MNI EUROPEAN MARKETS ANALYSIS: Dollar & Yields Steady Ahead of CPI/FOMC Later

- US Treasury futures are little changed today, as the markets awaits US CPI and the FOMC later tonight. The USD is equally steady, outside of a modest pop higher in AUD/USD. Regional equity sentiment has been mixed.

- China CPI data for May suggested a benign domestic backdrop, with core inflation pressures ticking down a touch.

- Later the Fed is expected to hold rates steady but increase its 2024 and 2025 median rate forecast (see MNI Fed Preview). US May headline CPI is projected to be steady at 3.4% while core should ease 0.1pp to 3.5% (see MNI US Preview).

- The ECB’s Tuominen, Schnabel, Buch, de Guindos and McCaul, and BoC’s Macklem speak. UK April trade and monthly GDP print.

MARKETS

US TSYS: Tsys Futures Steady Ahead Of Key US Data Later Today

- Treasury futures are little changed today, as the markets awaits US CPI and the FOMC later tonight. TU is - 00¼ at 101-31⅛, off highs of 101-31¼, while TY is unchanged at 109-17+, off earlier highs of 109-18.

- Volumes are on the low side this morning: TU 15k, FV 30k TY 51k

- Tsys Flows: 1,500 Block likely buyer of FVU4, Large SOFR Strip buyer DV01 $1m

- Cash treasury curve is little changed this morning with the 2Y +0.4bp to 4.838%, the 10Y is -0.6bp at 4.398%, while the 2y10y is -0.998 at -44.210

- Across APAC Rates: ACGBs are 2-3bps lower, Australia's Jim Chalmers said he is cautiously confident the government can bring the economy in for a soft landing. NZGBs are unch to 2bps lower, while JGBs are 2-4bps lower.

- Looking ahead, CPI at 0830ET and FOMC policy announcement at 1400ET, Fed Chairman Powell presser at 1430ET.

JGBS: Richer Ahead Of US CPI Data & FOMC Policy Decision, BoJ Decision On Friday

JGB futures are holding richer and near session highs, +30 compared to settlement levels.

- Today's BoJ Rinban operations saw negative spreads and mostly lower offer cover ratios. At the margin, this generated some slight support for the market in the Tokyo afternoon session.

- Outside of the previously outlined PPI data, there hasn't been much in the way of domestic drivers to flag.

- Looking ahead, we anticipate that the BoJ will maintain its policy rate on June 14. Nevertheless, we expect a generally hawkish tone at the meeting, indicating the possibility of additional policy tightening in subsequent meetings, possibly as soon as July.

- The focus for the June meeting will likely be on the future pace of JGB purchases. It seems increasingly likely that the Policy Board will introduce new guidelines. (See MNI BoJ Preview here)

- Cash US tsys are little changed in today’s Asia-Pac session ahead of today’s US CPI data and the FOMC policy decision.

- Cash JGBs are richer, with yields flat to 3.2bps lower. The benchmark 10-year yield is 3.0bps lower at 0.997% versus the cycle high of 1.101%.

- Swap rates are ~1bp lower. Swap spreads are wider.

- Tomorrow, the local calendar will see Weekly International Investment Flow data and results of the Q2 BSI Large Company Survey. The MoF will also conduct a Liquidity Enhancement Auction for OTR 15.5-39-year JGBs.

BOJ: MNI BoJ Preview - June 2024: Steady Policy Rate, Focus On JGB Purchases

EXECUTIVE SUMMARY

- At this week’s meeting, we anticipate that the BoJ will maintain its policy rate settings (keeping the target for the overnight uncollateralized call rate at 0-0.1%) on June 14, in line with consensus. Recent economic data around prices and growth suggest this approach.

- Nevertheless, the trend towards normalisation continues. The BoJ's sensitivity to foreign exchange rates has also shifted in recent months. We expect a generally hawkish tone at the meeting, indicating the possibility of additional policy tightening in subsequent meetings, possibly as soon as July.

- The focus for the June meeting will likely be on balance sheet policy and the future pace of JGB purchases.

- It is uncertain whether the BoJ will revise its JGB purchase directive this week. However, it seems increasingly likely that the Policy Board will introduce new guidelines, as suggested by recent reports indicating a potential discussion on publishing a more specific schedule for reduced JGB purchases as early as the June meeting

- The Reuters poll showed that 63% of economists predict the BoJ will decide to start reducing bond buying at the June meeting, up from 41% in May.

- Regardless of the decision at this week’s meeting, we expect the BoJ to proceed cautiously and gradually in both hiking the policy rate and adjusting JGB purchases.

- Full preview here:

AUSSIE BONDS: Early Gains Relinquished, May’s Employment Report Tomorrow

In roll-impacted trading, ACGBs (YM +0.4 & XM +1.6) are largely unchanged after relinquishing the early gains driven by yesterday’s rally in US tsys. With US tsy yields steady during today’s Asia-Pac session and no significant domestic events on the calendar, the retreat from the session's peak levels likely reflects position squaring ahead of US CPI data and the FOMC policy decision.

- Cash ACGBs are 1-2bps richer, with the AU-US 10-year yield differential at -10bps.

- Swap rates are flat to 1bp lower.

- The bills strip is little changed, with pricing flat to +1.

- RBA-dated OIS pricing is unchanged across meetings. 5bps of easing is priced by year-end.

- Tomorrow, the local calendar will see the Employment Report and CBA Household Spending data.

- May jobs data will be watched closely given the RBA’s dual mandate. While the labour market remains tight, there are signs it is gradually easing. The data has been volatile lately so it will continue to be important to look through that volatility to the underlying trends. Bloomberg consensus expects 30k new jobs with the unemployment rate easing by 0.1pp to 4.0%.

- If employment comes in close to consensus at 30k, it will be slightly higher than the 6-month average to April but a lot lower than the 3-month average of around 50k.

AUSTRALIAN DATA: SEEK Data Show Easing Jobs Market

SEEK new job ads fell 0.6% m/m in May after a sharp 4.9% drop in April. They are now down 17.9% y/y after -18.6%. While 3-month momentum is still negative, it is not as weak as it was. Growth in applicants per job slowed to +0.3% m/m in April but is still up almost 60% y/y. Labour demand remains robust but is now well off its 2022 peak, while supply has increased considerably. May employment data print on Thursday and a small drop in the unemployment rate to 4% is expected (see MNI preview).

- The May weakness was not broadbased across Australia with it driven by NSW, Queensland and Victoria. Job ads rose in the smaller states, but all regions are down on the year.

- Again the May drop was not consistent across sectors with those dominated by the public sector showing increases, such as education and healthcare. Surprisingly the struggling retail sector posted a 0.9% m/m rise to be down 15% y/y. Trades & services fell 1.6% m/m and 16.1% y/y.

Source: MNI - Market News/SEEK

Australia SEEK applicants/job ad index 2013=100

Source: MNI - Market News/SEEK

NZGBS: Little Changed, Narrow Ranges Ahead Of US CPI & FOMC Decision

NZGBs closed slightly cheaper, with yields flat to 1bp higher and the 2/10 curve steeper. Ranges were relatively narrow ahead of key events in the US later today: CPI is at 0830ET, with the FOMC policy announcement at 1400ET and Fed Chairman Powell’s presser at 1430ET.

- The market ascribes no chance for a rate cut at this meeting but will be seeking guidance on the timing of the first rate cut. The dot plot projections are likely to show the median FOMC member expecting just one or two rate cuts this year (down from three previously projected).

- The NZGB 10-year has underperformed its $-bloc counterparts over the past 24 hours, with the NZ-US and NZ-AU 10-year differentials 5bps and 1bps wider respectively. Nevertheless, both differentials remain close to the narrowest levels seen over the past year.

- Swap rates closed 1bp lower.

- RBNZ dated OIS pricing closed 2bps softer for meetings beyond October. A cumulative 25bps of easing is priced by year-end.

- The local calendar will see Card Spending data tomorrow alongside the NZ Treasury’s planned sale of NZ$250mn of the 3% Apr-29 bond, NZ$200mn of the 2% May-32 bond and NZ$50mn of the 2.75% Apr-37 bond.

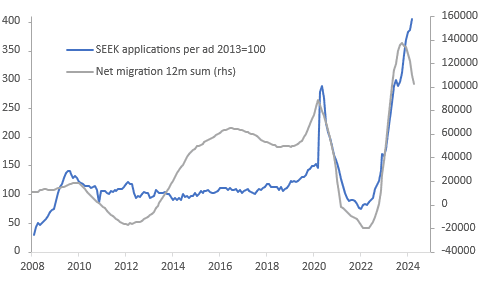

NEW ZEALAND DATA: Migration Gains Off Peak But Still Elevated

NZ saw a net migration gain of 7380 in April after an upwardly revised 4910. This was the largest increase this year and the 12-month sum remains elevated but it peaked in October and continued trending lower in April.

- Strong migration has added to the labour supply and helped to reduce tightness in the labour market. SEEK applications per ad are at very high levels and while they may turn down soon, they are likely to remain elevated. Weaker job prospects are probably weighing on NZ’s attractiveness as a destination and it seems to be driving an increase in departures.

- While stronger supply of labour reduces inflationary pressures, the rise in the working age population is putting pressure on housing, especially rents. So, the RBNZ is likely on hold for the foreseeable future.

- Westpac notes that both inflows and outflows of people were strong in April, which may be due to the April school holidays. There was a large rise in “migrants” on visitor visas.

- ASB points out that growth in tourist numbers is slowing and that will weigh on NZ growth.

NZ net migration vs job applications

Source: MNI - Market News/SEEK/Refinitiv

FOREX: Dollar Steady, US CPI & FOMC Coming Up

Outside of a modest pop higher in AUD, G10 FX trends have been very quiet ahead of key US event risk later, with CPI due, followed by the FOMC later on.

- The BBDXY sits around 1266.45, little changed for the session, but close to recent highs. US equity futures are up a touch, while US yields are firmer, but gains are less than 1bps.

- Regional equity markets are mixed, Hong Kong and China markets are mostly lower.

- USD/JPY is around 157.15/20 little changed for the session. We had stronger than expected PPI data earlier, but this didn't impact sentiment.

- AUD/USD has recovered from earlier lows, last near 0.6615, which is around option expiry strikes for NY cut later today. So that may be playing a role, while slightly lower USD/CNH levels are another potential positive. China May inflation data was close to expectations, but isn't suggesting a sharp pick up in domestic demand.

- NZD/USD is relatively steady, last around the 0.6145 level.

- Later the Fed is expected to hold rates steady but increase its 2024 and 2025 median rate forecast. US May headline CPI is projected to be steady at 3.4% while core should ease 0.1pp to 3.5%. The ECB’s Tuominen, Schnabel, Buch, de Guindos and McCaul, and BoC’s Macklem speak.

ASIA STOCKS: China & Hong Kong Equities Mixed On Disappointing China CPI Data

Hong Kong and China equity are mostly lower today. The Hang Seng index slipped below the crucial 18,000 level due to disappointing China CPI data and speculation about new US chip restrictions. Despite these losses, mainland Chinese investors continued their buying streak of Hong Kong stocks for the 18th consecutive session, with net purchases reaching HK$321.3 billion this year. Additionally, Chinese regulators are considering stricter rules on how banks sell financial products, which could impact distribution channels for major hedge funds.

- Hong Kong equities are lower today, HSTech Index is down 1.51%, while the Mainland Property Index is down 2.72% and the HS Property Index is down 2.10%, the HSI is down 1.45%

- China onshore equities are mixed today. The CSI300 Real Estate Index is one of the worst performing indices, down 1.24%, small-cap indices are higher with the CSI1000 is up 0.37%, the CSI2000 down 1.32%, while the CSI300 is down 0.17%.

- In the property space, China’s daily new home transaction volume increased by more than 60% during the Dragon Boat Festival (June 8-10) compared to the recent May Day holiday, indicating a market recovery following market-boosting policies, according to Securities Times. However, on a year-on-year basis, the daily transaction volume in 30 major cities declined by 16% during the Dragon Boat Festival.

- PBoC Governor Pan Gongsheng pledged to enhance the dual-pillar regulatory framework of monetary and macro-prudential policy, according to an article in People’s Daily. The PBOC aims to deepen market-oriented reforms of interest rates and exchange rates. Additionally, China Securities Regulatory Commission chief Wu Qing stated that the CSRC will expedite the development of a comprehensive capital market supervision system.

- Earlier, China's PPI for May was -1.4% y/y vs -1.5% est, while May CPI was 0.3% vs 0.4% est.

- (MNI) China Press Digest June 12: PBOC, Shipping Price, Emission (See link)

ASIA PAC STOCKS: Asian Equities Mixed, Ranges Tight Ahead Of US CPI & FOMC Later

Asian equities had a mixed performance this morning. Shares of Apple suppliers in South Korea and Japan advanced after Apple's record high on AI hopes, while Japanese stocks overall fell due to a weaker yen and cautious sentiment ahead of key US inflation data and a Federal Reserve rate decision. Conversely, Australian stocks fell, led by the mining sector, ahead of upcoming jobs data. The MSCI Asia Pacific declined as much as 0.40%.

- Japanese stocks dare lower today, with the downturn following a slip in the US Dow overnight, despite gains in the tech-rich Nasdaq and S&P 500 driven by a surge in Apple shares. Major companies like Toyota Motor, Daiichi Sankyo, and Sony Group contributed to the losses, reflecting investor caution ahead of a busy night for US data with the FOMC and the release of US inflation data. The market's apprehension is further compounded by concerns over the Bank of Japan's potential monetary policy actions to address the weak yen. The Nikkei 225 is 0.63% lower, while the Topix is 0.70% lower.

- South Korean stocks are slightly higher today, with shares of Apple suppliers advancing after Apple's record high on new AI features. The Kospi index saw gains as investors responded to the strong performance of Wall Street's tech sector. Morgan Stanley analysts recommended buying shares in the iPhone supply chain, suggesting that companies like Hon Hai, Largan, Luxshare, Genius, AAC, and Foxconn Industrial Internet could benefit from weak traction in Huawei’s newly launched Pura smartphone. The Kospi is 0.44% higher, while the small-cap Kosdaq is up 0.15%

- Taiwan equities are higher today, led higher by tech names. Foreign investors have been selling local stocks recently, with a large $1b outflow on Tuesday, although domestic investors have been able to easily absorb the supply with the Taiex trading near record highs. Focus will now turn to the central bank rate decision tomorrow. The Taiex is up 1% today.

- Australian stocks are lower today, the decline was primarily driven by weakness in the mining sector, reflecting broader concerns ahead of significant economic data releases. Investors are focused on the Federal Reserve's interest rate decision and US inflation data due tonight, while attention will shift to Australian jobs data on Thursday. The downturn in Australian equities mirrors a mixed performance across the Asia-Pacific region, with broader market volatility anticipated due to these pivotal economic developments. The ASX200 is down 0.60%

- Elsewhere in SEA, New Zealand Equities are unchanged, Singapore equities are 0.16% higher, Malaysian equities are 0.15% higher, Indian equities are 0.50% higher, while Indonesian equities are lower at the currency hits 4 year lows and Morgan Stanley downgrades local stocks to underweight.

OIL: Crude Stronger Ahead Of Fed & US CPI

Oil prices continued rising during APAC trading today ahead of the Fed decision and US CPI data later today. Brent is up 0.4% to $82.27/bbl and has spent most of the session trading above $82. It is close to the intraday high of $82.29. WTI has moved above $78 and is currently around 0.6% higher at $78.35/bbl after a peak of $78.39. The USD index is slightly stronger.

- Bloomberg reported a US crude stock drawdown of 2.4mn barrels last week, according to people familiar with the API data. Gasoline fell 2.5mn but distillate rose 1mn. The official EIA data is out later today.

- Reports on Tuesday showed that OPEC still expects a pickup in crude demand in H2 and a supply shortfall while the US’ EIA revised up its US output projections to a new record high. The global IEA will release its monthly report later today.

- ING expects a large market deficit in Q3 which should support oil prices.

- Later the Fed is expected to hold rates steady but increase its 2024 and 2025 median rate forecast (see MNI Fed Preview). US May headline CPI is projected to be steady at 3.4% while core should ease 0.1pp to 3.5% (see MNI US Preview).

- The ECB’s Tuominen, Schnabel, Buch, de Guindos and McCaul, and BoC’s Macklem speak. UK April trade and monthly GDP print.

GOLD: Steady Ahead Of US CPI & FOMC Decision

Gold is little changed in the Asia-Pac session, after closing 0.3% higher at $2317.01 on Tuesday.

- Bullion was supported by lower US Treasury yields, which in turn were buoyed by haven demand associated with European Parliament elections and the surprise snap election called in France. Solid demand metrics at a 10Y auction added to US Treasuries’ strength.

- The 10-year yield finished 7bps lower at 4.40%, with 2-year was down 5bps to 4.83%.

- Later today, the US calendar delivers US CPI at 0830ET today, with the FOMC policy announcement at 1400ET and Fed Chairman Powell’s presser at 1430ET.

- The market ascribes no chance for a rate cut at this meeting but will be seeking guidance on the timing of the first rate cut. The dot plot projections are likely to show the median FOMC member expecting just one or two rate cuts this year (down from three previously projected).

- According to MNI’s technicals team, the yellow metal cleared support around the 50-day EMA, at $2,315.2, in last week’s sharp sell-off, opening $2,277.4, the May 3 low. Initial resistance to watch is $2,387.8, Friday’s high.

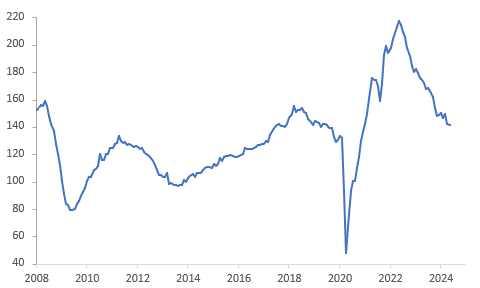

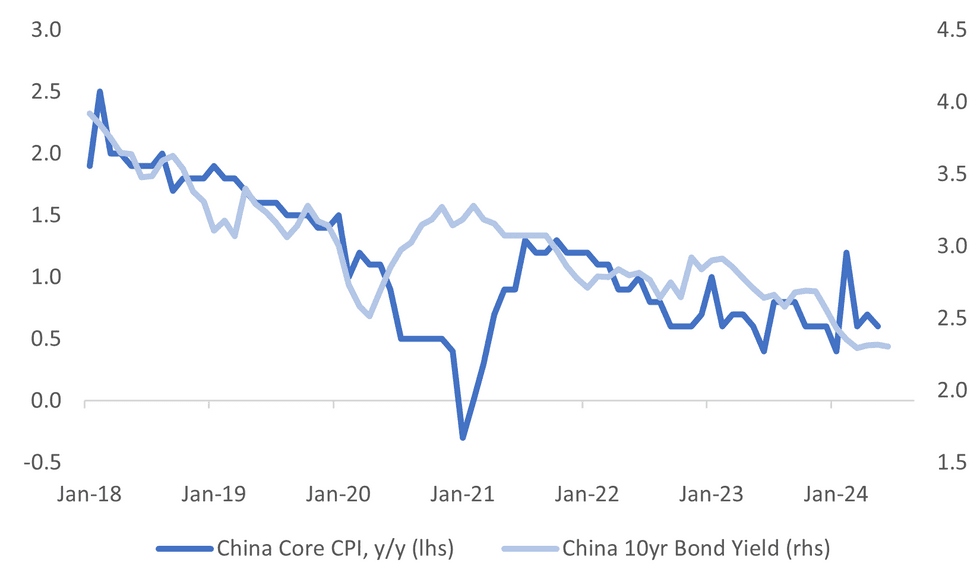

CHINA DATA: CPI Pressures Remain Benign, PPI Aided By Higher Commodities, Base Effects

China May inflation data was close to expectations. Headline CPI rose 0.3% y/y, against a 0.4% forecast and 0.3% in April. The PPI was -1.4% y/y, against a -1.5% forecast and -2.5% prior.

- The detail on the CPI still suggests quite a benign domestic price backdrop. In m/m terms prices fell 0.1%. Consumer good prices were flat in y/y terms, services were 0.8% y/y, unchanged from April. Goods price deflation has ended, but services prices are off the pace from the second half of 2023.

- Core inflation (ex food and energy) was 0.6% y/y, down slightly from April's 0.7% pace. The trend remains benign, albeit up from recent lows. The chart below overlays the 10yr CGB yield against core CPI y/y.

- In terms of the sub categories, we saw drags from food and transport. The main positives were clothing, recreation and the other segment. Only one category saw a pick up in y/y pace versus the April outcome, which was food, but it remained negative in an outright sense.

Fig 1: China Core CPI Y/Y Versus 10yr CGB Yield

Source: MNI - Market News/Bloomberg

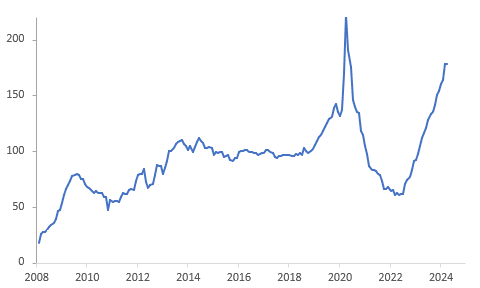

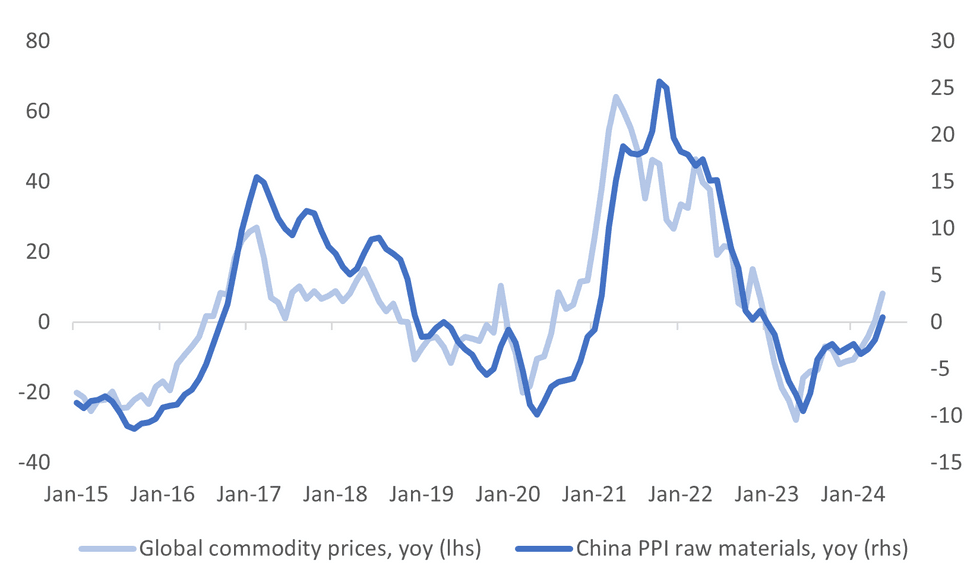

- For the PPI, base effects are favorable for a further improvement in y/y momentum over the next few months.

- The global commodity price backdrop is also helping. The second chart below plots the raw materials sub index of the PPI (which ticked up into positive territory, +0.5% y/y), against spot global spot commodity price changes y/y. Mining and manufacturing PPI's were also less negative in y/y terms in May.

- Consumer goods remained negative and close to the April y/y pace.

Fig 2: China PPI Raw Materials & Global Commodity Prices Y/Y

Source: MNI - Market News/Bloomberg

SOUTH KOREA: Unemployment Rate Steady, But Jobs Growth Momentum Slows

For May, South Korea's unemployment rate held steady at 2.8%, which was in line with the consensus forecast and the prior April outcome.

- The unemployment rate has largely been wedged between 2.5-3.0% since early 2022. On the jobs front, there were 80k job created in May versus a year ago.

- This a step down from the prior pace. In April we had +261k jobs added from a year prior and in Jan-Feb this was running in excess of 300k.

- May's 80k rise was the slowest pace since early 2021, so there are signs of softening jobs growth momentum.

ASIA FX: Close To Unchanged Ahead Of Key US Events

Asia currencies sit modestly stronger against the USD in the first part of Wednesday dealings. Overall moves are fairly muted though, ahead of key event risks (CPI/FOMC) in the US later on Wednesday. Still to come in the region is India CPI and IP data later.

- USD/CNH sits back under 7.2700 after finding selling interest above this figure level earlier. The USD/CNY fixing was steady, which lent some support to the yuan, although spot onshore gains have been limited. Onshore equites are down modestly, while inflation data still suggested a fairly benign domestic demand backdrop.

- 1 month USD/KRW has moved away from earlier highs near 1378 and is back around 1375, which is very much within recent ranges. Onshore equities are higher, which may be helping at the margins. Earlier data showed a steady unemployment rate, but loss of momentum in terms of jobs growth.

- It is close to very steady elsewhere. USD/IDR spot remains close to the 16300 level. Offshore investors sold local equities for the 14 straight session yesterday. The local JCI equity index is off over 6% from mid May highs, as local fiscal concerns/higher for longer Fed weigh.

- USD/THB is in the 36.70/75 region, also little changed for the session. Focus is on the upcoming BoT decision later today. No change is expected, although domestic political pressure continues to call for easier policy settings. Broader political uncertainties are also potentially curbing offshore investor appetite.

- USD/HKD spot sits just under 7.8100. We are under all the key EMAs, with the 20-day the nearest on the topside around 7.8130. In the past week, upside moves have not been sustained through this resistance point. The 200-day sits around 7.8210, while late May highs rested close to 7.8250. On the downside recent lows rest around 7.8080, so close to current spot levels. Earlier May lows sat at 7.7964. US -HK yield differentials sit off earlier YTD highs. On a 12 month basis we are back to +16bps, on a 3 month basis we are back at +64bps. A concerted dip in USD/HKD (sub the mid point of the peg band), may not materialize until yield differentials are notably lower or threatening a break sub 0bps.

- Elsewhere, USD/MYR is around 4.7170, while USD/SGD tracks close to 1.3530. Philippine markets are closed today.

ASIA RATES: China Yields Higher After CPI/PPI, BoK Governor Comments Signal Easing Later In The Year

Asian government bonds are showing mixed performance, with China's government yields slightly higher and South Korea's sovereign bond curve seeing gains.

- China government bonds are dealing flat to 1bp cheaper after today’s May CPI/PPI data.

- China May inflation data was close to expectations, with the Headline CPI rising 0.3% y/y against a 0.4% forecast and 0.3% in April. Core inflation (ex-food and energy) was 0.6% y/y, down slightly from April's 0.7% pace. The trend remains benign, albeit up from recent lows. The global commodity price backdrop is also helping.

- The PPI was -1.4% y/y against a -1.5% forecast and -2.5% prior.

- South Korean sovereign bond curve has shifted richer, with yields flat to 2bps lower, after annual jobs growth (+80k) fell to its slowest pace since early 2021.

- South Korea's May unemployment rate held steady at 2.8%, which was in line with the consensus forecast and the prior April outcome.

- South Korean sovereign bonds were also supported by comments from BoK Governor Rhee Chang-Yong, who called for a balanced approach in considering the timing of a policy pivot (per BBG). This was interpreted as another sign that the central bank is moving toward easing its restrictive policy later this year as inflation continues to cool. (See link)

INDONESIA: Indonesian Markets Little Changed Today As Investors Await US Data

The Indonesian sov curve has twist-flattened today, better buying seen in the 7yr tenor again. The USD/IDR continues to test 16,300, Morgan Stanley downgrades Indonesian stocks to underweight on concerns around fiscal policy and the weaker IDR, while foreign investors continue to sell local stocks.

- The INDON curve is flatter, pivoting at the 7yr. Yields are are 1-4bps higher today giving back some of yesterday's late moves. The 2Y yield is +1bp at 5.30%, 5Y yield is -2bps at 5.08%, the 10Y yield is -2bp at 5.14%, while the 5-year CDS is 0.5bp higher at 72bps.

- The INDON to UST spread diff the 2Y is now 46bps (+1bp), 5yr is 66bps (+1bp), while the 10yr is 73.5bps (unchanged).

- In cross-asset moves: USD/IDR is little changed today trading at 16,294, with BI intervening around these levels, the JCI is unchanged after earlier making new ytd lows. US Tsys are also little changed today as investors await the FOMC and CPI data tonight.

- Looking ahead: There is little on the local data calendar, focus will turn to the US for hints as to when the US will start to cut rates.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 12/06/2024 | 0600/0700 | ** |  | UK | UK Monthly GDP |

| 12/06/2024 | 0600/0700 | ** |  | UK | Trade Balance |

| 12/06/2024 | 0600/0700 | ** |  | UK | Index of Services |

| 12/06/2024 | 0600/0700 | *** |  | UK | Index of Production |

| 12/06/2024 | 0600/0700 | ** |  | UK | Output in the Construction Industry |

| 12/06/2024 | 0600/0800 | *** |  | DE | HICP (f) |

| 12/06/2024 | 0900/1000 | * |  | UK | Index Linked Gilt Outright Auction Result |

| 12/06/2024 | 0930/1130 |  | EU | ECB's Schnabel at German Finance Committee | |

| 12/06/2024 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 12/06/2024 | - | *** |  | CN | Money Supply |

| 12/06/2024 | - | *** |  | CN | New Loans |

| 12/06/2024 | - | *** |  | CN | Social Financing |

| 12/06/2024 | - |  | UK | Sky News- Election Leaders Event | |

| 12/06/2024 | 1230/0830 | *** |  | US | CPI |

| 12/06/2024 | 1230/0830 | * |  | CA | Intl Investment Position |

| 12/06/2024 | 1300/1500 |  | EU | ECB's De Guindos at MNI Connect Event | |

| 12/06/2024 | 1430/1030 | ** |  | US | DOE Weekly Crude Oil Stocks |

| 12/06/2024 | 1600/1200 | *** |  | US | USDA Crop Estimates - WASDE |

| 12/06/2024 | 1800/1400 | ** |  | US | Treasury Budget |

| 12/06/2024 | 1800/1400 | *** |  | US | FOMC Statement |

| 12/06/2024 | 1915/1515 |  | CA | BOC Governor Macklem speaks at panel in Montreal. |