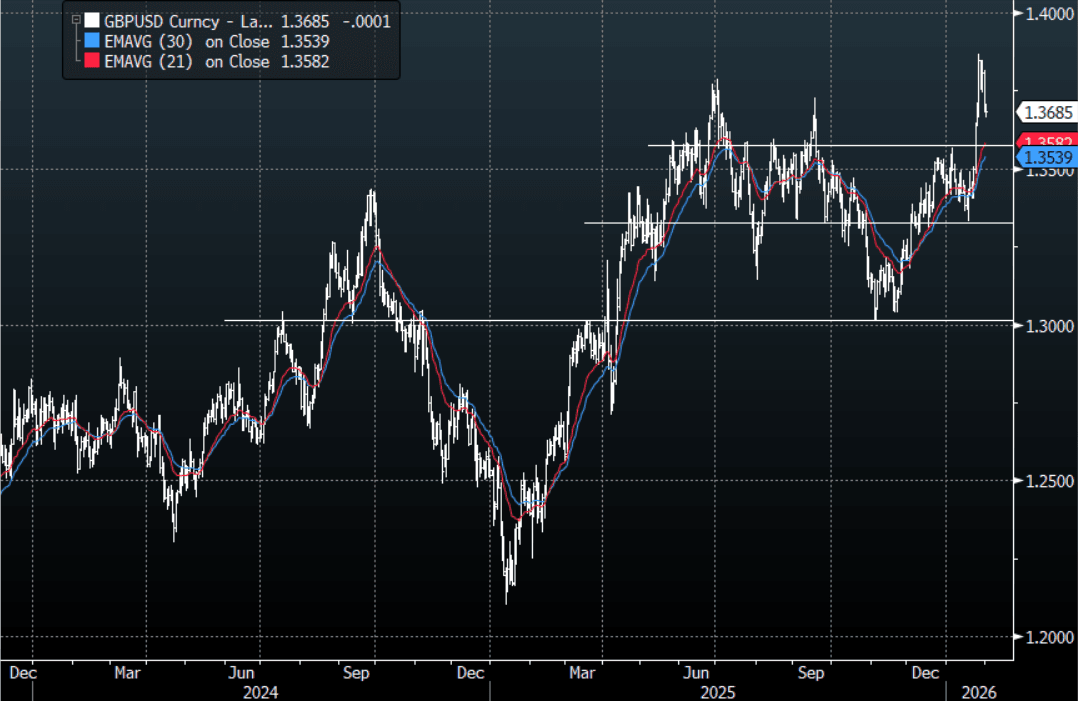

- GBP/USD - Asian range 1.3662-1.3706, Asia is currently dealing around 1.3685. The pair like everything else had an ugly weekly close leaving a clear rejection of the 1.3850 area. The price action suggests we could see some further retracements but I suspect buyers could reemerge on any decent dip. On the day, first support is 1.3600-1.3650 then the 1.3500 area.

- Cross asset : SPX -1.05%, Gold $4700, US 10-Year 4.23%, BBDXY 1189, Crude Oil $62.14

- Data/Events : Germany Retail Sales/HCOB Germany Manufacturing PMI, Italy HCOB Italy Manufacturing PMI/Budget Balance, Spain HCOB Spain Manufacturing PMI, EZ HCOB Eurozone Manufacturing PMI, France HCOB France Manufacturing PMI

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

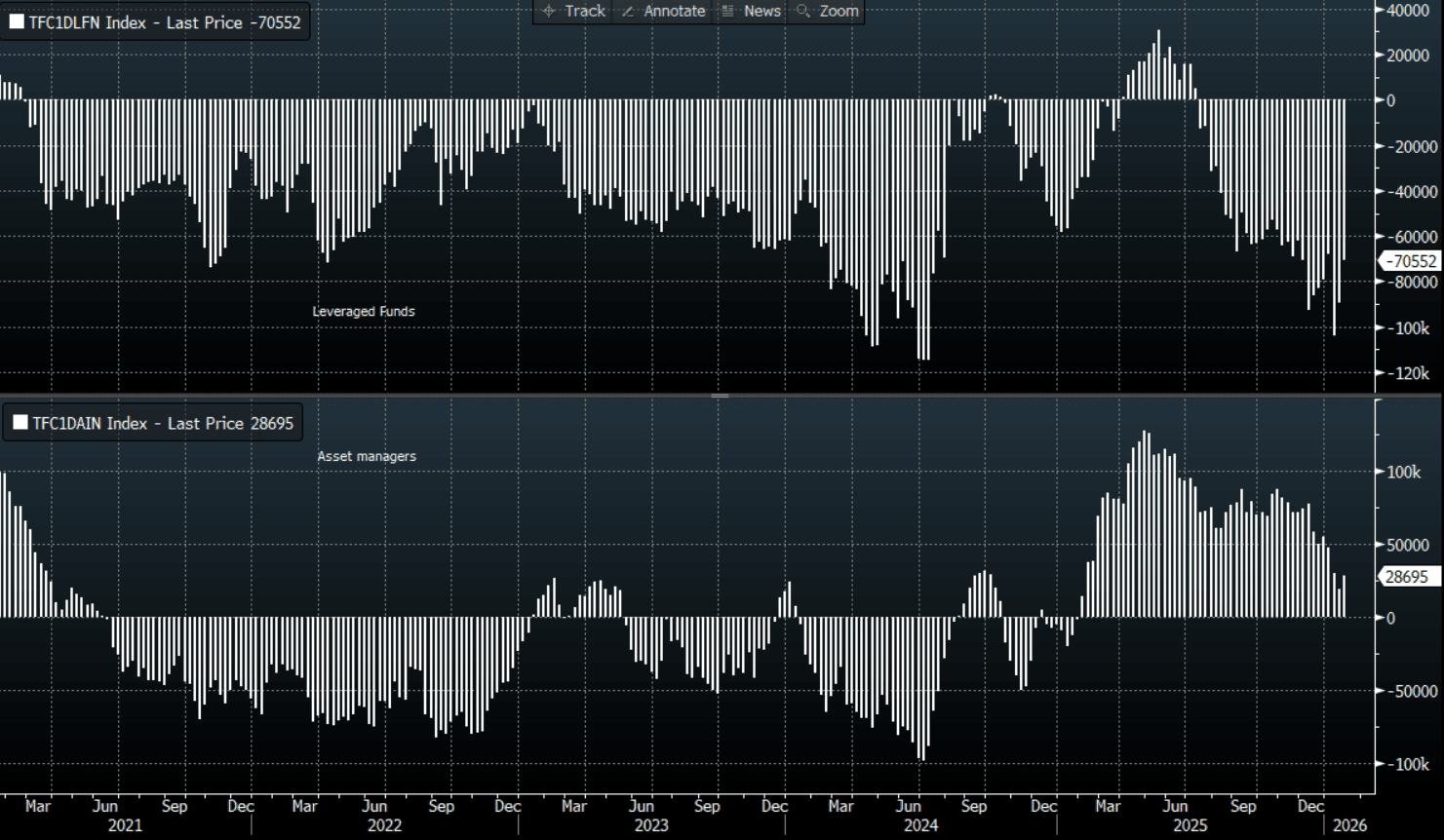

JPY: USD/JPY - Struggles Toward 155.50 As Takaichi Clarifies Yen Comments

The USD/JPY range today has been 154.82 - 155.51 in the Asia-Pac session, it is currently trading around 154.90, +0.05%. The USD/JPY move higher seemed to stall toward 155.50 today as risk turned meaningfully lower. CFTC data up until last Tuesday shows leveraged funds paring back large Yen shorts, this bounce back to 155-156 might provide good levels to further reduce positioning for CTA/Momentum type players. In today's session, watch to see if these positions are further reduced into the 155.00-156.00 area. The juggernaut speed it was building to the topside looks to have been broken for now and we might need to consolidate and do some work before embarking on a clear trend again.

- MNI: BOJ Opinions: Early Rate Hikes, Upside Risks to Prices. Several Bank of Japan board members saw the need to raise the policy interest rate relatively early, with one favouring hikes at intervals of a few months, according to the summary of opinions

- Bloomberg - "Japan's ruling bloc is poised to win 300 out of 465 seats in the upcoming election, an Asahi poll showed.”

- “Sanae Takaichi sought to clarify her earlier comments about the yen, saying Japan needs to create an economy that can withstand currency fluctuations.”

- CFTC Data up to 27/01/2026 shows Asset Managers started to add back to their reduced JPY longs, +28695(Last +19404). The Leveraged community continued to pare back their large shorts after the BOJ, –70552(Last -89657).

- Options : Close significant option expiries for NY cut, based on DTCC data: 155.00($570m), 155.70($530m). Upcoming Close Strikes : 153.00($1.23b Feb 5), 151.50($1.11b Feb 4) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 142 Points

Fig 1 : JPY CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

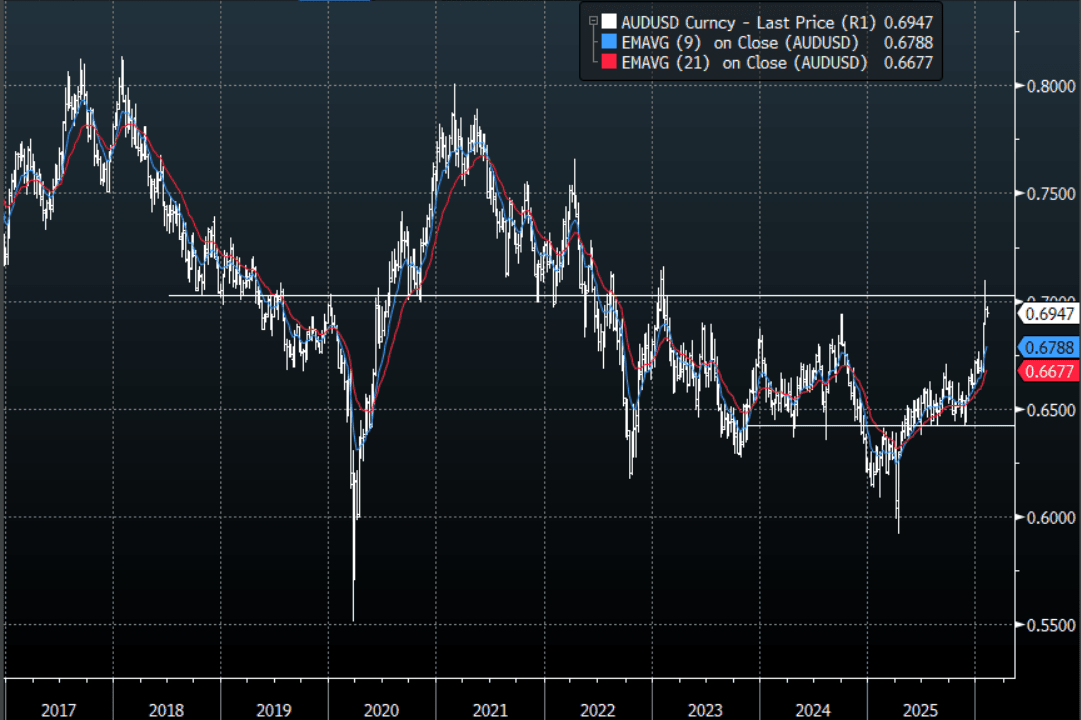

AUD/USD - An Ugly Weekly Close As Risk Starts The Week Under Pressure

The AUD/USD has had a range today of 0.6921 - 0.6971 in the Asia- Pac session, it is currently trading around 0.6945, -0.30%. Risk starts the week under some decent pressure, the AUD is consolidating around 0.6950 after the collapse in Metals and the bounce in the USD saw it put in an ugly rejection on the weekly chart. The AUD has been outperforming across the board as leveraged funds increase their longs anticipating a potential RBA hike tomorrow, but when we see an event like Friday night, the repercussions tend to cascade as traders are forced to pare back and deleverage risk across the board. My first instinct is to look for dips to be supported in the AUD but we might need to see how risk fares over the next couple of days as the move in metals could have some contagion and it could take a few days for its full implications to be seen. On the day, the first buy-zone is back toward the 0.6885-0.6915 area, if this does not hold we could see a deeper pullback toward 0.6800-0.6850. I suspect a bounce towards 0.7000-0.7030 could see sellers return initially as the market waits for the dust to settle. There looks to be some decent optionality between 0.6900-0.6950 which should see it do some work.

- MNI AU - OIS now reflects materially tighter policy expectations across the curve. A 25bp hike tomorrow is priced at a 77% probability (up from 32% pre-jobs data), with cumulative tightening probability of 166% by June (vs 88% pre-jobs) and 229% by December 2026 (vs 152% pre-jobs).

- CFTC Data up to 27/01/2026 shows Asset managers continued to reduce their shorts, -18983(Last -31659). The Leveraged community was again aggressively adding to newly built longs, +39860(Last +24741).

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6900(AUD474m), 0.6925(AUD304m), 0.6930(AUD325m). Upcoming Close Strikes : 0.6850(AUD886m Feb 5), 0.6950(AUD1.81b Feb 4) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 73 Points

Fig 1: AUD/USD spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

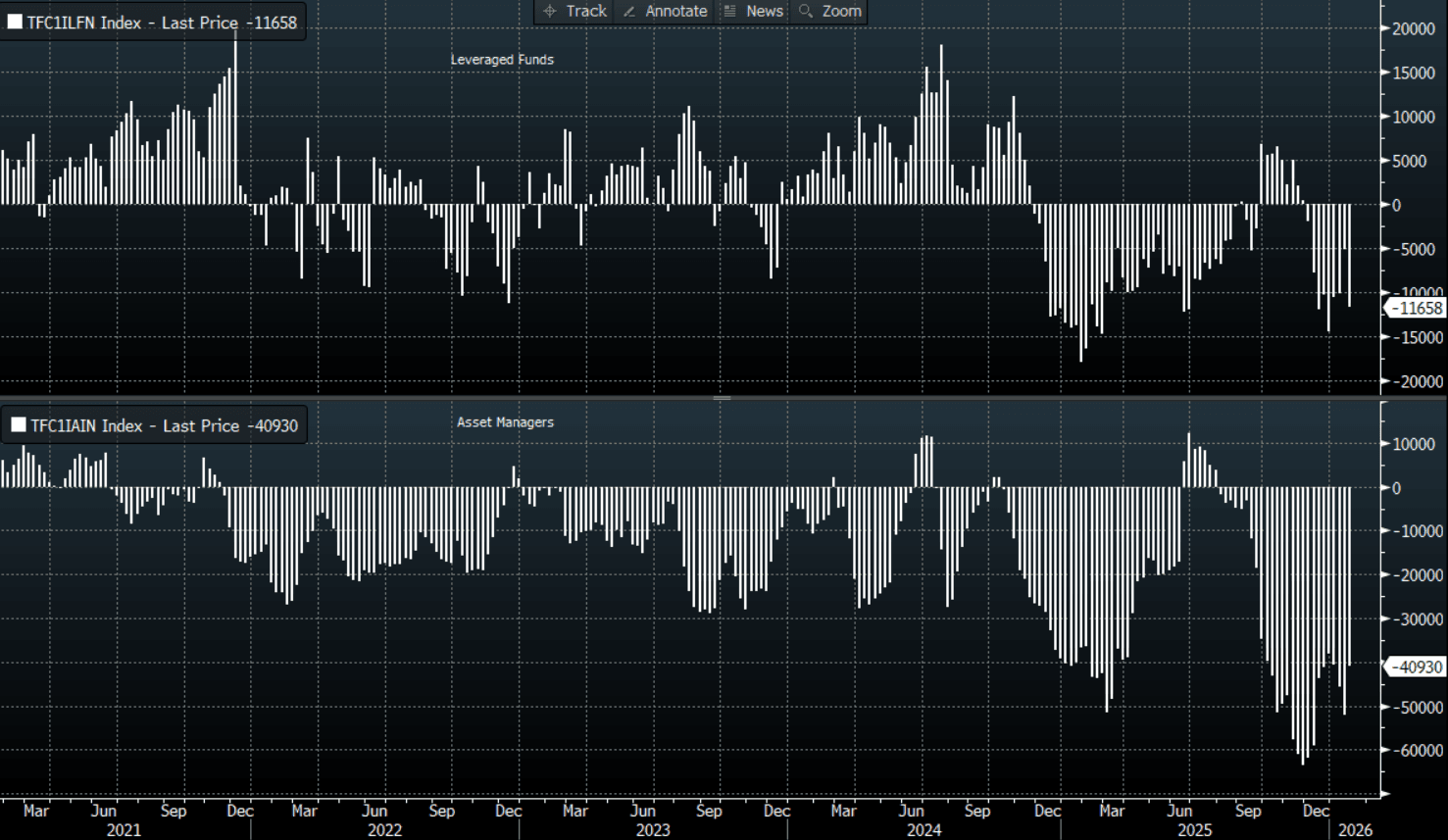

NZD/USD-Consolidates Above 0.6000 As Risk Starts The Week Under Pressure

The NZD/USD had a range today of 0.5993-0.6034 in the Asia-Pac session, it is currently trading around 0.6020, -0.02%. The NZD is holding just above 0.6000 for now even with risk starting the week under serious pressure. The NZD failed again just ahead of 0.6100, the collapse in Metals and the bounce in the USD saw it retrace on Friday. Like the AUD my first instinct is to look for dips to be supported in the NZD but we might need to see how risk fares over the next couple of days as the move in metals could have some contagion and it could take a few days for its full implications to be seen. On the day, the first support is right here 0.5980-0.6010 and then 0.5900-0.5950. I suspect a bounce back toward 0.6050-70 could now see some sellers first up. I was surprised by the CFTC data as the price action suggested there had been much more paring back of shorts but as of yet the bears seem to be holding on.

- "NZ TREASURY SAYS INFLATION DATA DOESN’T SUGGEST OVERSTIMULATION" - BBG

- MNI AU - China PMI MFg Cools View of Imminent Rate Cuts: China's PMI Manufacturing for private and export companies expanded more than expected in January. Following on from the strong rebound in Industrial Profits in December, this for some is further support for the view that there are no imminent changes in policy to support the economy. PMI Mfg was forecast to stay just in expansion at +50, and whilst +50.3 does not suggest the expansion is significant it may be enough to cool expectations on policy ahead of lunar new year.

- CFTC Data up to 27/01/2026 shows Asset Managers paring back their short positions in the NZD, -40930(Last -52099). The Leveraged community surprisingly added back to their own shorts which they had just started to wind down, -11658(Last -5119).

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5800(NZD887m Feb 3), 0.5975(NZD746m Feb 4) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 58 Points

Fig 1: NZD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

FOREX: CFTC FX Positioning - Firms Moves Against The USD To Jan 27

Last week's CFTC FX positioning update saw leveraged net USD selling across most of the major currencies, see the table below. This data is up to date for Jan 27 (last Tuesday). The BBDXY index hit fresh cycle lows Jan 27, near 1173.5. We bounced firmly into the weekend though (back above 1188) as the Fed Chair pick of Warsh contributed to sharp metals weakness.

- To last Tuesday we saw net leveraged buying JPY, EUR and GBP, as well as AUD. For JPY this continues to bring us away from somewhat stretched leveraged shorts, but at -70.5k we can still see further paring of shorts on USD/JPY spikes.

- EUR net buying saw the outright position in the leveraged space move into a modest long. AUD and GBP net longs were extended. NZD net selling by leveraged contracts bucked these trends though.

- In the asset manager space, net USD selling was evident across all the major currency pairs. Addition to CAD longs was the standout. Net shorts are still evident for GBP, AUD and NZD in the asset manager space.

Table1: CFTC FX Positioning By Major Currency - Weekly Change & Outright

| Leveraged Contracts | Asset manager Contracts | |||

| Weekly Change | Outright Position | Weekly Change | Outright Position | |

| JPY | 19105 | -70552 | 9291 | 28695 |

| EUR | 14660 | 1351 | 14337 | 419933 |

| GBP | 6978 | 51727 | 7622 | -78831 |

| AUD | 15119 | 39860 | 12676 | -18983 |

| NZD | -6539 | -11658 | 11169 | -40930 |

| CAD | 8737 | -49247 | 20470 | 26314 |

| CHF | -553 | -853 | 2618 | -53069 |

| MXN | -13172 | 52662 | 5096 | 82066 |

Source: CFTC/Bloomberg Finance L.P./MNI

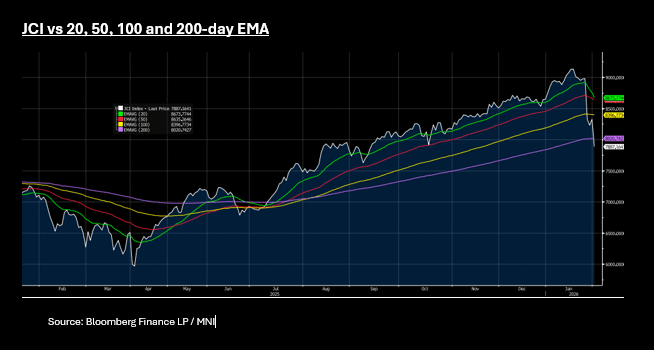

ASIA STOCKS: Ripple Effect Through Stocks, Profit Taking on AI Adding

The ripple effect of the new FED Chair markets has followed through to stocks, creating downward pressure amidst on over valued markets as losses mount. A huge day of losses Friday across precious metals included a 25% decline in silver and near 10% in gold, the knock on effects rippling through Aia stocks with all major markets lower. Tech stocks were in line today with headline names like Softhank (-2.7%), SK Hynix (-5.2%), Samsung (-4.1%) and TSMC (-1.4%) dragging their bourses lower as the Nvidea CEO clarified his investment forecasts for AI . Asia's equities are correlated to US interest rates and a historic analysis of new Fed Chair Warsh, shows him to be a hawk. This is at odds with Trump's desire for lower rates and that push pull is a further input to volatility. The NIKKEI was a standout earlier rising over 1% following polls suggesting PM Takaichi was likely to secure a lower house majority, though those gains fizzled out into the afternoon.

Sentiment appears fragile and with such positivity priced into many markets, with the possibility of further volatility as profit takers step in. Again the problems were focused in Jakarta as the JCI was the biggest faller, down over 5%, with the KOSPI down by -3.4% for its biggest one day decline since November. The JCI has fallen below all major moving averages over the course of four trading days, as outflows from stocks ramp up. News of regulatory changes to increase equity allocations for funds will do little for now to help.

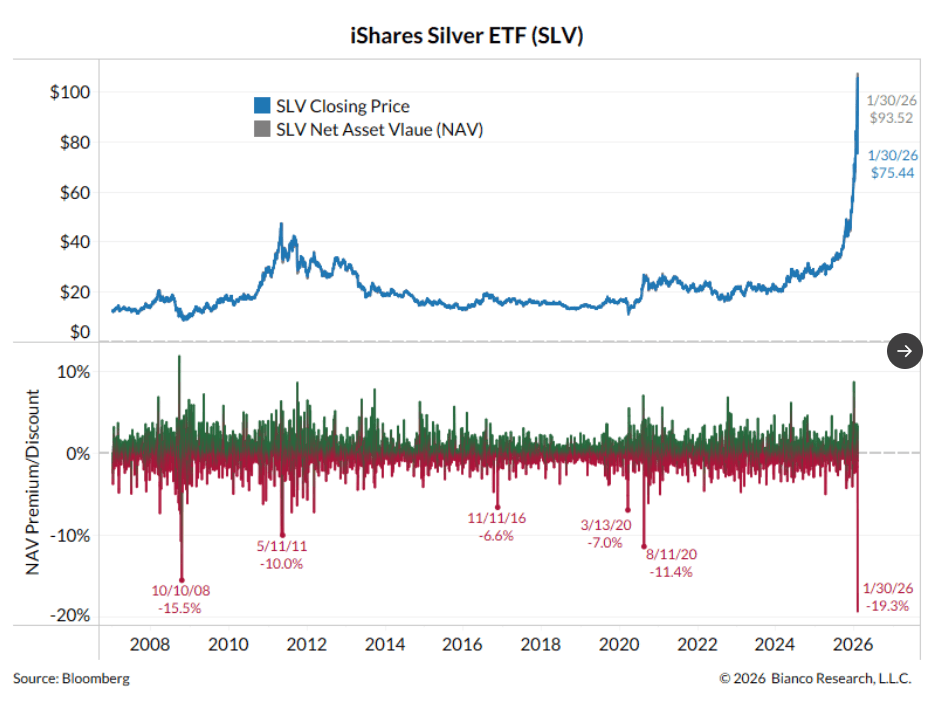

PRECIOUS METALS: Silver - Collapses Over 37% On Friday Causing Mass Deleveraging

The range Friday night for XAG was $73.97 - $109.511, Asia is currently trading around $81, -4%. The move had looked overdone but the timing of these pullbacks when things are going parabolic are always tough, but I am sure even the most vocal naysayer would not have been calling for a 37% collapse in a day. A truly monumental move that will have caused a VAR shock right across the market. There will be lots of calls to now use this dip to enter longs but my experience tells me when you have a move of this magnitude it takes a few days if not a couple of weeks to truly see the ramifications of this unprecedented move. All retail stops would have been done at the lows but the larger investment positions would not have been able to exit in any size due to the pace and lack of liquidity seen in that move. I feel should we get any sort of a bounce it will be used to fade initially as the longs that are still caught will want to pare back risk given the move we just saw. On the day, look for sellers back toward $90-$94 and then $100-$105, buyers have been seen just below the $75k area and is holding up for now. The first support is in this $70-$75k area a break below here could signal a deeper pullback toward $55-$60. This move is all about positioning and moves like this tend to squeeze everyone out before finding a base so I would not be fading this move initially but rather be patient and let the capitulation play out. Liquidity has obviously completely disappeared so it will be no surprise to continue to see swings of between 10-15% over the coming days as this continues to play out.

- The XAG Average True Range for the last 10 Trading days: $15.07

- Jim Bianco on X: “Yesterday's 19% discount to NAV broke the record set on 10/10/2008, the day the TARP was introduced during the Global Financial Crisis. Before Friday's collapse, SLV had about $60 billion in assets. The chart below shows that the silver market is now broken, meaning there is a high risk that a financial firm heavily involved in this market is either bankrupt (causing the large discount above) or in serious trouble (due to the large discount above). It doesn't mean we will automatically see a firm fail, but the silver market needs to correct itself quickly; otherwise, it probably will. Quickly correct itself = Monday or Tuesday.” See graph below

- Bloomberg - "Chinese metals traders have racked up losses totaling at least 1 billion yuan ($144 million) after one of their counterparties fled the country leaving deals unfinished, alarming top regulators worried about hidden financial risks, according to people familiar with the matter.”

Fig 1 : Silver ETF(SLV)

Source: MNI - Market News/@biancoresearch

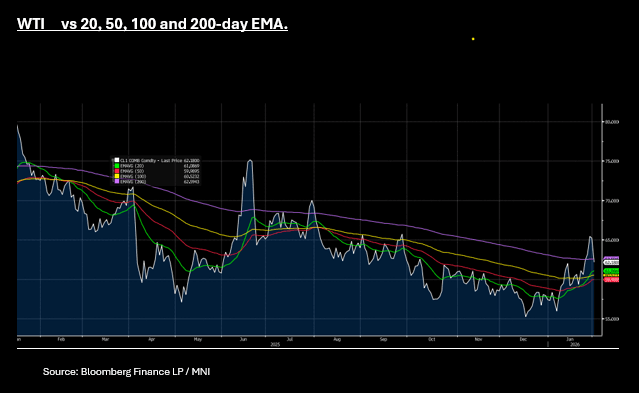

OIL: Geopolitics Sidelined as Risk-Off Hits Oil

- A global risk off sentiment followed through into oil Monday with WTI and Brent both down heavily.

- WTI is down -4.6% at US$62.16 bbl, trading through the 200-day EMA of $62.59. Below is downside resistance via the 20-day EMA of $61.08

- Brent is down -6.3% to $66.22, having held above $70 bbl only briefly. Brent is now near to the 200-day EMA and further falls below could bring the 20-day EMA into play at $65.74

- OPEC's decision to maintain its pause in supply when WTI / Brent are both c. 18% higher than their December lows comes at an interesting time in global oil politics.

- Investors are navigating a "Trump put" on energy, as the administration prioritizes lower prices (targeting $50/bbl or lower) to manage inflation in a world of tightened sanctions on Russia and redirected Venezuelan flows shifting global trade patterns.

- The underlying market narrative remains bearish due to a projected surplus. However adding to the supply considerations is severe weather related disruptions in the US, outages in Kazakhstan and Libya and investors who had loaded up on bearish bets for oil.

- The wash out in markets began with the FED Chair announcement and key markets like precious metals have been hit hard. This will have a knock on effect as portfolio adjust. Look for oil markets to re-focus on the mounting risks in the Middle East.

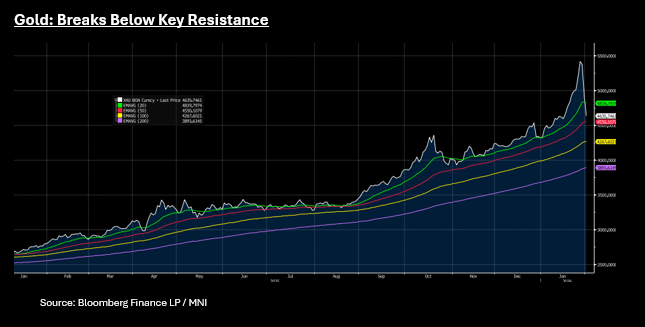

Gold's Vol to Stay as Portfolios Adjust

- Gold's decline continues Monday as the 'Warsh effect' as a saying now comes into being. Markets perceive Warsh as more hawkish, leading to expectations of a smaller Fed balance sheet and a focus on combating inflation, whilst uncertain about the path of interest rate.

- Gold is arguably one of the most crowded trades in markets at present following a surge in 2025 of more than 60% and a record-breaking start to 2026 taking bullions price on momentum indicators to the most over bought in more than a decade.

- Due for a correction, gold fell sharply post Warsh's announcement and that has followed on into Asia where it is down -5.7% currently.

- Gold's rise had reached over 20% year to date and has fallen 15% from the peak of US$5,417.21. Gold has fallen below the 20-day EMA of $4,819, with downside resistance via the 50-day EMA at 4,550.

- This will take several days to wash out as positioning was heavily skewed for further appreciation. This may cause knock on effects across other assets as portfolios are rebalanced even when the longer term structural reason for gold's ascent has not changed.

ASIA FX: KRW, TWD Slump With Equities, CNH Outperforms On Reserve Goal

In North East Asia FX, we have seen strong USD gains against KRW and TWD. USD/CNH has traded slightly lower, amidst a weaker than forecast USD/CNY fixing and onshore media highlighting China's desire around the yuan as a global reserve currency. KRW and TWD are weaker, amid broader risk off, which has impacted local equity market sentiment. Focus remains on sharp metal losses, but recent winning trades, like those in South Korea and Taiwan equities, could also be impacted.

- USD/CNH spot found early selling interest above 6.9600, which was close to the 20-day EMA resistance point. Dips under have been supported, but CNH has meaningfully outperformed the likes of KRW and TWD (and broader USD gains from Friday's session). the USD/CNY fix was set below the market estimate for the first time since late Nov last year, indicating scope for yuan outperformance amidst firmer USD trends. The weekend China press also highlighted China's desire for the yuan to be a global reserve currency. Via BBG: "Xi's remarks, published in the Qiushi magazine, emphasize the need for a powerful currency, widely used in international trade, investment and foreign exchange markets, holding the status of a global reserve currency."

- Spot USD/KRW got close to 1460 in earlier dealings, but sits slightly lower now. The pair is back above all key EMAs, but we might expect to see increased official resistance/FX jawboning on a return in the 1460/80 region. Local equities have slumped, the Kospi last down nearly 4%, with potential profit taking in the tech related/AI space in play, as contagion from the metals slump spills over. Offshore investors have been large sellers of local stocks today after strong outflows of nearly $1.5bn on Friday.

- Spot USD/TWD is back in the 31.60/65 region, close to Jan highs (near 31.70). Upside focus is likely to rest around the 32.00 region, where we broke under in early May last year.

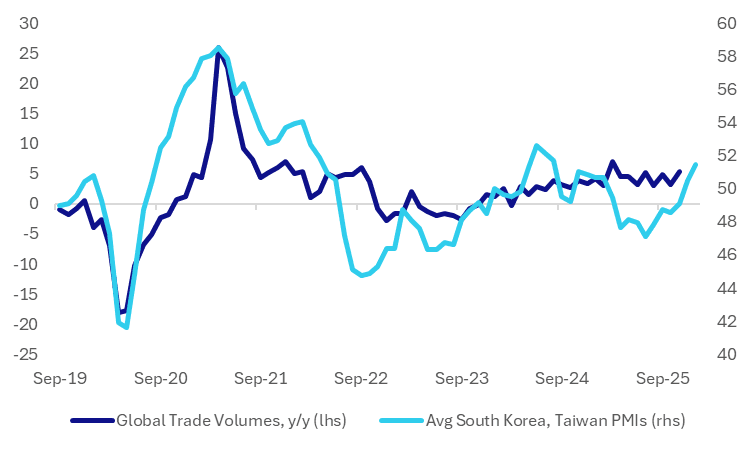

ASIA: SK, Taiwan PMIs Recover Further, Supporting Global Trade Outlook

Trade bellwethers South Korea and Taiwan both saw improvements in their respective PMI reads for Jan. The South Korean print rose to 51.2 from 50.1 in Dec 2025. Taiwan's PMI rose to 51.7 from 50.9 prior. The chart below plots the average of the PMIs for these two countries, plotted against global trade volume growth y/y. The improved PMI backdrop is pointing to better global trade growth. We have already had Jan export growth for South Korea, released yesterday, which showed export growth above 30%y/y. Tech/AI related demand remains strong for both economies.

- In terms of the detail, for South Korea, its PMI is the highest read since Aug 2024. New orders were also up, best reading since June 2024.

- Output also moved into expansion of 51.5, versus the 49.3 Dec read.

- For Taiwan, it was a similar outcome, with new orders up to the highest level since Feb 2025.

Fig 1: South Korea, Taiwan Average PMI Print & Global Trade Volumes, y/y

Source: S&P/Bloomberg Finance L.P./MNI

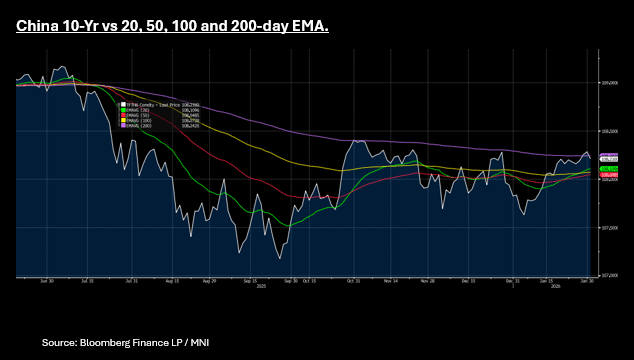

CHINA: Bond Futures Break Lower, Expect Liquidity Injection in Coming Days

- China's bond market is not reacting the usual way to the down day for stocks, with a general risk off sentiment across the board Monday.

- Futures are down -.07 in the 10-year to 108.21 and -.01 in the 2-Yr to 102.38 whilst the CGB 10-YR is up +.05bps to 1.815%

- The move lower in the 10-Yr takes it back below the 200-day EMA of 108.24, which it rallied above briefly last week on liquidity injections. Downside resistance now in the form of the 20-day EMA is at 108.10. Issuance this week is focus on CNY45bn of 182-bills on 03 Feb, CNY130bn of 2027 bonds 04 Feb, CNY 120bn of 2027 bonds 06 Feb and CNY32bn of 2056 bonds 06 Feb.

- With some large maturities in the coming days and the auctions, there is a growing likelihood of liquidity injections to stabilize bond markets and support the issuance.

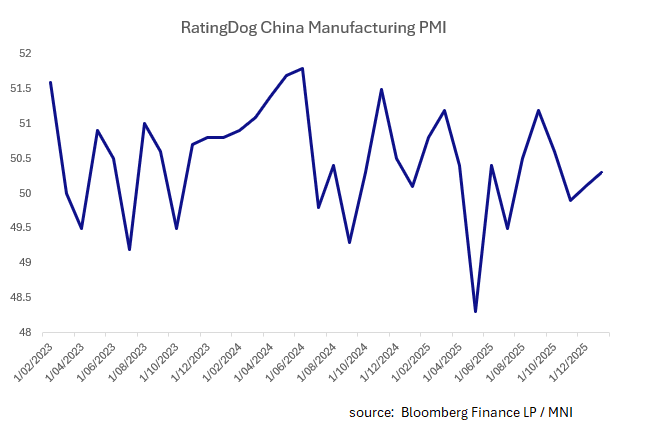

CHINA: PMI MFg Cools View of Imminent Rate Cuts

- China's PMI Manufacturing for private and export companies expanded more than expected in January. Following on from the strong rebound in Industrial Profits in December, this for some is further support for the view that there is no imminent changes in policy to support the economy.

PMI Mfg was forecast to stay just in expansion at +50, and whilst +50.3 does not suggest the expansion is significant it may be enough to cool expectations on policy ahead of lunar new year, as output rises to 50.6 vs 50.5 in Dec whilst new orders fall vs prior month.

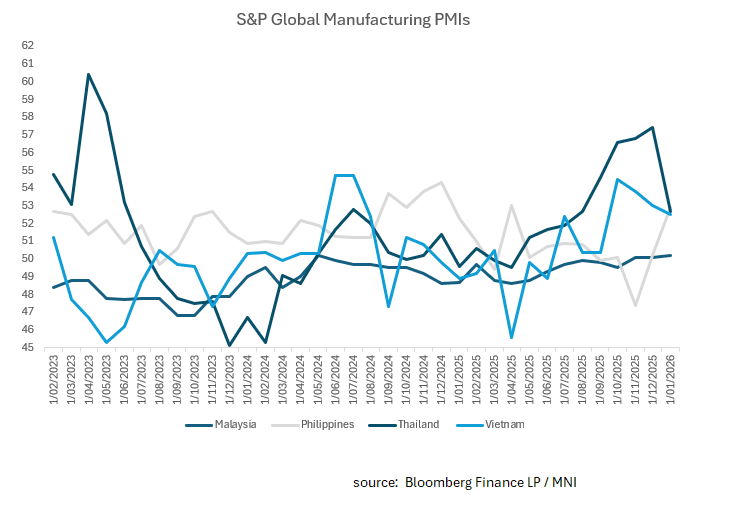

ASIA: Mixed Bag for PMIs, BSP's Bias to Cut Remains

- A mixed bag for regional PMI Manufacturing today with Malaysia and the Philippines up modestly, whilst Thailand and Vietnam were down on the prior month.

- According to forecasts, the Philippines (Bangko Sentral ng Pilipinas) and Thailand (Bank of Thailand) are the most likely to cut rates within the next three months, following their established easing cycles from late 2025.

- In contrast, Malaysia and Vietnam are expected to remain on hold or even face upward pressure on rates.

- Malaysia's January PMI was +50.2, from +50.1; Philippines +52.9 from +50.2 whilst Thailand was +52.7 from +57.4 and Vietnam +52.5 from +53.0

- The BSP has been Asia's most aggressive in rate cuts, having reduced its policy rate by a total of 200 basis points (to 4.5%) as of December 2025. The BSP chief signaled a potential pause in early 2026 to monitor the peso's stability an additional 25-basis-point cut is forecast by major banks for the second quarter of 2026 given low inflation.

- The Bank of Thailand shifted to an easing stance in late 2025 to address a significant economic slowdown, and is expected to maintain an easing bias through early 2026 due to soft growth and muted inflation, though with rates at 1.25%.

- Malaysia forecasts for 2026 so far point to no move from the BNM for the year, given the robust outlok for the economy.

- Vietnam could see rates going the other way in time to support its currency.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 02/02/2026 | 0700/0800 | ** | Retail Sales | |

| 02/02/2026 | 0815/0915 | ** | S&P Global Manufacturing PMI (f) | |

| 02/02/2026 | 0815/0915 | ** | Retail Sales | |

| 02/02/2026 | 0845/0945 | ** | S&P Global Manufacturing PMI (f) | |

| 02/02/2026 | 0850/0950 | ** | S&P Global Manufacturing PMI (f) | |

| 02/02/2026 | 0855/0955 | ** | S&P Global Manufacturing PMI (f) | |

| 02/02/2026 | 0900/1000 | ** | S&P Global Manufacturing PMI (f) | |

| 02/02/2026 | 0930/0930 | ** | S&P Global Manufacturing PMI (Final) | |

| 02/02/2026 | 1145/1145 | BOE Breeden on Payments | ||

| 02/02/2026 | 1445/0945 | *** | S&P Global Manufacturing Index (final) | |

| 02/02/2026 | 1500/1000 | *** | ISM Manufacturing Index | |

| 02/02/2026 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 02/02/2026 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 02/02/2026 | 1730/1230 | Atlanta Fed's Raphael Bostic | ||

| 03/02/2026 | 0030/1130 | * | Building Approvals | |

| 03/02/2026 | 0330/1430 | *** | RBA Rate Decision | |

| 03/02/2026 | 0700/0200 | * | Turkey CPI | |

| 03/02/2026 | 0745/0845 | *** | HICP (p) | |

| 03/02/2026 | 0745/0845 | Budget Balance | ||

| 03/02/2026 | 0900/1000 | ** | ECB Bank Lending Survey | |

| 03/02/2026 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 03/02/2026 | 1300/0800 | Richmond Fed's Tom Barkin | ||

| 03/02/2026 | 1355/0855 | ** | Redbook Retail Sales Index |