MNI EUROPEAN MARKETS ANALYSIS: Risk Off Aids US Tsy & JGBs

- Risk sentiment has traded with a softer tone in Asia Pac hours, as markets await for the US re-open after the long weekend. Silver and gold are weaker, along with US equity futures. JPY has outperformed in the FX space, while oil prices hold near recent Monday highs, ahead of a US-Iran meeting.

- US Tsy yields have re-opened and are tracking lower, while JGBs are also in demand, despite a lacklustre 5-year auction.

- Much of the Asia region was out today for the Lunar New Year break, which has likely impacted liquidity.

- UK labour market data and Canada CPI data are the highlights later on.

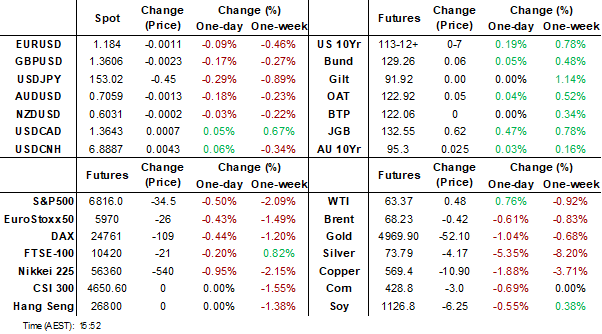

MARKETS

US TSYS: Yields Lower on JGB Lead, FOMC Minutes Next Focus

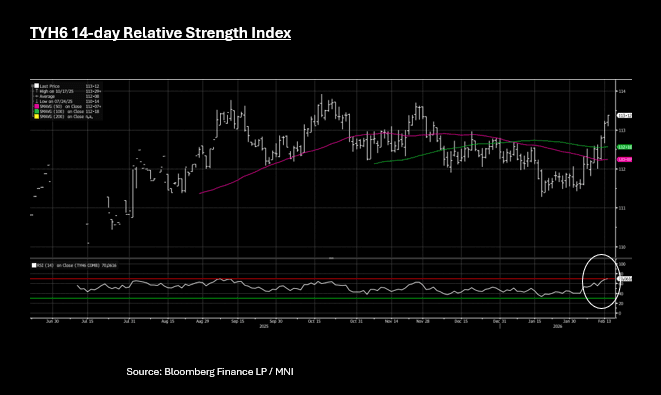

US bond futures posted reasonable gains Tuesday with the 10-Yr up +07 in Asia at 113-12+ This takes TYH6 to overbought on the 14-day relative strength index having rallied since early February. US bond markets were generally stronger in thin markets on JGB leads and positioning ahead of FOMC minutes.

Cash was open post the President's day holiday in the US with a mixed start turning into a decent rally by mid afternoon as curves flattened further.

- The 2-Yr is down -1.7bps at 3.393%

- The 5-Yr is down -2.8bps at 3.580%

- The 10-Yr is down -2.5bps at 4.025%

- The 30-Yr is down -2.4bps at 4.673%

Market signals in Asia are difficult to interpret and for a clearer guide for the US re-opening. US equity futures are pointing to a modestly positive open as bond markets ready for the next wave of data. 4.00% for the 10-Yr is the next key resistance level should the positive momentum continue.

Tomorrow sees ADP up to Jan 31, Empire Manufacturing and NAHB housing index. Q4 GDP / PCE/ flash PMII are key and out Friday

JGBS: Bull-Flattener Has Curve Testing Bottom Of Range

JGB futures are stronger and at session highs, +50 compared to settlement levels, despite a lacklustre 5-year auction.

- Today’s 5-year JGB auction sent mixed demand signals. The low price undershot expectations at 99.80, while the bid-to-cover ratio edged up to 3.0961x from 3.0811x. Meanwhile, the tail narrowed to 0.03 from 0.05, suggesting a modest improvement in pricing tension despite the softer price outcome.

- Risk-off sentiment has buoyed global bonds, with cash US tsys are 1-2bps richer in today's Asia-Pac session after yesterday's holiday.

- Cash JGBs have bull-flattened across benchmarks, with yields 3-9bps lower. The benchmark 10-year yield is 6.8bps lower at 2.146% versus the cycle high of 2.359%.

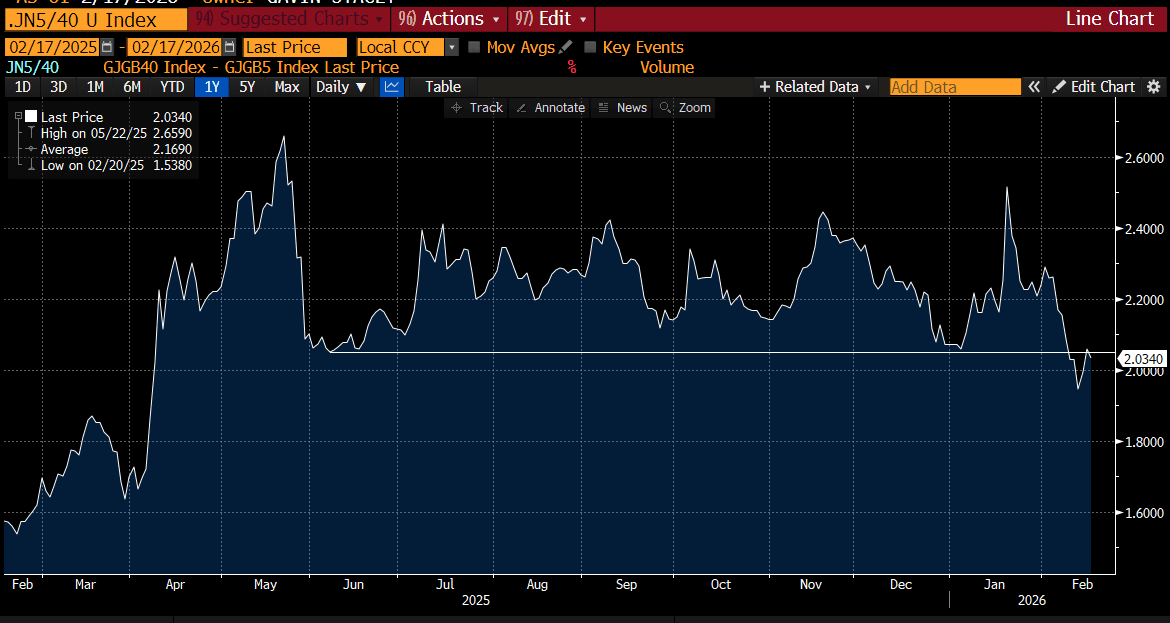

- Today’s move sees the 5/40 yield curve re-test the former breakdown level, following last Friday’s decisive move through the bottom of its well-established trading range.

- Swap rates are 3-6bps lower, with a flatter curve.

- Tomorrow, the local calendar will see Trade Balance data.

Source: Bloomberg Finance LP

AUSSIE BONDS: Richer With Risk-Off, Q4 Wages Tomorrow With Jobs Data On Thu

ACGBs (YM +3.5 & XM +2.5) are stronger and near session bests.

- The RBA minutes from the Feb policy meeting noted re the inflation outlook: "the central projection for inflation had been revised materially higher, remaining above target throughout 2026 and only returning close to the midpoint of the target range around mid-2028 (on the assumption that the cash rate follows the market path)."

- This points to a fairly high bar, or meaningful downside inflation surprises in Q1, for the RBA not to act further. Still, the concluding paragraphs from the minutes show the RBA is not on a pre-determined rate path and will continue to assess the incoming data.

- Cash US tsys are 1-2bps richer in today's Asia-Pac session after yesterday's holiday.

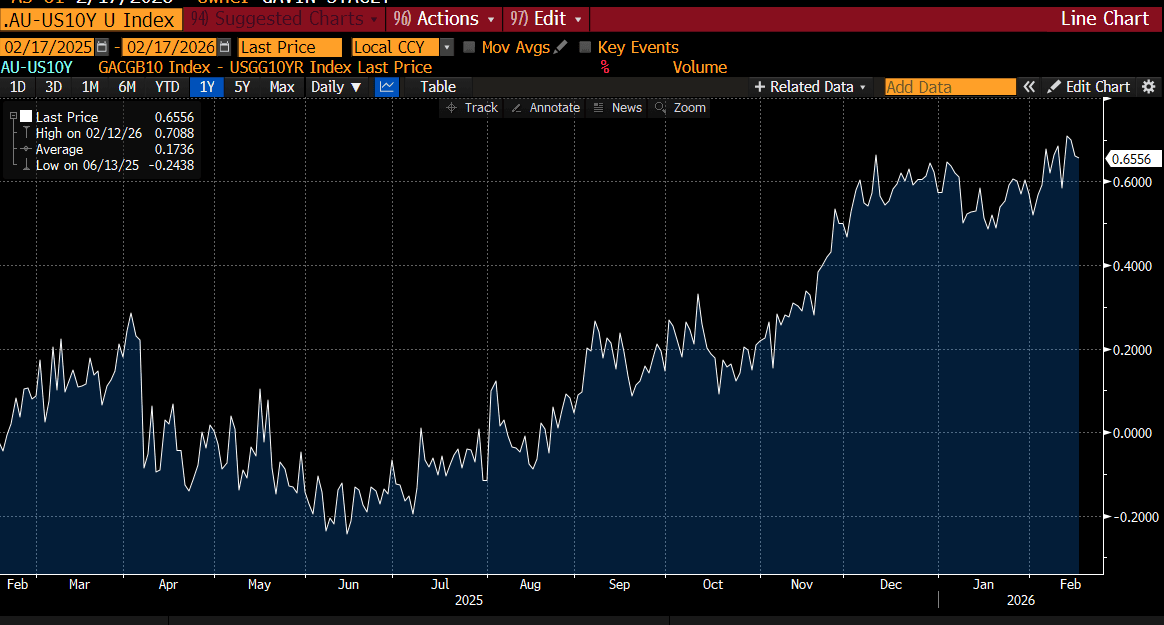

- Cash ACGBs are 2-4bps richer with the AU-US 10-year yield differential at +66bps, near cycle highs.

- The bills strip has bull-flattened, with pricing +2 to +4.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 13% for March to 82% by June and 129% by December 2026.

- The Q4 Wage Cost Index is due for release tomorrow with January's Employment Report on Thursday.

Bloomberg Finance LP

RBA: Mins Show Data Dependency, But Likely High Bar Not To Act Again

The RBA minutes from the Feb policy meeting noted re the inflation outlook: "the central projection for inflation had been revised materially higher, remaining above target throughout 2026 and only returning close to the midpoint of the target range around mid-2028 (on the assumption that the cash rate follows the market path)." This points to a fairly high bar, or meaningful downside inflation surprises in Q1, for the RBA not to act further. Still, the concluding paragraphs from the minutes show the RBA is not on a pre-determined rate path and will continue to assess the incoming data, see below for key excerpts.

Tomorrow, we get Q4 wages data. The market forecast is 0.8%q/q and 3.4%y/y (unchanged from Q3), while on Thursday Jan jobs data is out (+20k forecast, along with a 4.2% unemployment rate (4.1% was prior and Dec jobs growth was +65.2k). Jan inflation is out on Feb 25, while the Q1 print is due on Apr 29, which comes just ahead of the May policy meeting (May 5).

- RBA concluding comments from the Feb minutes: "members agreed that the prevailing uncertainties meant it was not possible to have a high degree of confidence in any particular path for the cash rate. They pointed to risks on both sides of the central projection for inflation. If demand growth proved weaker, supply capacity stronger, the pick-up in inflation largely a function of sector-specific shocks or the stance of policy more restrictive than believed, then inflation might abate more rapidly than projected. However, if demand growth continued to pick up, supply was more constrained than thought, longer term inflation expectations began to rise or policy was not restrictive, then inflation might prove more persistent than in the central case."

- Future policy decisions would need to respond to these evolving risks. Members noted that it was important to continue exploring what the incoming data reveal about their judgements in relation to these matters. "

- See the full minutes at this link.

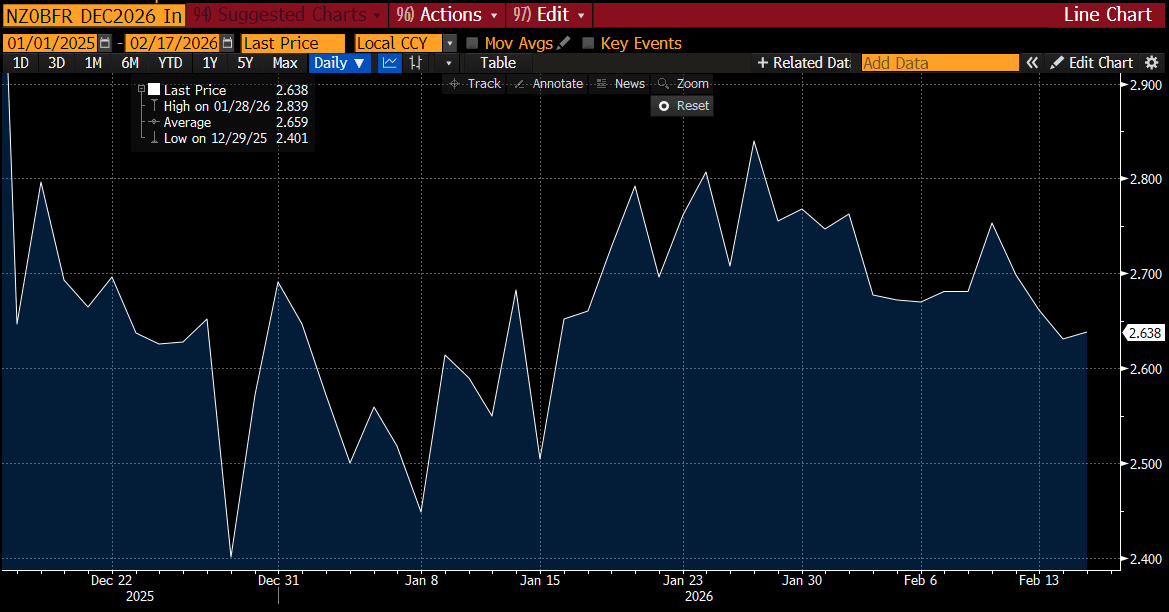

BONDS: NZGBS: Richer Ahead Of Tomorrow's RBNZ Policy Decision

NZGBs closed 2bps richer across benchmarks, wit the NZ-AU 10-year yield differential unchanged at -26bps.

- Cash US tsys are 1-2bps richer in today's Asia-Pac session after yesterday's holiday.

- Tomorrow, the local calendar will see PPI data ahead of the RBNZ Policy Decision.

- MNI RBNZ Preview-Feb 2026: On Hold, Hike Timing Key Focus: At tomorrow's RBNZ meeting the central bank is widely expected to keep rates on hold. The Bloomberg survey of sell-side economists shows all 22 economists see the policy rate being held at 2.25%. Our strong bias is also for no change tomorrow. If realized, this will leave the focus firmly on the outlook, particular on the RBNZ's new OCR path.

- The other focus point will be gauging new RBNZ Governor Breman's tone, as this will be her first rate setting meeting in charge. The RBNZ will also likely be cautious around sounding too hawkish around the outlook, which the market will likely judge via the implied OCR outlook path. (see MNI Preview here)

- RBNZ-dated OIS pricing closed little changed across meetings. No tightening is priced for tomorrow, while December 2026 assigns 39bps.

- On Thursday, the NZ Treasury plans to sell NZ$200mn of the 3.00% Apr-29 bond and NZ$250mn of the 4.50% May-35 bond.

Bloomberg Finance LP

RBNZ: MNI RBNZ Preview-Feb 2026: On Hold, Hike Timing Key Focus

- At tomorrow’s RBNZ meeting the central bank is widely expected to keep rates on hold. The Bloomberg survey of sell-side economists shows all 22 economists see the policy rate being held at 2.25%. Our strong bias is also for no change tomorrow. If realized, this will leave the focus firmly on the outlook, particular on the RBNZ’s new OCR path. The other focus point will be gauging new RBNZ Governor Breman’s tone, as this will be her first rate setting meeting in charge.

- The RBNZ will also likely be cautious around sounding too hawkish around the outlook, which the market will likely judge via the implied OCR outlook path. We would be surprised if the OCR path is more hawkish than current market pricing, which implies a policy rate near 2.65% by year’s end (versus the current rate of 2.25%). The NZD TWI is up over 4% from Nov 2025 lows, while local rates have also risen. A further material tightening of financial conditions could put the economic recovery in jeopardy. This is also where Breman’s tone is likely to be watched closely in terms of keeping the policy outlook flexible.

- See this link for our full preview:

NEW ZEALAND: Food Prices Surge In Jan, But Other Components Mostly Down M/M

For Jan, NZ food prices surged 2.5%m/m, the strongest rise monthly rise since Jan 2022. Jan does tend to be a strong month for m/m rises, with Jan 2025 seeing a 1.9%m/m gain in food prices. In y/y terms, food prices are up 4.6%, versus 4.0% in Dec, but this is still below 2025 highs of 5.0%. Outside of food, other monthly price change updates were close to flat or down on Dec outcomes. The RBNZ meets tomorrow, with no change widely expected. Focus will be on the timing of the first hike, with the central bank still likely to signal a wait and see approach, given spare capacity in the economy. Given what is already priced by the market (38bps for Dec 2026), the central bank is unlikely to give a more hawkish view versus current pricing.

- Rents were flat, while electricity rose 0.3%m/m (prior +1.5%). Petrol prices were down -2.4%m/m (after +0.1m/m prior), while diesel and gas prices also fell in the month. Domestic and international air travel both fell, but this followed strong surges in Dec last year. Accommodation services fell -7.8%m/m in Jan.

- In y/y terms, outside of food, the other price components saw softer y/y momentum, see below.

- Food: 4.6%y/y (prior 4.0%)

- Rent: 1.2%y/y (prior 1.3%)

- Electricity: 11.5%y/y (prior 12.2%)

- Petrol: -4.8%y/y (prior 1.4%)

- Domestic air travel: -5.5% (prior -1.2%)

- International air travel: 4.0%y/y (prior 6.6%)

- Accommodation services: 1.4%y/y (prior 12.1%).

FOREX: USD - BBDXY Trades Sideways, If Risk Corrects Can The USD Rise ?

The BBDXY has had a range today of 1182.95 - 1183.83 in the Asia-Pac session; it is currently trading around 1183. The USD is drifting sideways below 1185. How will risk open today in the New York session? If it starts to build on the pullback that started last week does the USD find a bid? The market is very bearish the USD so if we should get some form of a deeper correction in risk and the USD finds demand as a hedge, the market is not positioned for this. On the day, the first resistance remains toward the 1185-1187 area and then 1195 where I suspect we could see sellers return initially. A sustained break below 1175-1180 is needed to potentially signal the start of another leg lower. While the market waits for clarity around the pullback in risk the BBDXY looks to be stuck in a 1177-1187 range.

- EUR/USD - Asian range 1.1838-1.1854, Asia is currently trading 1.1840. The pair continues to trade sideways around 1.1850 albeit with a slightly heavy tone. Price action remains constructive, can it build a base above 1.1800 and then find the momentum to push on? On the day, the first support is toward 1.1820-1.1840 and then the 1.1750-0.1780 area. A sustained move back above 1.1925-1.1940 is needed to give it the thrust it needs to have another look toward the 1.2000 area.

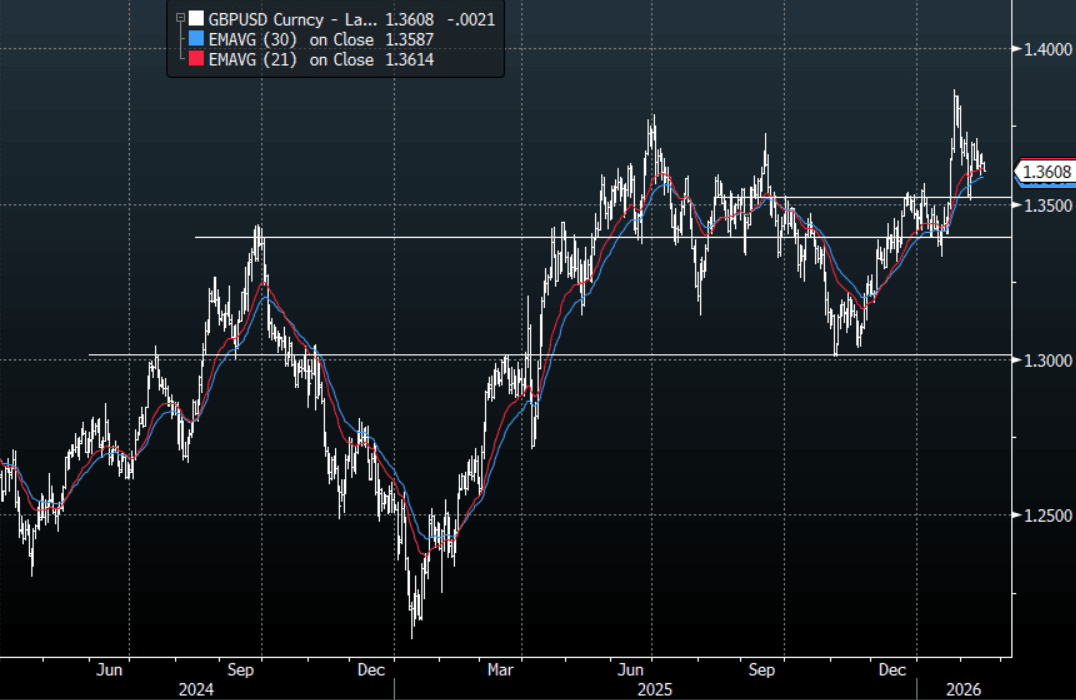

- GBP/USD - Asian range 1.3606-1.3635, Asia is currently dealing around 1.3610. GBP continues to look like 1.3580-1.3730 to me for now as we wait to see how the big USD trades when the US returns from its day off.

- Cross asset : SPX -0.40%, Gold $4955, US 10-Year 4.03%, BBDXY 1183, Crude Oil $63.50

- Data/Events : Germany CPI/ZEW Survey Expectations, EZ ZEW Survey Expectations, Italy Trade Balance

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

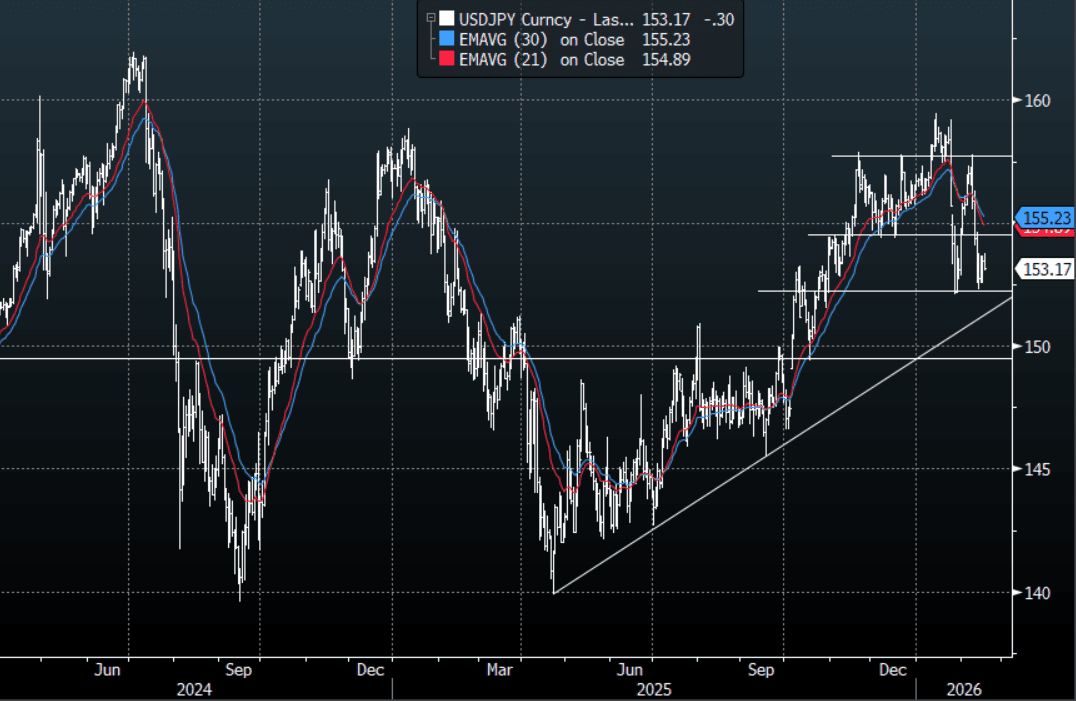

JPY: USD/JPY-Rejects The 154.00 Area Again, As Cross-Yen Reacts To Lower Risk

The USD/JPY range today has been 153.03-153.76 in the Asia-Pac session, it is currently trading around 153.15, -0.20%. USD/JPY stalled again toward 154.00 and then turned very easily lower as risk traded under pressure during our session and cross-Yen in particular is looking vulnerable. This price action does look messy for those leveraged Yen shorts but I still believe dips back toward the 149-152 will probably provide solid support initially should we see it, until then it looks like we chop around albeit with a heavy tone. On the day, the first resistance is back towards 153.75-154.25 and then the 155.00-156.00 area as the market pares back its overextended USD longs and looks for another base to form from which to potentially move higher again.

- MNI Analysis: 'Gaps in Japanese Fiscal' suggest fiscal pressure remains. Financing the JPY5trn food consumption tax suspension with proceeds from the FX special account would likely open up gaps in the general budget.

- This leaves the Japanese finance ministry with three options: Plug the gap through increasing the efficiency of the tax base and expenditure, net liquidation of parts of the FX special account, or higher JGB issuance through the backdoor.

- “The BOJ is likely to hike its key rate in April, former board member Seiji Adachi said, after it assesses a slew of data due that month.” - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 151.00($986m), 156.00($1.87b). Upcoming Close Strikes : 153.00($2.73b Feb 19), 155.00($1.43b Feb 19),158.00($1.21b Feb 20) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 142 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

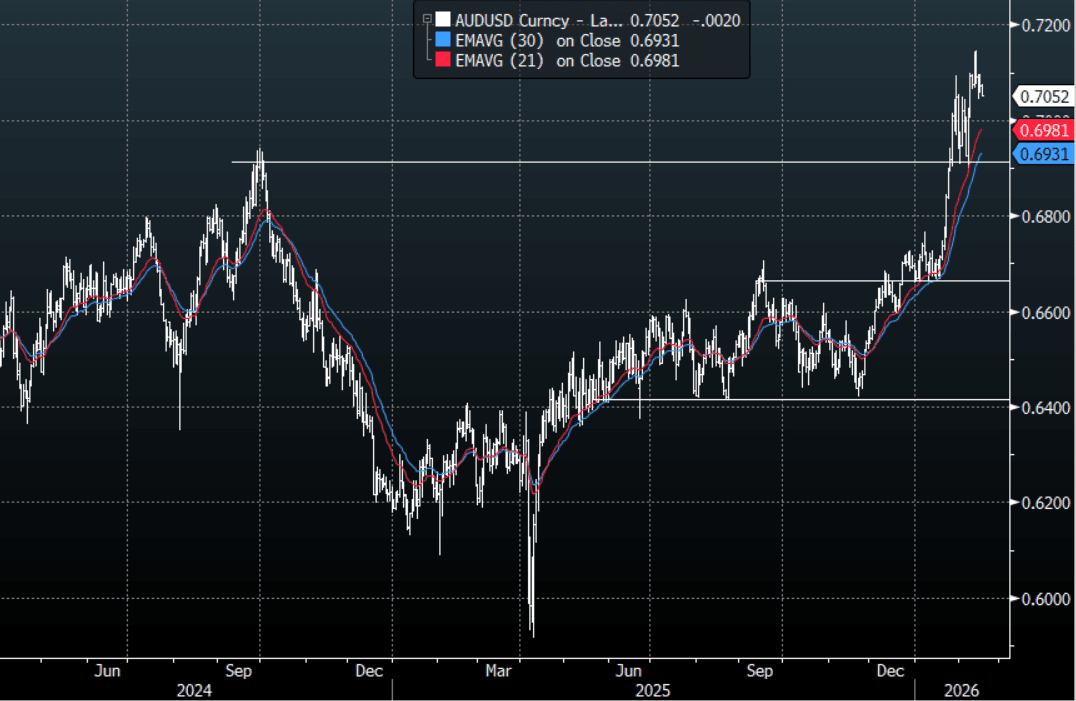

AUD/USD - Drifts Lower As Risk Starts Under Pressure Ahead Of US Open

The AUD/USD has had a range today of 0.7046 - 0.7076 in the Asia- Pac session, it is currently trading around 0.7055, -0.25%. The AUD drifted lower and traded with a heavy tone today as US futures opened under pressure and continued to move lower. Tonight's US session will be closely watched for any signs of the pullback that started last week building into something more serious. CFTC data shows leveraged funds continued to add to their AUD longs as further hikes are potentially priced in. On the day, the first support is again back toward 0.7020-0.7050, a break below here could signal a deeper pullback as the 0.7100-0.7200 area continues to cap the move higher. How risk holds up when the US returns tonight will be a key factor as to whether the bulls can muster another challenge to this resistance.

- MNI AU - RBA Mins Show Data Dependency, But Likely High Bar Not To Act Again: The RBA minutes from the Feb policy meeting noted re the inflation outlook: "the central projection for inflation had been revised materially higher, remaining above target throughout 2026 and only returning close to the midpoint of the target range around mid-2028 (on the assumption that the cash rate follows the market path)." This points to a fairly high bar, or meaningful downside inflation surprises in Q1, for the RBA not to act further. Still, the concluding paragraphs from the minutes show the RBA is not on a predetermined rate path and will continue to assess the incoming data.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.7025(AUD429m). Upcoming Close Strikes : 0.6980(AUD694m Feb 18 ) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 67 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

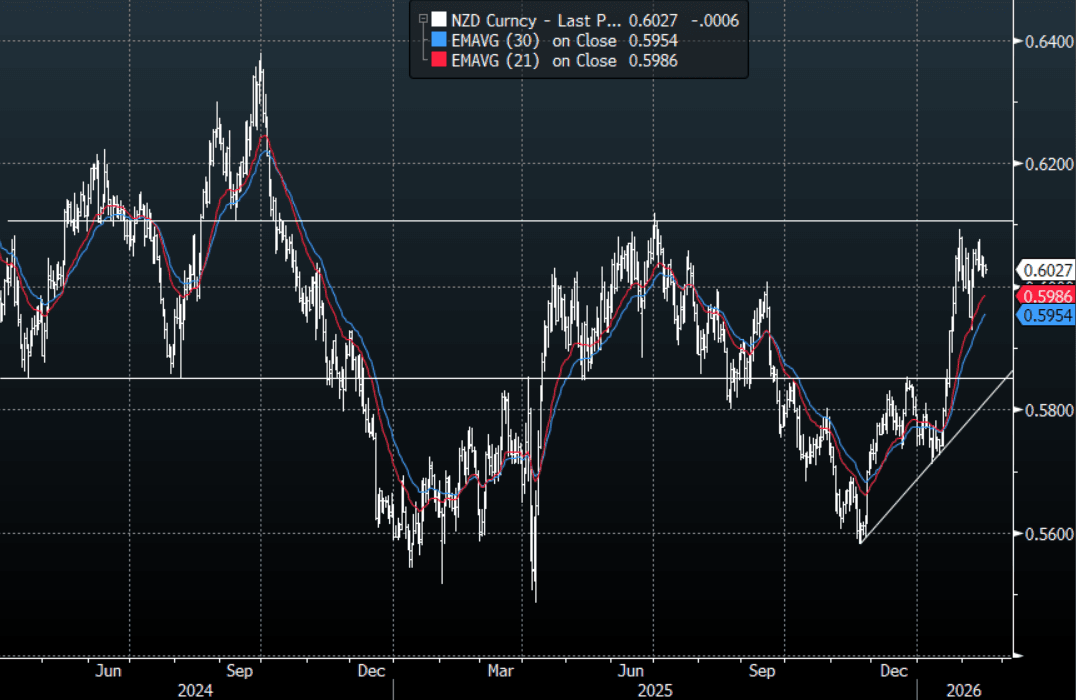

NZD/USD - Drifts Lower, But Still Holds Above 0.6000

The NZD/USD had a range today of 0.6019-0.6035 in the Asia-Pac session, it is currently trading around 0.6025, -0.10%. The NZD drifted lower and traded with a heavy tone today as US futures opened under pressure and continued to move lower. Tonight's US session will be closely watched for any signs of the pullback that started last week building into something more serious. On the day, the first support remains in the 0.5985-0.6015 area; a break below here could signal a deeper pullback toward 0.5900. For now the 0.6100 area continues to cap but the bulls will be hoping for risk to firm up tonight to have another go.

- MNI RBNZ Preview-Feb 2026: On Hold, Hike Timing Key Focus: At tomorrow's RBNZ meeting the central bank is widely expected to keep rates on hold. The Bloomberg survey of sell-side economists shows all 22 economists see the policy rate being held at 2.25%. Our strong bias is also for no change tomorrow. If realized, this will leave the focus firmly on the outlook, particularly on the RBNZ's new OCR path. The other focus point will be gauging new RBNZ Governor Breman's tone, as this will be her first rate setting meeting in charge.

- The RBNZ will also likely be cautious around sounding too hawkish around the outlook, which the market will likely judge via the implied OCR outlook path. We would be surprised if the OCR path is more hawkish than current market pricing, which implies a policy rate near 2.65% by year's end (versus the current rate of 2.25%).

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5700(NZD400m Feb18 ), 0.5860(NZD420m Feb 19), 0.6000(NZD308m Feb 19) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 50 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Post Election Rally Fades as AI Values Questioned in Japan

With much of Asia closed due to the Lunar New Year, it was left to the NIKKEI to set the tone for regional equities today. The NIKKEI reached a new all time high last Tuesday on post election hopes, but has declined for a fourth consecutive session as the "post-election euphoria" began to fade. BOJ Governor Ueda indicated no new specific fiscal or monetary signals following a meeting with the PM, maintaining a cautious stance on further rate hikes. This left sentiment mixed as preliminary Q4 GDP figures released yesterday missed median forecasts on weak capital spending. AI / tech darling Softbank is down heavily today by over 6% over growing concerns as to the real value of AI-driven industry disruptions. Profit taking is a major play here with the NIKKEI up 14% YTD prior to the last four days. Despite the losses, it remains up over 10% for the year.

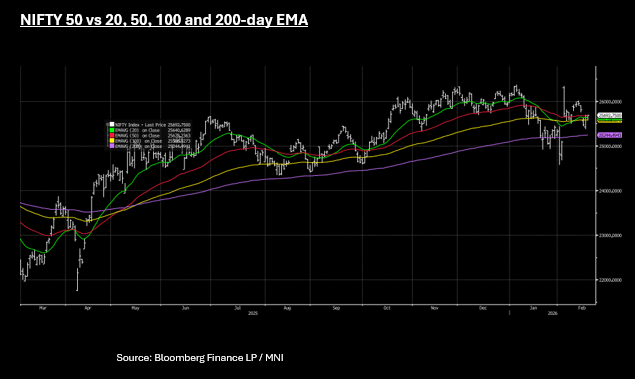

The NIFTY 50 has had a quiet opening Tuesday, as it edges above a key technical. Following strong gains yesterday, the NIFTY 50 has opened marginally higher at 25,693 as it tries to consolidate above the 50-day EMA of 25,678. The short-term (20-day), medium-term (50-day), and long-term (100-day) price averages have converged for the NIFTY suggesting that there is currently no consensus between short-term and long-term investors, leading to narrow ranges.

In Australia, the ASX delivered modest gains of +0.25% as mining giant BHP reported a 28% jump in half-year profit and retailer JB HiFi reported a 24% dividend hike.

COMMODITIES: Oil Up on Military Moves, Gold Holds Below $5,000

- News that Iran's Revolutionary Guard began naval drills near the Strait of Hormuz, a critical transit point for 20% of global have given oil prices a further boost ahead of the planned US Iran meeting Tuesday.

- Despite the longer term structural downtrend for oil on supply concerns, the near term price action is underpinned by geopolitical concerns. Prices are sensitive to negative headlines from the talks, ignoring the longer term trends. Should positive signals come out of the talks early, the geopolitical premium priced in since the early January lows, could unwind quickly.

- WTI is up +1.05% in the Asia trading day on thin markets. Some futures contracts are seeing the lowest daily turnover for the year given US and Canada out and much of Asia closed for Lunar New Year.

- WTI has traded in a tight range of $62.49 - $63.87, currently at US$63.57 bbl.

- Brent has traded lower throughout the Asia trading day, down -0.36% at US$68.40 bbl.

- Gold is lower again Tuesday also, losing ground by -0.6% to US$4,958.83

- The price action over the last week has been quite balanced, keeping the precious metal in tight ranges.

- The bull case for gold in the short term hinges on the US Iran talks in Geneva Tuesday. If negotiations stall and the US pivots back toward military action, this could send gold higher.

- The bearish case is more technical. Gold has repeatedly failed to hold gains above $5,000. At current levels, a bearish outlook could see the Feb 02 low of $4,402 eyed.

INDIA: IGBs in Tug-of-War: Global Leads Versus Domestic Supply

- India’s 10-year GB February peak was 6.76% and taking its lead from UST trends has moved lower to 6.66%

- The expected heavy slate of state bond issuance is keeping investors cautious.

- For the rest of February, apart from the regular bill issuance, the RBI will auction INR330bn in 2029, 2033 and 2055 maturities. Indian states are set to raise over INR 400 billion, above the scheduled amount, reinforcing concerns over an already crowded supply pipeline into the fiscal year-end.

- Since the Reserve Bank of India held rates steady on Feb 6 and refrained from announcing any fresh liquidity support, investors have turned more cautious.

- While the policy pause was widely expected, investors had anticipated measures to ease liquidity conditions or absorb rising issuance, but no further policy was announced.

- This comes as swaps move to price in rate hikes by year end.

- Our swaps model has +59bps of hikes priced in, with the first full rate hike in August. Probabilities for hikes in the coming 3 months are near 70% suggesting that the market has turned quickly post the end of the cutting cycle.

- FDI flows have returned and remain supportive but pre-emptive measures may be required from the RBI to help absorb expected issuance.

- The risks now are for a turn in the current down trend for USTs in the face of a strong issuance schedule.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 17/02/2026 | 0700/0700 | *** | Labour Market - AWE & Unemployment | |

| 17/02/2026 | 0700/0700 | *** | Labour Market - Payrolls & Claimants | |

| 17/02/2026 | 0700/0700 | *** | Labour Market - Payrolls & Claimants | |

| 17/02/2026 | 0700/0700 | *** | Labour Market - AWE & Unemployment | |

| 17/02/2026 | 0700/0800 | *** | Germany CPI (f) | |

| 17/02/2026 | 0700/0800 | *** | Germany CPI (f) | |

| 17/02/2026 | 0900/1000 | Foreign Trade | ||

| 17/02/2026 | 1000/1100 | *** | ZEW Current Expectations Index | |

| 17/02/2026 | - | ECB de Guindos at ECOFIN Meeting | ||

| 17/02/2026 | 1330/0830 | * | International Canadian Transaction in Securities | |

| 17/02/2026 | 1330/0830 | ** | Wholesale Trade | |

| 17/02/2026 | 1330/0830 | ** | Empire State Manufacturing Survey | |

| 17/02/2026 | 1330/0830 | *** | CPI | |

| 17/02/2026 | 1500/1000 | ** | NAHB Home Builder Index | |

| 17/02/2026 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 17/02/2026 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 17/02/2026 | 1745/1245 | Fed Governor Michael Barr | ||

| 17/02/2026 | 1800/1300 | ** | US Treasury Auction Result for 52 Week Bill | |

| 17/02/2026 | 1930/1430 | San Francisco Fed's Mary Daly | ||

| 18/02/2026 | - | Reserve Bank of New Zealand Meeting | ||

| 18/02/2026 | 0001/0001 | * | Brightmine pay deals for whole economy | |

| 18/02/2026 | 0030/1130 | *** | Quarterly wage price index | |

| 18/02/2026 | 0100/1400 | *** | RBNZ official cash rate decision | |

| 18/02/2026 | 0700/0700 | *** | Consumer Inflation Report (1dp) | |

| 18/02/2026 | 0700/0700 | *** | Consumer Inflation Report (2dp) | |

| 18/02/2026 | 0700/0700 | *** | Producer Prices | |

| 18/02/2026 | 0745/0845 | *** | HICP (f) | |

| 18/02/2026 | 0900/1000 | ECB Cipollone at ABI's Executive Committee Meeting | ||

| 18/02/2026 | 1000/0500 | * | CREA Existing Home Sales | |

| 18/02/2026 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 18/02/2026 | 1330/0830 | *** | Housing Starts | |

| 18/02/2026 | 1330/0830 | *** | Housing Starts | |

| 18/02/2026 | 1330/0830 | ** | Durable Goods New Orders | |

| 18/02/2026 | 1330/0830 | ** | Durable Goods New Orders | |

| 18/02/2026 | 1355/0855 | ** | Redbook Retail Sales Index |