EM LATAM CREDIT: MNI EM Credit Market Wrap - LATAM (29 May)

Source: BBG

Measure Level Δ DoD

5yr UST 4.00% -7bp

10yr UST 4.42% -6bp

5s-10s UST 42.4 +1bp

WTI Crude 61.0 -0.9

Gold 3320 +32.9

Bonds (CBBT) Z-Sprd Δ DoD

ARGENT 3 1/2 07/09/41 854bp +11bp

BRAZIL 6 1/8 03/15/34 262bp +1bp

BRAZIL 7 1/8 05/13/54 371bp +0bp

COLOM 8 11/14/35 405bp +0bp

COLOM 8 3/8 11/07/54 497bp +1bp

ELSALV 7.65 06/15/35 451bp +2bp

MEX 6 7/8 05/13/37 274bp -5bp

MEX 7 3/8 05/13/55 340bp -4bp

CHILE 5.65 01/13/37 152bp -1bp

PANAMA 6.4 02/14/35 331bp -2bp

CSNABZ 5 7/8 04/08/32 574bp +10bp

MRFGBZ 3.95 01/29/31 287bp +4bp

PEMEX 7.69 01/23/50 660bp +7bp

CDEL 6.33 01/13/35 219bp +2bp

SUZANO 3 1/8 01/15/32 211bp +2bp

FX Level Δ DoD

USDBRL 5.66 -0.03

USDCLP 936.15 -4.78

USDMXN 19.3 -0.08

USDCOP 4120.63 -4.95

USDPEN 3.62 -0.02

CDS Level Δ DoD

Mexico 120 (2)

Brazil 162 (2)

Colombia 228 0

Chile 58 0

CDX EM 96.85 (0.03)

CDX EM IG 100.93 0.02

CDX EM HY 92.71 0.02

Main stories recap:

Comments

· From the 1st quarter GDP report, consumer spending was revised lower while weekly initial jobless claims moved higher and pending home sales fell more than expected which all added up to economic weakness that was supportive for U.S. Treasury prices and reflected in a spectacular 7-year note auction that triggered further gains later in the day.

· The primary market was active once again in Asia and CEEMEA with a few new issues while LATAM was quiet with no new mandate announcements.

· Secondary market EM Asia and CEEMEA benchmark USD bond spreads had a tightening bias but as the macro backdrop shifted LATAM spreads trended wider as bond prices failed to keep up with falling Treasury yields.

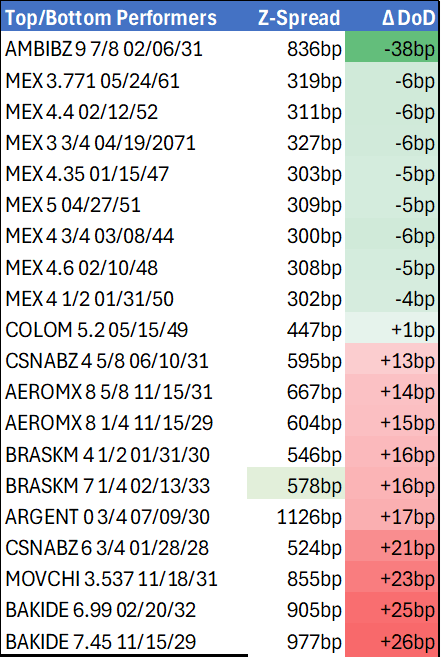

· Brazil’s environmental services company Ambipar outperformed with bonds up almost 2 points but that was after yesterday’s 5 points rout. The company announced a corporate restructuring today that followed yesterday’s reaction to a delayed filing of the 20-F SEC annual report filing.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Modest Risk On - Domestic Automakers Hopeful For Tariff Relief

- Treasuries look to finish near near midday highs Tuesday, curves mildly steeper amid decent short end support all day (conditional steepeners via options, Block buying SOFR White packs) as Trump officials reported progress in tariff negotiations without much hard facts.

- Pres Trump to announce "more tariff relief" at a rally in Michigan this afternoon, "domestic automakers will be happy" WH Deputy Chief of Staff Miller said.

- Cautious risk-on support in rates buoyed projected rate cut pricing in the later half of the year (Sep at -61.0bp) while stocks finished near moderate session highs (SPX eminis +35.0 at 5588.0).

- The JOLTS report saw a second month with lower-than-expected job openings, and this time by a greater extent in March. However, layoffs fell to their lowest since June and quit rates surprisingly inched higher.

- US consumer confidence dropped for a 5th consecutive month in April following the November peak per the Conference Board's survey, with the Composite to 86.0 (88.0 expected, 93.9 prior upwardly revised from 92.9) - the lowest since May 2020.

- Focus turns to Wednesday's ADP private jobs data, GDP, Chicago PMI, PCE and Home Sales.

AUDUSD TECHS: Short-Term Structure Remains Bullish

- RES 4: 0.6550 61.8% retracement of the Sep 30 ‘24 - Apr 9 bear leg

- RES 3: 0.6528 High Nov 29 ‘24

- RES 2: 0.6471 High Dec 9 ‘24

- RES 1: 0.6450 Intraday high

- PRICE: 0.6388 @ 16:25 BST Apr 29

- SUP 1: 0.6344/6307 Low Apr 24 / 50-day EMA

- SUP 2: 0.6181 Low Apr 11

- SUP 3: 0.6116 Low Apr 10

- SUP 4: 0.5915 Low Apr 9 and key support

The trend condition in AUDUSD is unchanged, it remains bullish and the pair is trading at its recent highs. Price has recently breached a key resistance at 0.6409, the Dec 9 ‘24 high. This breach reinforces bullish conditions and signals scope for a continuation higher near-term. Sights are on 0.6471 next, the Dec 9 2024 high. Initial key support to monitor is 0.6307, the 50-day EMA. A clear break of this EMA would be a concern for bulls.

PIPELINE: Corporate Bond Roundup: $9B World Bank 2Pt Lion's Share $23B Supply

- Date $MM Issuer (Priced *, Launch #)

- 04/29 $9B *World Bank $4B 3Y +35, $5B 7Y +55

- 04/29 $5B *KFW 5Y SOFR+42

- 04/29 $2B *ADQ $1B 5Y +85, $1B 10Y +95

- 04/29 $1.75B *Swedish Export Credit 3Y SOFR+45

- 04/29 $1.5B #Las Vega Sands $1B 3Y +200, $500M 5Y +225

- 04/29 $1B *GS Private $400M 3Y +225, $600M 5Y +250

- 04/29 $900M *Tyco Electronics $450M each: +5Y +83, 10Y +97

- 04/29 $800M *Weir Group 5Y +160

- 04/29 $500M *Constellation Brands 5Y +107

- 04/29 $500M *Southwestern Public Service 10Y +115

- 04/29 $Benchmark Bahrain 12Y, 8Y Sukuk investor calls

- Expected Wednesday:

- 04/30 $Benchmark IADB 5Y SOFR+45a

- 04/30 $Benchmark CoE Dev Bank 3Y SOFR+37a

- 04/30 $Benchmark Nordic Investment Bank 5Y SOFR+44a