MNI EUROPEAN MARKETS ANALYSIS: Fed In Focus Later

- Markets haven't shifted much so far today, with Middle East developments still in focus. Oil prices are holding Tuesday gains but sub recent highs. The USD has softened. US yields are little changed.

- China is looking to open up more and increase the role of CNY internationally. Japan data saw exports dip, but in line with market forecasts.

- The Fed is widely expected to leave rates unchanged but the dot plot will be monitored closely (see MNI Fed Preview). Inflation and jobs data have yet to show an impact from tariffs but some activity/survey data have slowed. The Fed is likely to want more time to evaluate the impact and now oil prices are up over 20% this month, it will also monitor its impact on inflation if sustained.

- There are also a number of ECB speakers including de Guindos, Elderson, Lane, Machado and Donnery and BoC’s Macklem appears. In terms of data, US May housing starts/permits, jobless claims, euro area May CPI and UK May CPI are released.

MARKETS

US TSYS: Asia Wrap - Quiet Session

The TYU5 range has been 110-23+ to 110.30 during the Asia-Pacific session. It last changed hands at 110-25, down 0-02 from the previous close.

- The US 2-year yield is unchanged; it is trading around 3.95%.

- The US 10-year yield edged higher, it is trading around 4.40%, up 0.01 from its close.

- MNI FED: FOMC Meeting Expectations: Patience Mostly Seen In New Projections. We expect that the June meeting communications will reflect an increasingly patient attitude since May and certainly since March’s projections

- (Bloomberg) -- “The report on possible easing of the US bank capital rule has so far seen muted market reaction in part because it falls short of expectations, according to National Australia Bank. “A general reduction in capital requirements is a lesser deal than a Treasury exemption,” says Ken Crompton, head of rates strategy at the Australian bank. The general lowering of the ratio is still theoretically supportive for Treasuries’ demand, but not as much as an exemption would be, says Crompton.”

- The 10-year yield bounced strongly off its 4.30/35% support, this area needs to hold if yields are to move higher. The range looks to be 4.30% - 4.60% for now a break either side would provide a clearer direction. Lots for the market to digest as things heat up in the middle east and we approach the FOMC.

- Data/Events: MBA Mortgage Applications, Housing starts, Initial Jobless Claims, FOMC

JGBS: Cash Bonds Mixed Ahead Of FOMC, Twist-Steepener

JGB futures are holding stronger, +24 compared to settlement levels, but sitting near the middle of today’s range.

- The primary focus of the BoJ decision was the pace of quantitative tightening (QT) beyond the near term. From the second quarter of 2026 through the first quarter of 2027, it will slow that pace to ¥200 billion per quarter. Overall, the BoJ signalled a gradual, data-dependent approach to policy normalisation, balancing market stability, inflation developments, and global uncertainties as it proceeds with cautious tapering into 2026 and beyond. (See MNI BoJ Review here)

- Japanese politician Shigeru Ishiba said he had frank discussions with former U.S. President Donald Trump on tariffs and aims to work toward a mutually beneficial trade deal. He emphasised that tariffs, particularly on autos, would significantly impact companies and stressed that Japan must not compromise its national interests to secure a deal. (BBG)

- The cash JGB curve has twist-steepened, with yields 2bps lower to 1bp higher. The benchmark 10-year yield is 0.3bps lower at 1.462%.

- The swaps curve has bear-steepened, with rates flat to 3bps higher.

- Tomorrow, the local calendar will see Weekly International Investment Flow and Tokyo Condominiums for Sale data alongside 5-year supply.

BOJ: MNI BoJ Review – June 2025: QT Taper Mildly More Dovish

EXECUTIVE SUMMARY

- The BoJ decided to keep its policy rate unchanged at 0.50%, a move fully expected by markets and consensus economists. The decision was made by a unanimous 9-0 vote from the Monetary Policy Committee (MPC).

- The primary focus of the meeting was the pace of quantitative tightening (QT) beyond the near term. From the second quarter of 2026 through the first quarter of 2027, it will slow that pace to ¥200 billion per quarter, a decision backed by an 8-1 vote.

- The BoJ’s policy statement maintained its existing economic and inflation outlook, aside from technical changes to incorporate recent higher inflation prints.

- Importantly, Ueda stated that the BoJ may consider raising interest rates without needing to see clear-cut new signs of rising inflation, should the economic outlook and forecast trajectory warrant such action.

- Overall, the BoJ continues to signal a gradual, data-dependent approach to policy normalisation, balancing market stability, inflation developments, and global uncertainties as it proceeds with cautious tapering into 2026 and beyond.

- Full review here

JAPAN DATA: Exports Dip Y/Y, Trade Surplus With US Narrows

Japan's May trade data was close to expectations, with export growth at -1.7%y/y, versus -3.7% forecast. The April outcome was +2.0%. On the import side, we were -7.7%y/y, against a -5.9% forecast (-2.2% was recorded for April). The trade deficit was -¥637.6bn, close to forecasts but wider than the -¥115.6bn print in April. In seasonally adjusted terms the trade position was -¥305.5bn, close to forecasts and the April outcome.

- Exports to the US fell by 11.1% y/y and were down to China by 8.8%, but up 4.9% to the EU. In volume terms exports fell 1.4%y/y to the US, and were down 7.9%y/y to China.

- The trade surplus with the US continued to narrow, now at ¥451.7bn from ¥1012.01bn at the end of last year.

- The faltering export growth backdrop for Japan is in line with other parts of the region (ex Taiwan) that have seen slowing growth in the wake of higher US tariffs. Still, the US side is likely to take comfort from the declining trade surplus. Car exports to the US fell 24.7% in May Bloomberg notes.

- The terms of trade have taken a hit in terms of the recent oil price/energy price rise (the Citi proxy is at multi month lows). If sustained this could weigh on Japan's trade position.

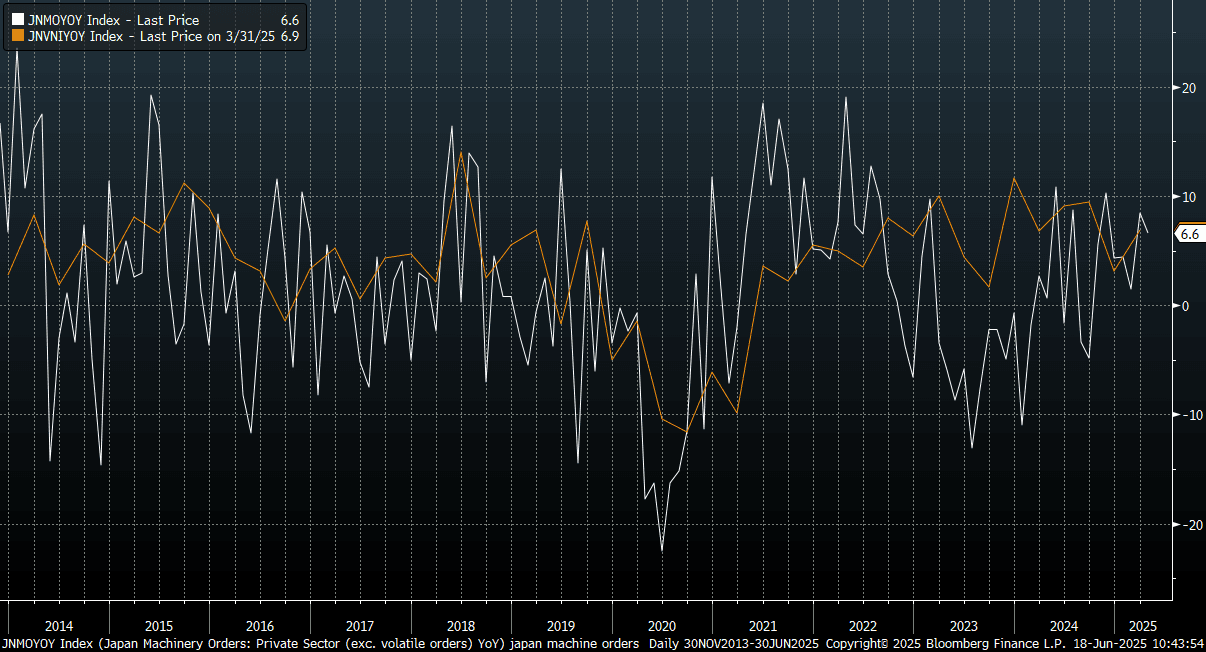

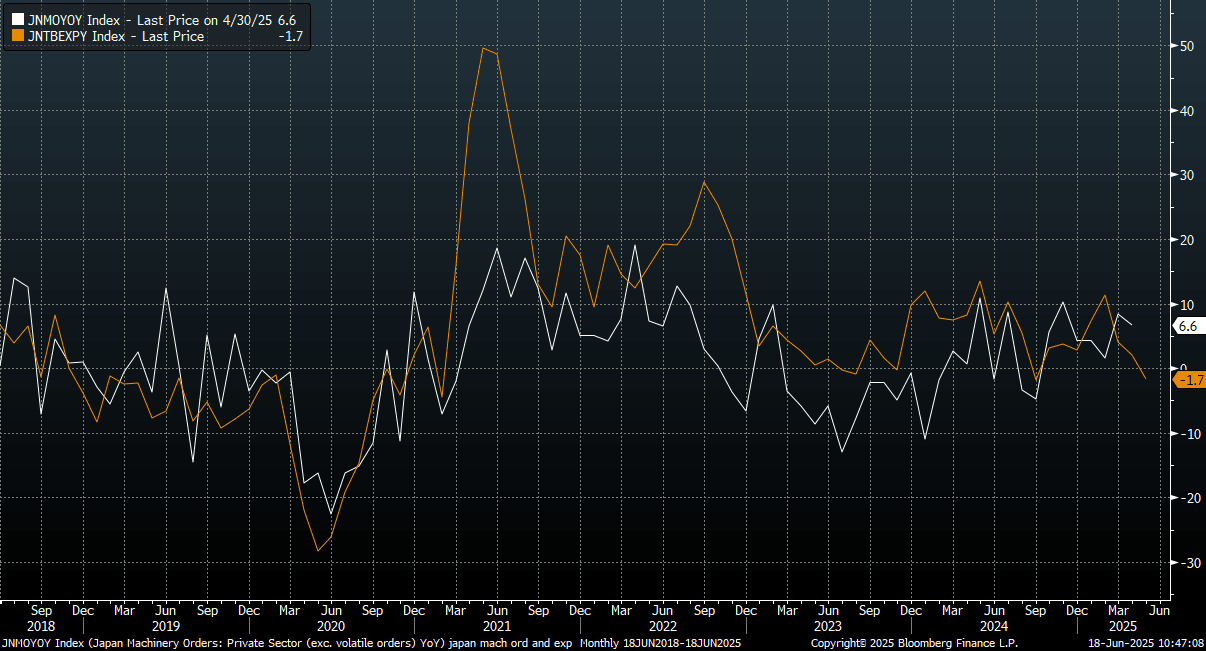

JAPAN DATA: Core Machine Orders Dip In April, Weaker Exports May Weigh

Japan April core machine orders fell sharply, but in line with market projections. We were down -9.1%m/m (-9.5% forecast and following a 13.0% gain in March). In y/y terms, we were slightly better than forecasts at +6.6% (+4.2% was projected, while 8.4% was the March outcome).

- The chart below plots core machine orders y/y (the white line on the chart) against a Japan Capex (ex software), which is also in y/y terms. It's still painting a fairly resilient backdrop in the earlier stages of Q2.

- Still, this comes ahead of trade headlines, with earlier data showing faltering export growth. The second chart below plots the machine orders against export growth (y/y), which is the orange line on the chart.

Fig 1: Japan Core Machine Orders & Capex (Y/Y)

Source: Bloomberg Finance L.P./MNI

Fig 2: Japan Core Machine Orders & Exports (Y/Y)

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: Subdued Session Ahead Of FOMC Announcement

ACGBs (YM +1.0 & XM +1.0) sit marginally stronger on a subdued pre-FOMC session.

- Cash US tsys are slightly cheaper ahead of today's FOMC Decision including a Summary of Economic Projections (Dots). The June FOMC meeting communications should reflect an increasingly patient attitude from May and certainly since March's projections.

- Cash ACGBs are 1bp richer with the AU-US 10-year yield differential at -16bps.

- The bills strip little changed with pricing flat to +2.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut in July is given a 83% probability, with a cumulative 76bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- May jobs data are released tomorrow and Bloomberg consensus is expecting labour market tightness to continue, one of the reasons the RBA remains cautious regarding the monetary policy outlook.

- Consensus is forecasting a 21.2k increase in new jobs, close to the 3-month average of 23k, with the unemployment rate steady at 4.1%. In May the RBA projected 4.2% in Q2 and employment growth of 2.1% y/y. New jobs rose a stronger-than-expected 89k and 2.7% y/y in April.

- The AOFM plans to sell A$800mn of the 1.00% 21 December 2030 bond on Friday.

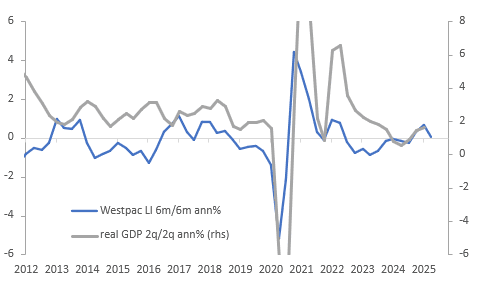

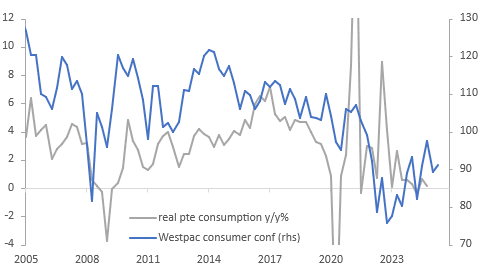

AUSTRALIA DATA: Westpac Lead Index Signals Slower Growth

The Westpac lead indicator fell 0.06% m/m in May after -0.01% but this resulted in the 6-month annualised rate falling to -0.08%, the weakest since September but importantly signalling that growth could ease to below trend over the second half of the year. The measure peaked in February and has been trending lower since as global uncertainty has risen and some domestic factors were also soft but Westpac believes these local “drags” are “temporary”.

- A disappointing recovery is likely to add to the argument for the RBA to ease policy further, especially if underlying inflation moves towards the 2.5% band mid-point. Westpac continues to expect the Board to be cautious given labour market tightness (May data print June 19) and be on hold on July 8 but then cut 25bp on August 12.

- The domestic economy appears to be struggling due to the end of public spending on some big projects but the private sector remains sluggish. Global uncertainty is also delaying investment decisions.

- A large share of the deterioration in the 6-month rate has been due to the stalling in the recovery of residential building approvals and the drop in hours worked, which hasn’t been helped by higher consumer inflation and unemployment expectations. Commodity and equity prices have also been a drag but to a lesser degree. However, US IP has added to the lead index.

Australia Westpac LI vs GDP growth

Source: MNI - Market News/LSEG

BONDS: NZGBS: Closed Little Changed, Subdued Session, FOMC Due, Q1 GDP Tomorrow

NZGBs closed little changed after a subdued session.

- Cash US tsys are slightly cheaper ahead of today’s FOMC Decision including a Summary of Economic Projections (Dots). The June FOMC meeting communications should reflect an increasingly patient attitude since May and certainly since March’s projections.

- The NZGB 10-year underperformed its $-bloc counterparts, with the NZ-US and NZ-AU yield differentials widening 2-3bps.

- Westpac Q2 consumer confidence picked up to 91.2 from 89.2 in Q1.

- Swap rates closed unchanged.

- RBNZ dated OIS pricing closed little changed across meetings. 4bps of easing is priced for July, with a cumulative 26bps by November 2025.

- Tomorrow, the local calendar will see Q1 GDP. Bloomberg consensus is forecasting the production-based measure to rise 0.7% q/q again, bringing the annual rate to -0.8%, higher than forecast by the RBNZ in May. The central bank is expecting a rise of 0.4% q/q.

- With rates now in the “neutral zone” and RBNZ Governor Hawkesby saying the MPC doesn’t have a bias, and especially if GDP prints stronger than it expects, the RBNZ may be on hold on July 9.

- Tomorrow, the NZ Treasury plans to sell NZ$225mn of the 3.00% Apr-29 bond, NZ$175mn of the 2.75% Apr-37 bond and NZ$50mn of the 2.75% May-51 bond.

NEW ZEALAND: Westpac Consumer Confidence Signals Spending Outlook Remains Soft

Westpac Q2 consumer confidence picked up to 91.2 from 89.2 in Q1, while the number of pessimists declined they continue to outnumber optimists with the breakeven-index 100. Sentiment also remains below Q4 2024’s 97.5. Households remain cautious about the outlook despite 225bp of RBNZ easing given heightened global uncertainty, an unbalanced recovery and a soft labour market.

- While most regions saw a rise in consumer confidence, only one posted a reading above 100.

- Present conditions remained weak at 81.7 up from 80.2 with the assessment of current financial conditions falling to -27 from -24.1. Westpac notes that finances are being impacted by rises in living costs. Q1 CPI inflation rose 2.5% y/y up from 2.2% while May data showed food and electricity inflation rising further.

- The outlook is more positive with expected conditions rising 2.3 points to 97.5, still below the 10-year average, and the expected financial situation improving 2.6 points to 7.4.

- It is still not a “good time to buy” a major item but it improved 6.1 points to -9.5 but the 10-year average is at +4.5. Recent consumption data have been lacklustre and show that households remain cautious. The Westpac survey found that a net 31% have reduced discretionary spending.

NZ consumer outlook

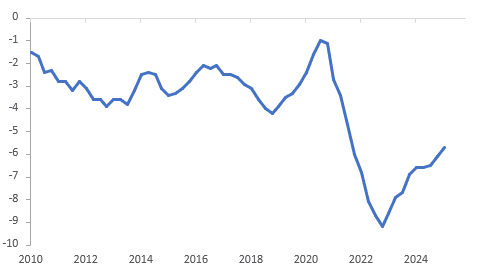

NEW ZEALAND: Q1 Current Account Narrows On Strong Goods Exports

The Q1 non-seasonally adjusted current account deficit narrowed substantially to $2.32bn from a downwardly-revised $6.80bn but seasonally adjusted it was similar to Q4 at $5.55bn. This brought it to 5.7% of GDP down from 6.1%, the lowest since Q3 2021 and 3.5pp less than the Q4 2022 peak. The trade deficit narrowed to $1.22bn from $1.63bn, the lowest since Covid-impacted Q2 2021, due to a strong pickup in goods exports. Robust shipments in Q1 are likely to support GDP growth when it is released on Thursday.

NZ current account % GDP

Source: MNI - Market News/LSEG

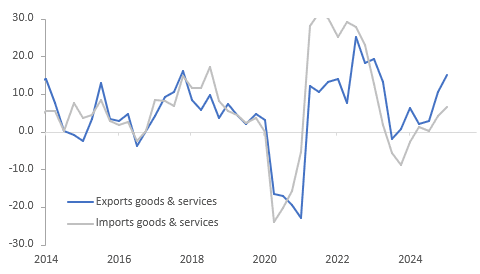

- Goods exports rose 11.9% q/q in Q1 to be up 18% y/y driven by agricultural products and higher prices for dairy and meat. Imports rose 5.5% q/q to be up 6% y/y driven by intermediate items including processed fuels. Durable consumer goods also saw a robust rise.

- The services balance returned to a deficit in Q1 after a small surplus in Q4, as exports fell 5.9% q/q due to lower visitor expenditure while imports rose 2.4% q/q driven by transport services.

- The net international investment liability position narrowed to $212.2bn in Q1 from $213.6bn, as the value of assets fell by less than liabilities due to global market uncertainty.

NZ goods & services exports vs imports y/y%

Source: MNI - Market News/LSEG

FOREX: Asia FX Wrap - The USD Drifts Lower Heading Into FOMC

The BBDXY has had a range of 1207.92 - 1210.11 in the Asia-Pac session, it is currently trading around 1208. “Xi Jinping said there are no winners in tariff and trade wars, and pledged 1.5 billion yuan ($209 million) in aid this year to central Asian nations as Beijing seeks closer ties with the region. He also said China is ready to play a role in restoring Mideast peace.”(BBG). “CHINA FX REGULATOR: FX MARKET RESILIENCE WILL CONTINUE, ABILITY TO COUNTER FX MARKET VOLATILITY HAS IMPROVED, WILL KEEP YUAN BASICALLY STABLE AT REASONABLE AND BALANCED LEVELS" RTRS”

- EUR/USD - Asian range 1.1475 - 1.1506, Asia is currently trading 1.1505. EUR has rejected the move above 1.1600 but dips should continue to find demand, first support back towards the 1.1400 area then 1.1100/1200. Price action does not look good short-term with a potential false break above 1.1500/1.1600.

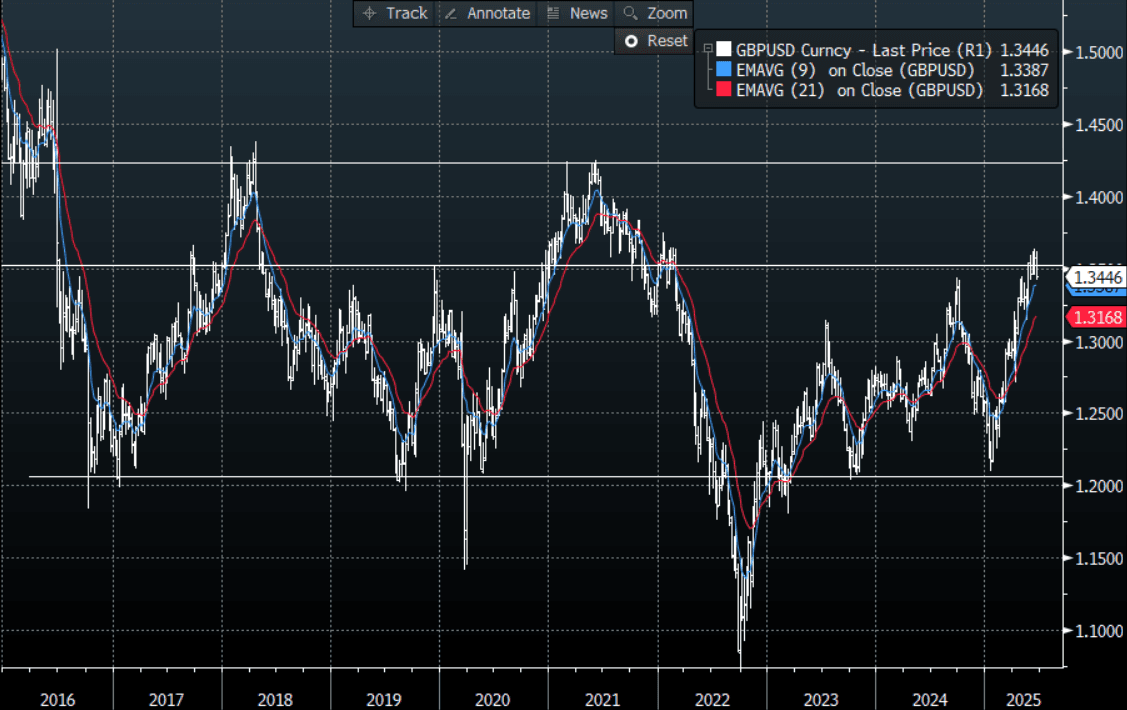

- GBP/USD - Asian range 1.3422 - 1.3447, Asia is currently dealing around 1.3445. The GBP looks to have failed in its attempts to break above the 1.35/36 Weekly pivot. First support is seen back towards 1.3400 a move back below here and we could see a deeper correction unfold.

- USD/CNH - Asian range 7.1866 - 7.1924, the USD/CNY fix printed 7.1761. Asia is currently dealing around 7.1890. Sellers should be around on bounces while price holds below the 7.2500 area and the PBOC manages the fix lower.

- Cross asset : SPX +0.07%, Gold $3396, US 10-Year 4.40%, BBDXY 1207, Crude oil $75.0

Data/Events : EZ Current Account, Italy Current Account, EZ CPI

Fig 1: GBP/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

JPY: Asia Wrap - USD/JPY In The Middle Of Its Recent Range, Can FOMC move it ?

The Asia-Pac USD/JPY range has been 144.93 - 145.44, Asia is currently trading around 144.93. USD/JPY has drifted lower in a muted Asian session, -0.25%. With the USD bouncing across the board as risk digests the potential of the US entering the fray in the middle east, the long JPY positions continue to be challenged. You would normally expect the JPY to outperform in this scenario but the outsized move in oil and a market that is already positioned very long is providing headwinds to the trade.

- Japan Data - Exports Dip Y/Y, Trade Surplus With US Narrows : Japan's May trade data was close to expectations, with export growth at -1.7%y/y, versus -3.7% forecast. The April outcome was +2.0%. On the import side, we were -7.7%y/y, against a -5.9% forecast (-2.2% was recorded for April). The trade deficit was -637.6bn, close to forecasts but wider than the -115.6bn print in April.

- "ISHIBA: HAD FRANK DISCUSSIONS ON TARIFFS WITH TRUMP, WILL WORK WITH US TOWARD A WIN-WIN DEAL" - BBG

- "ISHIBA: TARIFFS WILL HAVE BIG IMPACT ON COMPANIES, NAMELY AUTOS, SAYS JAPAN MUST NOT SACRIFICE NATIONAL INTEREST FOR DEAL" - BBG

- “ISHIBA: WAGE INCREASE MORE IMPORTANT THAN CUTTING SALES TAX, IMPACT OF CASH HANDOUT IS MORE IMMEDIATE THAN TAX CUT" - BBG

- USD/JPY found decent demand yesterday every time it had a look towards the 144.50 area yesterday. This price action stands out considering the risk backdrop and could hint at a market that is already very long JPY.

- Price is back in the middle of its recent 142.00 - 147.00 range and will need a break either side of that to get a clearer direction. Can FOMC be that catalyst ?

- The market is clearly looking for a move lower in USD/JPY but with positioning quite large now we have seen the risk of pullbacks increase. A break above 147.00 would be needed to challenge the conviction of any shorts.

- Options : Close significant option expiries for NY cut, based on DTCC data: 144.00($725m). Upcoming Close Strikes : 146.00($1.92b June 20), 143.00($925m June 20)

Fig 1 : USD/JPY Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

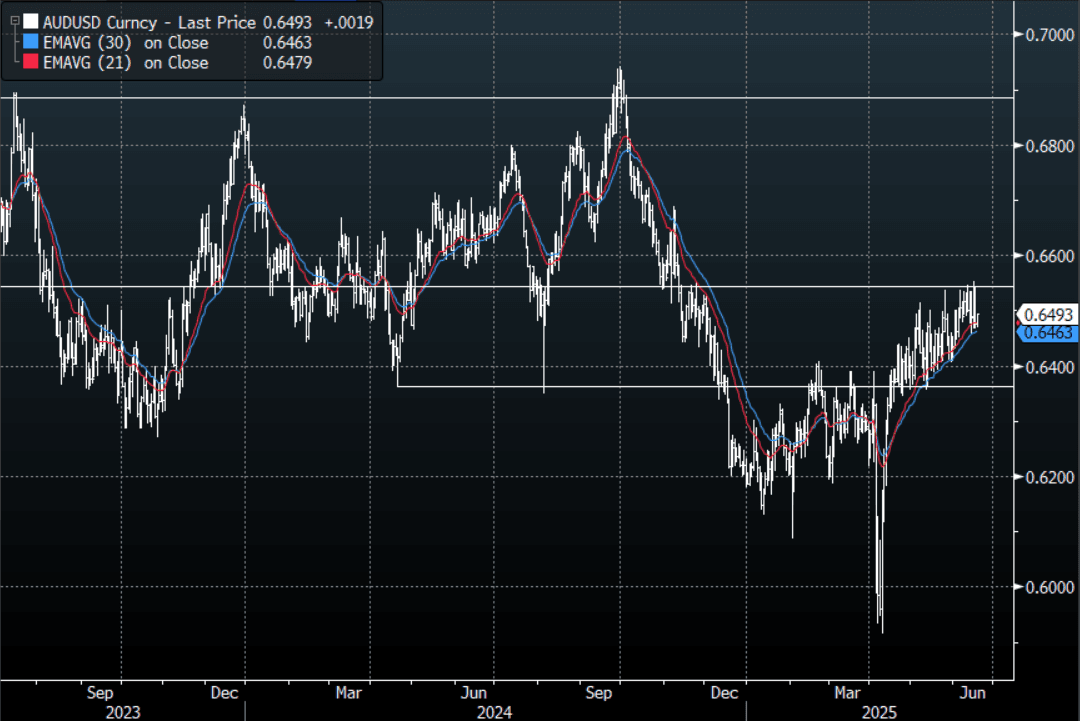

AUD: Asia Wrap - Drifts Higher

The AUD/USD has had a range of 0.6469 - 0.6494 in the Asia- Pac session, it is currently trading around 0.6490. The AUD has drifted higher in a quiet Asian session +0.26%.

- AU Data - Westpac Lead Index Signals Slower Growth. The Westpac lead indicator fell 0.06% m/m in May after -0.01% but this resulted in the 6-month annualised rate falling to -0.08%, the weakest since September but importantly signalling that growth could ease to below trend over the second half of the year.

- (Bloomberg) -- “China is willing to enhance the level of trade and investment facilitation with Australia, Chinese Commerce Minister Wang Wentao says. China is willing to work with Australia to adhere to cooperation and openness, and not to engage in closed-door confrontation, Wang says.”

- The AUD failed miserably again to break above the 0.6550 area, with momentum stalling and the USD starting to bounce the probability of it moving to the bottom end of its range increases.

- Price remains in the 0.6350 - 0.6550 range for now, a sustained break above 0.6550/0.6600 is needed for the move higher to accelerate.

- Buyers should continue to be around on dips while the support in the AUD/USD holds, a close back below 0.6350 is needed to challenge the newly formed uptrend.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6400(AUD321m). Upcoming Close Strikes : 0.6600(AUD 1.1b June 19)

AUD/JPY - Today's range 94.02 - 94.30, it is trading currently around 94.15.Choppy price action as the pair establishes a range between 92.00 - 96.00. A break back below 91.50/92.00 is needed to see the move lower regain momentum and the focus turn back to the year's lows again.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

NZD: Asia Wrap - Holds Above 0.6000, For Now ?

The NZD/USD had a range of 0.6010 - 0.6034 in the Asia-Pac session, going into the London open trading around 0.6025. The NZD has drifted higher in a quiet Asian session, still holding above 0.6000.

- NZ Data - Westpac Consumer Confidence Signals Spending Outlook Remains Soft. Westpac Q2 consumer confidence picked up to 91.2 from 89.2 in Q1, while the number of pessimists declined they continue to outnumber optimists with the breakeven-index 100. Sentiment also remains below Q4 2024’s 97.5. Households remain cautious about the outlook despite 225bp of RBNZ easing given heightened global uncertainty, an unbalanced recovery and a soft labour market.

- "NZ TREASURY CONFIDENT OF 2025 GROWTH DESPITE WEAK MAY DATA" - BBG

- The USD is finally looking like it could potentially bounce as the risk backdrop deteriorates. We have seen this before, is this time different ?

- The NZD is back to testing its support around the 0.6000 area, a break back below here and we could see a deeper pullback.

- While the support around 0.5850 holds in NZD/USD there should be buyers around on dips. A clear sustained break above 0.6050/0.6100 is needed for the pair to push higher.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5760(NZD1.16b). Upcoming Close Strikes : 0.5830(NZD300m June 23), 0.5755(NZD300m June20)

AUD/NZD range for the session has been 1.0758 - 1.0776, currently trading 1.0770. A top looks in place now just above 1.0900, the cross topped out last week towards the 1.0800/25 sell area, but the momentum lower seems to have stalled for now, with the range for June basically being captured within a 1.0750 - 1.0800 range.

Fig 1: NZD/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Hang Seng Drags Others Lower

The Hang Seng was one of the worst regional performers today, weighing heavy on other major bourses. As escalating Middle East tensions dominate this week's Federal Reserve meeting has markets sidelined to see if the FED will alter the direction for US interest rates.

The Middle East tensions are driving oil prices higher raising concerns as to the return of inflation as a catalyst for interest rates in the region.

- China's Hang Seng is down -1.15% and is down -2.75% over the last five days of trading. This dragged the CSI 300 with it, albeit marginally, down -0.07%, the Shanghai Comp was softer by -0.20% and the Shenzhen Comp down -0.36%

- The KOSPI's good run continued and is up +0.45% today and approaching a +2.00% gain over the last week.

- The FTSE Malay KLCI barely moved today and is where it started the trading day despite the BNM governor's positive comments about the economy.

- The Jakarta Composite fell -0.54%, taking back yesterday's gains.

- The FTSE Straits Times in Singapore fell -0.33% and the PSEi in the Philippines fell -0.10%

- The NIFTY 50 is up +0.20% so far today, looking to recover yesterday's losses of -0.37%

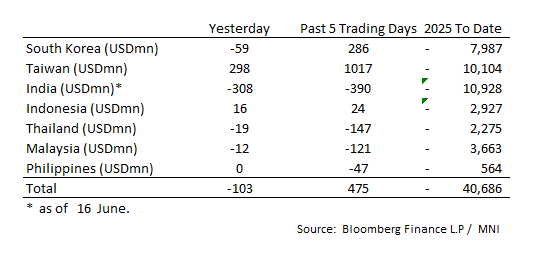

ASIA STOCKS: Outflows Continue, Taiwan the Exception

After a strong period of inflows, recent days have seen outflows beginning whilst Taiwan enjoyed a sizeable inflow yesterday.

- South Korea: Recorded outflows of -$59m yesterday, bringing the 5-day total to +$286m. 2025 to date flows are -$7,987. The 5-day average is +$57m, the 20-day average is +$169m and the 100-day average of -$80m.

- Taiwan: Had inflows of +$298m as of yesterday, with total inflows of +$1107 m over the past 5 days. YTD flows are negative at -$10,104. The 5-day average is +$203m, the 20-day average of +$74m and the 100-day average of -$95m.

- India: Had outflows of -$308m as of the 16th, with total outflows of -$390m over the past 5 days. YTD flows are negative -$10,928m. The 5-day average is -$78m, the 20-day average of -$91m and the 100-day average of -$83m.

- Indonesia: Had inflows of +$16m yesterday, with total inflows of +$24m over the prior five days. YTD flows are negative -$2,927m. The 5-day average is +$5m, the 20-day average +$8m and the 100-day average -$29m.

- Thailand: Recorded outflows of -$19m as of yesterday, with outflows totaling -$147m over the past 5 days. YTD flows are negative at -$2,275m. The 5-day average is -$29m, the 20-day average of -$26m and the 100-day average of -$21m.

- Malaysia: Recorded outflows of -$12m as of yesterday, totaling -$121m over the past 5 days. YTD flows are negative at -$3,663m. The 5-day average is -$31m, the 20-day average of -$29m and the 100-day average of -$23m.

- Philippines: Saw no flows yesterday, with net outflows of -$47m over the past 5 days. YTD flows are negative at -$564m. The 5-day average is -$10m, the 20-day average of -$17m the 100-day average of -$5m.

OIL: Crude Holds Gains As Nervously Watches Middle East Developments, Fed Later

Oil prices have held onto Tuesday’s +5% gains during today’s APAC session. Risks that an escalation in the Israel-Iran conflict impacting Middle Eastern oil exports have risen. While, Israel attacked oil and gas infrastructure, Iran’s major export facilities are so far untouched. Markets are also waiting for the Fed decision later.

- WTI is down slightly to $74.80/bbl after falling to $74.72, while Brent is flat at $76.46/bbl recovering from $76.25. Both benchmarks remain below the highs following Israel’s initial strikes. The USD index is down 0.1%.

- Israel has said that the US is helping it with defence but speculation is growing that it will become directly involved in the conflict. President Trump has demanded that Iran surrender and that his patience with Iran is “wearing thin”.

- In its June report, the IEA revised up its 2025 supply forecast by 1.8mbd to 104.9mbd while demand is expected to be 103.8mbd. It has been signalling excess supply for some time and sustained higher prices would likely boost production. US EIA inventories are released later today but industry-based data showed a sharp 10.1mn barrel drawdown last week.

- The Fed is widely expected to leave rates unchanged but the dot plot will be monitored closely (see MNI Fed Preview). Inflation and jobs data have yet to show an impact from tariffs but some activity/survey data have slowed. The Fed is likely to want more time to evaluate the impact and now oil prices are up over 20% this month, it will also monitor its impact on inflation if sustained.

- There are also a number of ECB speakers including de Guindos, Elderson, Lane, Machado and Donnery and BoC’s Macklem appears. In terms of data, US May housing starts/permits, jobless claims, euro area May CPI and UK May CPI are released.

GOLD: Bullion Monitoring Fed & Middle East Developments

Gold prices range traded on Tuesday and that trend has continued in today’s APAC session as markets await the Fed decision later. They fell to $3370.75/oz but have rebounded to $3399.0 to be up 0.3% today supported by the softer US dollar (USD BBDXY -0.1%). Treasury yields are little changed. Bullion continues to be dependent on the Middle East too with any escalation driving safe-haven flows.

- Medium-term trend signals are bullish with moving average studies in a bull mode. Initial resistance is at $3451.3, 16 June high, while support is at $3340.2, 20-day EMA.

- Prospects of the US assisting Israel in its attacks on Iran have increased. President Trump has demanded that Iran surrender but said that they won’t assassinate the Ayatollah “for now” but his patience with Iran is “wearing thin”.

- Silver is 0.4% higher at $37.267 today to be up 13% this month. The intraday high of $37.282 is also the high for June. A bull wave persists and has broken above a number of resistance levels opening $37.478, March 2012 high.

- The Fed is widely expected to leave rates unchanged but the dot plot will be monitored closely (see MNI Fed Preview). Inflation and jobs data have yet to show an impact from tariffs but some activity/survey data have slowed. The Fed is likely to want more time to evaluate the impact and now oil prices are up over 20% this month, it will also monitor its impact on inflation if sustained. A prolonged hold would likely weigh on gold prices, depending on other events.

- There are also a number of ECB speakers including de Guindos, Elderson, Lane, Machado and Donnery and BoC’s Macklem appears. In terms of data, US May housing starts/permits, jobless claims, euro area May CPI and UK May CPI are released.

MNI BSP Preview - June 2025: Back to Back for the BSP

Download Full Report Here:

We see the BSP cutting rates at the June meeting given:

- Inflation falling below target and turning negative for the month.

- GDP at the lower end of the government's target.

- Imports turning negative highlighting concerns as to the health of the consumer.

- Peso and FX Reserves have stabilized.

INDONESIA: Country Wrap: Budget Details Released

- Indonesia’s state budget deficit was 21t rupiah in end-May, equivalent to 0.09% of GDP, according to the Ministry of Finance in a briefing in Jakarta. State revenue was 995.3t rupiah, -11.4% y/y. State expenditure was 1,016.3t rupiah, -11.3% y/y. Tax revenue was 683.3t rupiah, -10.1% y/y. Custom and excise revenue 122.9t rupiah, +12.7% y/y (source BBG)

- Singapore and Indonesia have cemented a new era of bilateral relations by signing 19 major agreements across diverse sectors during a highly productive Leaders’ Retreat, marking President Prabowo Subianto’s first official state visit to Singapore since taking office. Prime Minister Lawrence Wong opened the joint press conference by emphasizing the strength of bilateral ties, stating, Singapore-Indonesia relations are in excellent shape, and we want to chart even stronger ties in this new era of cooperation. “This retreat is a platform reserved for Singapore’s “two closest neighbors, “ he said in a joint press conference on Monday, June 16, 2025, showcasing a relationship built on “comfort and trust at the highest levels”. (source Indonesia Business Post)

- The Jakarta Composite fell -0.54%, taking back yesterday's gains.

- The rupiah fell today by -0.24% to 16,328 making it one of the worst regional performers.

- Bonds were mixed with limited yield movements. 10YR 6.72%

SOUTH KOREA: Country Wrap: Extra Budget Plan Presented Thursday

- South Korean President Lee Jae Myung and Japan’s Prime Minister Shigeru Ishiba agreed to step up cooperation in their first in-person talks, in an early indication of the direction of future relations between the two countries after Lee took office. (source BBG)

- South Korea will include tax revenue adjustment and consumption vouchers for all citizens in extra budget plan which will be presented to cabinet meeting on Thursday, ruling Democratic Party’s chief policymaker Jin Sung-joon says. Additional support for low income earners will be added; extra budget plan will also have debt relief for small business owners. Size of extra budgets, including first extra budget, would be around total ~35t won, Jin tells reporters after meeting with government. (source BBG)

- The KOSPI's good run continued and is up +0.45% today and approaching a +2.00% gain over the last week.

- The Won was the best regional performer today, gaining +0.23% to 1,371.17

- Bonds saw higher yields by 1-2bps. KTB 10YR 2.87%

CHINA: Country Wrap: China To Support Foreign Participation In Finance

- China will support foreign-funded companies to participate in more pilots of financial business in the country, especially in exclusive pension insurance and commercial pensions, said Li Yunze, director of the National Administration of Financial Regulation on Wednesday. (source MNI)

- The international monetary system is evolving toward a multipolar structure where several major sovereign currencies will coexist, and the International Monetary Fund's Special Drawing Rights (SDR) could emerge as a leading international currency, People’s Bank of China Governor Pan Gongsheng said Wednesday at the 2025 Lujiazui Forum. (source MNI)

- China's Hang Seng is down -1.15% and is down -2.75% over the last five days of trading. This dragged the CSI 300 with it, albeit marginally, down -0.07%, the Shanghai Comp was softer by -0.20% and the Shenzhen Comp down -0.36%

- Yuan Reference Rate at 7.1761 Per USD; Estimate 7.2001

- Bonds remain stable in very tight ranges. CGB 10YR 1.69%

INDIA: Country Wrap: Rate Cuts Not Over

- Reserve Bank of India Governor Sanjay Malhotra’s recent comments in an interview suggest that the central bank’s interest-rate-cutting cycle is not over, according to economists from Nomura led by Sonal Varma. The RBI’s growth and inflation forecasts are likely to be undershot as the year progresses, they write. The RBI is likely to pause rate cuts in August, then resume with cuts of 25 basis points each at its policy meetings in October and December (source BBG)

- There is a general sense that India is an inward-looking economy. After all, agriculture makes up a fifth of the economy, and India is more domestic demand-driven than some export-led Asian neighbours. Having said that, we find that India has grown at its fastest pace in periods of rising integration with the world. (source India Express)

- The NIFTY 50 is up +0.20% so far today, looking to recover yesterday's losses of -0.37%

- The rupee fell today by -0.08% to 86.31

- Bonds were marginally higher in yield with the 10YR at 6.27% (+0.5bp)

ASIA FX: USD/CNH Edges Down, Lujiazui Forum In Focus, USD/KRW Upticks Faded

In North East Asia FX, USD/CNH sits down a touch, amid a flurry of headlines from the Lujiazui Forum. Spot USD/KRW upticks have been faded, while USD/TWD is holding above 29.50. USD/HKD spot remains very close to the top end of the peg band.

- USD/CNH is holding under 7.1900, marginally down on end Tuesday levels. The USD/CNY fix was set higher, but only marginally, lending some support to CNH. Most focus has been on headlines from the Lujiazui forum, where various officials have spoken.

- The PBoC Governor sees a multipolar system, where several sovereign currencies will coexist (see this link from our policy team).

- Elsewhere it was noted - China’s foreign exchange market will remain stable, with the yuan operating at a “reasonably balanced level,” said Zhu Hexin, head of the State Administration of Foreign Exchange, adding that a new round of investment quotas under the Qualified Domestic Institutional Investor (QDII) scheme will be granted to meet demand for overseas investment. (see this link from our policy team).

- For spot USD/KRW, we opened close to 1382 before finding firm selling interest. The pair was last near 1370, slightly up in won terms for the session. The 1 month NDF is back under 1370, up 0.80% in won terms versus end NY levels on Tuesday. Local equities are higher, but sub early Tuesday highs in index terms.

- USD/TWD has been very steady, last holding above 29.50, which still looks to be a support point in the near term.

- USD/HKD is unchanged, and just under 7.8500.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 18/06/2025 | 0600/0700 | *** | Consumer inflation report | |

| 18/06/2025 | 0730/0930 | *** | Riksbank Interest Rate Decison | |

| 18/06/2025 | 0730/0930 | ECB Elderson At SRB Legal Conference 2025 | ||

| 18/06/2025 | 0800/1000 | ** | EZ Current Account | |

| 18/06/2025 | 0900/1100 | *** | HICP (f) | |

| 18/06/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 18/06/2025 | 1230/0830 | *** | Housing Starts | |

| 18/06/2025 | 1230/0830 | *** | Jobless Claims | |

| 18/06/2025 | 1230/0830 | *** | Housing Starts | |

| 18/06/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 18/06/2025 | 1500/1700 | ECB Lane At Macroprudential Conference | ||

| 18/06/2025 | 1515/1115 | BOC Governor speaks in Newfoundland. | ||

| 18/06/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 18/06/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 18/06/2025 | 1600/1200 | ** | Natural Gas Stocks | |

| 18/06/2025 | 1800/1400 | *** | FOMC Statement | |

| 18/06/2025 | 1800/2000 | ECB de Guindos at Osservatorio Permanente Giovani-Editori | ||

| 18/06/2025 | 2000/1600 | ** | TICS | |

| 19/06/2025 | 2245/1045 | *** | GDP | |

| 19/06/2025 | - | NorgesBank Meeting | ||

| 19/06/2025 | - | Swiss National Bank Meeting | ||

| 19/06/2025 | 0130/1130 | *** | Labor Force Survey | |

| 19/06/2025 | 0730/0930 | *** | SNB PolicyRate | |

| 19/06/2025 | 0730/0930 | *** | SNB Interest Rate Decision | |

| 19/06/2025 | 0730/0930 | ECB's Lagarde On Economic and Financial Integration | ||

| 19/06/2025 | 0800/1000 | *** | Norges Bank Rate Decision | |

| 19/06/2025 | 0900/1100 | ** | Construction Production | |

| 19/06/2025 | 0945/1145 | ECB de Guindos On Eurozone Economic Outlook | ||

| 19/06/2025 | 1030/1230 | ECB Lagarde Keynote Speech At Economic Integration Conference | ||

| 19/06/2025 | 1100/1200 | *** | Bank Of England Interest Rate | |

| 19/06/2025 | 1100/0700 | *** | Turkey Benchmark Rate | |

| 19/06/2025 | 1100/1200 | *** | Bank Of England Interest Rate | |

| 19/06/2025 | - | ECB Cipollone At Eurogroup Meeting |