MNI EUROPEAN MARKETS ANALYSIS: China Equities Lag Risk Mood

- Risk appetite mostly stayed firmer, particularly in the G10 FX space, with NZD/USD rallying through its simple 200-day MA resistance. AUD/USD also posted strong gains. Regional equities are mostly higher, on tariff reprieve hopes. China markets have lagged though.

- US Tsy Secretary Bessent stated the US have lots of tools to calm the bond market, but this isn't needed yet. Fed speak from Bostic was cautious.

- The US 10-year yield has continued to drift lower in a tight range in Asia.

- Looking ahead, UK unemployment, FR CPI, ECB Lending Survey, Ger ZEW, Empire State Man survey in the US is all on tap.

MARKETS

US TSYS: Yields Drift Lower in Today's Asia-Pac Session

TYM5 has traded in a tight 110-19/110-27+ range so far in today's Asia-Pac session. Going into the London open, it is dealing near its highs around 110-26,+0.02 from its close.

- The US 10-year yield has continued to drift lower in a tight range of 4.3408 - 4.3856 in Asia. Going into the London open dealing around 4.3485%.

- The market is starting to realise the FED will not be stepping in to rescue it by cutting rates, as long as it expects inflation to track higher on the back of Trump’s policies.

- The Fed’s Waller said yesterday the impacts of the tariffs on inflation would be temporary. He also described the new policy as “ one of the biggest shocks” on the US economy in decades, the effects of which are highly uncertain.

- Bostic spoke after the US market close: ”Right now range of possible outcomes has multiplied. Inflation still much higher than target. Not in position to boldly move in any direction, need more clarity.”

- Bessent says the Treasury has a big toolkit if needed for Bonds.

- Dips in the 10-year yield back towards 4.25/30% should now find supply, any move back to 5% and above would become problematic for equities.

- Upcoming Data/Events: Retail Sales and Fedspeak from Powell on Wednesday.

AUSSIE BONDS: Follow US Tsys Into A Bull-Flattener, RBA Remains Cautious

ACGBs (YM +2.0 & XM +7.0) are showing a bull flattener in today’s Sydney session.

- The release of the RBA Minutes for the April Meeting was the key domestic driver. The Board judged that economic conditions were broadly in line with forecasts, with inflation gradually declining and the labour market still tight.

- Risks to the outlook were seen as balanced, including global trade uncertainty and domestic factors like wages and productivity.

- Given this, the Board decided to keep the cash rate unchanged, emphasising the need for caution. Future decisions will depend on incoming data, especially on inflation, employment, and global developments.

- Cash US tsys are flat to 4bps richer, with a flattening bias, in today's Asia-Pac session.

- Cash ACGBs are 1-7bps richer with the AU-US 10-year yield differential at -2bps.

- The bills strip has bull-flattened, with pricing flat to +6.

- RBA-dated OIS pricing is flat to 3bps softer across meetings today. A 50bp rate cut in May is given a 36% probability.

- Tomorrow, the local calendar will see the Westpac Leading Index, ahead of March’s Employment Report on Thursday.

- The AOFM plans to sell A$1000mn of the 3.50% 21 December 2034 bond tomorrow.

BONDS: NZGBS: Sharp Bull-Flattening In Line With US Tsys

NZGBs closed at session highs in a bull-flattening move, with benchmark yields falling 5–15bps across the curve.

- The short end underperformed, partly due to a sharper rise in NZ food prices, which climbed 3.5% in the year to March 2025, up from 2.4% in February. Stats NZ attributed the increase primarily to higher prices in the grocery food and meat, poultry, and fish categories, which rose 5.1% and 5.3%, respectively.

- Meanwhile, the long end found support from US tsys. Cash US tsys has bull-flattened during today's Asia-Pacific session, with yields flat to 4bps lower. The US calendar is light today, with attention turning to retail sales and remarks from Fed Chair Powell on Wednesday.

- Swap rates closed flat to 9bps lower, with the 2s10s curve flatter.

- RBNZ dated OIS pricing closed 1-2bps firmer across meetings. 30bps of easing is priced for May, with a cumulative 78bps by November 2025.

- Tomorrow, the local calendar will see Non-Resident Bond Holdings data, ahead of Q1 CPI on Thursday.

- On Thursday, the NZ Treasury plans to sell NZ$275mn of the 3.00% Apr-29 bond and NZ$225mn of the 4.25% May-36 bond.

NEW ZEALAND: Food Prices Up, Other Detail Mixed, Lower Petrol Prices Evident

New Zealand food prices rose 0.5%m/m in March, reversing the fall seen in Feb. Outside of fruit and vegetables prices were all up for the sub-sectors. Stats NZ noted: "Food prices increased 3.5 percent in the 12 months to March 2025, following a 2.4 percent increase in the 12 months to February 2025". We are still well sub 2023 highs though above 12% y/y.

- In terms of the other m/m details released, rents edged up 0.3% (form 0.2%), but petrol and diesel prices were down over 2% in m/m terms. International air travel was also down for the third straight month.

- Domestic air travel, up 2.2%, along with accommodation services, up 5.7%m/m, provided some offset.

- Similar trends were evident in terms of y/y outcomes. Petrol and diesel are down noticeably in y/y terms but above 2024 lows.

- Earlier remarks from RBNZ Chief Economist Conway noted that inflation risks have shifted to the downside. This reflects global trade policy shifts, which will most likely weaken global and NZ growth. The central bank is analyzing the tariff impact ahead of the May MPS, but the scope to cut rates is still there.

FOREX: FX Wrap - USD Move Lower Pauses

The BBDXY has had a tight Asian range of 1229.25 - 1232.89. The move lower is starting to show signs of at least slowing down. The USD has looked in real trouble as a rotation out of US assets seems to be gathering momentum and normal correlations with yield are breaking down.

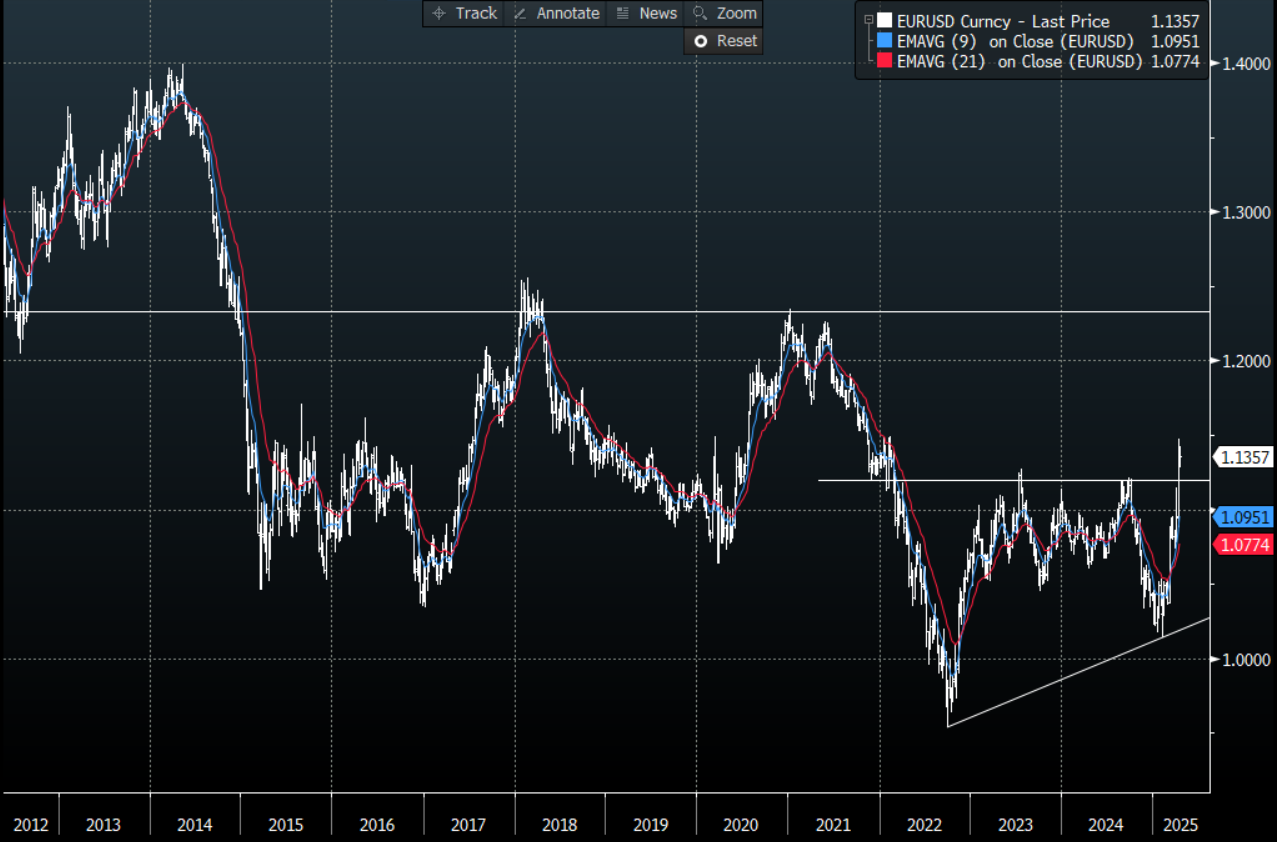

- EUR/USD - Asian range 1.1316 - 1.1361, dipped initially on the Asian open but it has since bounced off its lows dealing around 1.1355 going into London. EUR/USD had been trading very closely with the 10 year rate differential, this relationship broke down completely last week. Traders are targeting a move back to 1.2000 in the Euro as the USD’s safe haven role is reassessed. See graph below.

- GBP/USD - Asian range 1.3164 - 1.3215, dealing right at the day's highs going into the London session. GBP has been playing catch up to the broad USD weakness.

- USD/CNH - Asian range 7.3074 - 7.3189, the USD/CNY fix was slightly lower at 7.2096. USD/CNH goes into the London open dealing around 7.3120.

- USD/JPY - Asian range 142.94 - 143.59, bounced from the open making its highs into the Japanese fix. It has since drifted lower for most of the session going into London back around 143.00. Huge support is eyed around 140, a break here could see the move really accelerate.

- Cross asset : SPX Futures -0.15%, Gold 3229.50, US 10yr 4.35%, BBDXY 1229, Crude oil 61.77.

- Data/Events : UK unemployment, FR CPI, ECB Lending Survey, Ger ZEW, Empire State Man survey.

Fig 1: EUR/USD Weekly Chart

Source: MNI - Market News/BBG

FOREX: Antipodean Wrap - AUD & NZD Make New Gains

The AUD and NZD have both traded bid once more making new highs in Asia. In its minutes The Reserve Bank of Australia expressed caution over future interest-rate cuts, saying May would be an "opportune time" to revisit policy settings. The board will have additional data on the labor market, inflation, household spending, and global trade policies by the May 19-20 meeting, which would have a considerable bearing on the decision.

- AUD/USD - Asian range 0.6316 - 0.6355, AUD has traded quietly bid for most of the Asian session, breaking the overnight highs and going into the London open at the top of its range. Shorts will be hoping for sellers to return but will be watching the 0.6400 area this week for signs of the next leg of position squaring.

- AUD/JPY - Asian range 90.38 - 91.01, AUD/JPY was bid from the open and has drifted higher for the majority of the Asian session. Price goes into the London open around 91.00 pressing its highs. AUD/JPY is trying to build a base as risk stabilises, but it remains to be seen if it can this last. Expect supply once more back towards the pivotal 94.00 area.

- NZDUSD - Asian range 0.5861 - 0.5915, NZD has traded bid the whole session and there is still very little pullback. NZD printing around 0.591/5/20 going into London, having made new highs in the session.

- AUD/NZD - Asian range 1.0734 - 1.0779, the cross drifted lower in the Asian session before finding some buyers towards the 1.0740 area. The cross is going into London pretty directionless but the bias appears to remain for the upside to be capped, as liquidity in the NZD dries up quicker than for the AUD on any move higher.

Fig 1: AUD/USD Daily Chart

Source: MNI - Market News/BBG

ASIA STOCKS: Strong Regional Rally With China Down.

A BBG report suggests that the escalating trade war is having a material impact on the money investors have placed in Chinese ETFs. Data suggests that US$3.6bn has been withdrawn in early April following the imposition of tariffs.

Alibaba and Tencent backed Zhipu has begun an initial public offering as soon as this year, angling to become the first of several prominent ChatGPT-competitors to tap public markets.

Many of Asia’s bourses rose today with the US President floating a potential tariff pause, giving autos a reprieve.

- China’s bourses were the exception today. As the Hang Seng edged higher by +0.20%, the onshore bourses drifted lower with CSI 300 down -0.07, Shanghai down -0.07 and Shenzhen down -0.48%

- The KOSPI had a very strong day today rising +1%, following on from yesterday's gain of +0.95%.

- Singapore’s FTSE Straits Times was one of the regions best performers rising +1.8%, following yesterday’s gain of +1.04%.

- Malaysia’s FTSE Bursa Malaysia KLCI is holding onto modest gains of +0.20% following yesterday's outsized rally of +1.79%.

- The Jakarta Composite is up yet again and continues to perform well, rising +1.3% today, from yesterday’s gains of +1.70%.

- India’s NIFTY 50 has risen +2.1% in early trading, following on from yesterday’s gains of +1.92%.

ASIA STOCKS: Outflows Resume Across the Region

Constant outflows continue to be the thematic we see as we watch the equity flows across the major markets.

- South Korea: Recorded outflows of -$188m as of yesterday, bringing the 5-day total to -$1,584m. 2025 to date flows are -$11,666m. The 5-day average is -$317m, the 20-day average is -$323m and the 100-day average of -$152m.

- Taiwan: Had outflows of -$642m as of yesterday, with total outflows of -$1,402m over the past 5 days. YTD flows are negative at -$18,358. The 5-day average is --$280m, the 20-day average of -$247m and the 100-day average of -$249m.

- India: Had outflows of -$518m as of the 9th, with total outflows of -$2,815m over the past 5 days. YTD flows are negative -$16,476m. The 5-day average is -$563m, the 20-day average of -$44m and the 100-day average of -$150m.

- Indonesia: Had outflows of -$138m as of yesterday, with total outflows of -$488m over the prior five days. YTD flows are negative -$2,318m. The 5-day average is -$98m, the 20-day average -$50m and the 100-day average -$37m

- Thailand: Recorded outflows of -$34m as of the 11th, outflows totaling -$250m over the past 5 days. YTD flows are negative at -$1,396m. The 5-day average is -$50m, the 20-day average of -$25m the 100-day average of -$18m.

- Malaysia: Recorded outflows of -$18m as of yesterday, totaling -$222m over the past 5 days. YTD flows are negative at -$2,796m. The 5-day average is -$44m, the 20-day average of -$60m the 100-day average of -$40m.

- Philippines: Saw inflows of +$3m as of yesterday, with net outflows of -$62m over the past 5 days. YTD flows are negative at -$290m. The 5-day average is -$12m, the 20-day average of -$3m the 100-day average of -$6m.

OIL: Three Straight Days of Gains for Oil

- With ongoing discussions between the US and Iran whilst OPEC cut their forecasts for 2025 and 2026, oil has had a lot to digest.

- OPEC forecasts an increase of 1.3m barrels a day, a reduction of 100k a day as trade war uncertainty weighs on global growth prospects.

- WTI opened at US$61.58, and delivered a third straight day of gains, rising to $61.68

- Brent opened at $64.86, and has rallied to $65.02.

- The global oil market faces “large surpluses” this year and next as the trade war weighs on crude demand growth and OPEC+ eases supply curbs, according to Goldman Sachs. (source BBG)

- JPMorgan has lowered their year end price forecast with Brent to $66 bbl and WTI to $62 bbl

- UBS cut theirs also with Brent to $68

- Hedge funds slashed net-long Brent positions by the most on record in the week to April 8 following the tariff chaos (source BBG)

GOLD: The Rally Returns for Gold.

- Having hit new highs, yesterday saw gold slip lower into the close as profit taking on strong gains was evident yet in the Asian trading day, the rally continued.

- Gold opened at $3,210.93 and had a slow start to the trading day before jumping to $3,228.33, a gain of +0.54%

- South African miner Gold Fields Ltd has been ordered to stop mining its lease and leave one of its mines in Ghana after the rejection of a lease extension.

- West Australian miner Bellevue Gold is the target of several takeovers as the soaring cost of gold eats into its cashflow due to soaring hedge costs.

- The PBOC is offering increased quotas to banks for gold imports to meet the domestic demand from institutional and retail investors.

- Gold remains steadfast above all major moving averages with the nearest, the 20-day EMA, at $3,091.86

CHINA: Country Wrap: UBS Downgrade Growth.

- UBS AG added to a series of growth downgrades for China with the most pessimistic forecast among major banks, predicting the economy will expand just 3.4% this year as US tariffs choke exports. The Swiss bank, which previously saw growth in 2025 at 4%, maintained its estimate for next year at 3%. (source BBG)

- China should cut its interest rates or reserve requirement ratio to stimulate its economy in face of pressure from US tariff hikes, Securities Times reported, citing a recent survey of 57 economists it conducted. Over 80% of the respondents reckon China can cut rates or RRR at an appropriate time

- For additional fiscal stimulus in 2Q, more than 70% of the respondents propose to issue more ultra-long sovereign bonds or cut taxes and fees; about 60% suggest increasing subsidies for lower-income groups; almost half of respondents call for raising the fiscal deficit ratio (source BBG)

- China's bourses were the exception today. As the Hang Seng edged higher by +0.20%, the onshore bourses drifted lower with CSI 300 down -0.07, Shanghai down -0.07 and Shenzhen down -0.48%

- Yuan Reference Rate at 7.2096 Per USD; Estimate 7.3075

- A quiet day for bonds with the CGB 10Yr unchanged at 1.66%

SOUTH KOREA: Country Wrap: Deputy PM Proposes Increase to Supplementary Budget:

- Korea's Deputy Prime Minister and Finance Minister Choi has proposed an increase to the already additional budget to KRW12tn (US8b) to support key industries that will suffer from the trade war and to respond to the recent natural disasters. The budget is KRW2tn more than previously proposed supplementary budget to support the economy. Choi indicated that the supplementary budget would focus on disaster and emergency response, strengthening competitiveness in trade and AI and supporting the livelihoods of people. (source MNI – Market News)

- South Korea's money supply rose for the 21st consecutive month due to strong demand for deposits and profit-making securities, central bank data showed Tuesday. The seasonally-adjusted M2, or broad money, gained 0.6 percent to 4,229.5 trillion won (2.97 trillion U.S. dollars) in February compared to the previous month, continuing to increase since June 2023, according to the Bank of Korea (BOK). The continued growth was attributed to solid demand for profit-sharing securities and time deposits with a maturity of less than two years. (source Xinhua)

- The KOSPI had a very strong day today rising +1%, following on from yesterday's gain of +0.95%.

- KRW had a strong day with gains of +0.10% to be at 1,420.80

- Bonds were strong across the curve with the 10YR the best performer down -3.5bps at 2.67%

INDIA: Country Wrap: In Depth Trade Discussions to Start.

- India will start sector-specific trade discussions with the US next week with key agreements hoping to be in place within six weeks. (source BBG)

- The Reserve Bank of India will buy 400 billion rupees ($4.6 billion) of bonds through open market operation auctions on April 17, according to an official statement. (source RBI)

- India's NIFTY 50 has risen +2.1% in early trading, following on from yesterday's gains of +1.92%.

- INR: the rupee is having another strong day, rising +.44% to be 85.66.

- Bonds are strong following the announcement of the OMO with the 10YR -3bps at 6.41%

INDONESIA: Country Wrap: 2Q Bond Issuance to Decline

- An Indonesia delegation will propose Indonesian investment into the US and increased imports of US goods to reduce the trade gap as ways forward to mitigate tariffs (source BBG)

- Following on from IDR222tn of new issuance in the first quarter, the government’s planned issuance is set to drop in Q2 to IDR190tn according to a release from the Finance Ministry (source BBG)

- The Jakarta Composite is up yet again and continues to perform well, rising +1.3% today, from yesterday's gains of +1.70%.

- IDR was one of the few decliners today, losing -0.07 to be 16,801

- Bonds had a very strong day with yields 2-6bps lower. INDOGB 10YR 6.98% -4bps

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 15/04/2025 | 0600/0700 | *** | Labour Market Survey | |

| 15/04/2025 | 0645/0845 | *** | HICP (f) | |

| 15/04/2025 | 0800/1000 | ** | ECB Bank Lending Survey | |

| 15/04/2025 | 0900/1100 | ** | Industrial Production | |

| 15/04/2025 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 15/04/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 15/04/2025 | 1215/0815 | ** | CMHC Housing Starts | |

| 15/04/2025 | 1230/0830 | *** | CPI | |

| 15/04/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 15/04/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 15/04/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 15/04/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 15/04/2025 | 1300/0900 | * | CREA Existing Home Sales | |

| 15/04/2025 | 1530/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 15/04/2025 | 2310/1910 | Fed Governor Lisa Cook | ||

| 16/04/2025 | 2350/0850 | * | Machinery orders | |

| 16/04/2025 | 0200/1000 | *** | Fixed-Asset Investment | |

| 16/04/2025 | 0200/1000 | *** | Retail Sales | |

| 16/04/2025 | 0200/1000 | *** | Industrial Output | |

| 16/04/2025 | 0200/1000 | *** | GDP | |

| 16/04/2025 | 0200/1000 | ** | Surveyed Unemployment Rate M/M | |

| 16/04/2025 | 0600/0700 | *** | Consumer inflation report | |

| 16/04/2025 | 0800/1000 | ** | EZ Current Account | |

| 16/04/2025 | 0800/1000 | ** | Italy Final HICP | |

| 16/04/2025 | 0900/1100 | *** | HICP (f) | |

| 16/04/2025 | 1000/1100 | ** | Gilt Outright Auction Result | |

| 16/04/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 16/04/2025 | 1230/0830 | *** | Retail Sales | |

| 16/04/2025 | 1315/0915 | *** | Industrial Production | |

| 16/04/2025 | 1345/0945 | *** | Bank of Canada Policy Decision |