EM LATAM CREDIT: LATAM Credit Market Wrap

Source: Bloomberg Finance L.P.

Measure Level Δ DoD

5yr UST 3.69% -0bp

10yr UST 4.21% -3bp

5s-10s UST 50.9 -3bp

WTI Crude 64.3 +0.2

Gold 3420 +22.9

Bonds (CBBT) Z-Sprd Δ DoD

ARGENT 3 1/2 07/09/41 1073bp -14bp

BRAZIL 6 1/8 03/15/34 241bp -5bp

BRAZIL 7 1/8 05/13/54 334bp -5bp

COLOM 8 11/14/35 356bp -15bp

COLOM 8 3/8 11/07/54 423bp -17bp

ELSALV 7.65 06/15/35 421bp +2bp

MEX 6 7/8 05/13/37 245bp -4bp

MEX 7 3/8 05/13/55 297bp -2bp

CHILE 5.65 01/13/37 140bp -3bp

PANAMA 6.4 02/14/35 267bp -3bp

CSNABZ 5 7/8 04/08/32 569bp +0bp

MRFGBZ 3.95 01/29/31 266bp -0bp

PEMEX 7.69 01/23/50 525bp -11bp

CDEL 6.33 01/13/35 202bp +1bp

SUZANO 3 1/8 01/15/32 176bp -2bp

FX Level Δ DoD

USDBRL 5.41 -0.01

USDCLP 967.85 -0.53

USDMXN 18.6 -0.01

USDCOP 4027.35 -3.19

USDPEN 3.54 -0.01

CDS Level Δ DoD

Mexico 96 (0)

Brazil 137 (3)

Colombia 192 (6)

Chile 51 (1)

CDX EM 98.12 0.10

CDX EM IG 101.48 0.05

CDX EM HY 94.64 0.15

Main stories recap:

· Major U.S. equity indexes made new all-time highs in the wake of strong 2Q U.S. GDP data.

· The U.S. Treasury curve bull flattened with the long end rallying about 5bp ahead of tomorrow’s Core PCE data, the Fed’s preferred inflation gauge, as well as a solid 7-year auction.

· EM primary was relatively quiet, though there were a few new mandates announced, one in CEEMEA for an Arab National Bank USD AT1 and another in LATAM for Chile electric utility Colbun.

· EM secondary benchmark bond spreads trended tighter. In CEEMEA, higher beta African names were 10-24bp tighter in z-spread while in LATAM names like Pemex and Argentina sovereigns tightened 10-15bp.

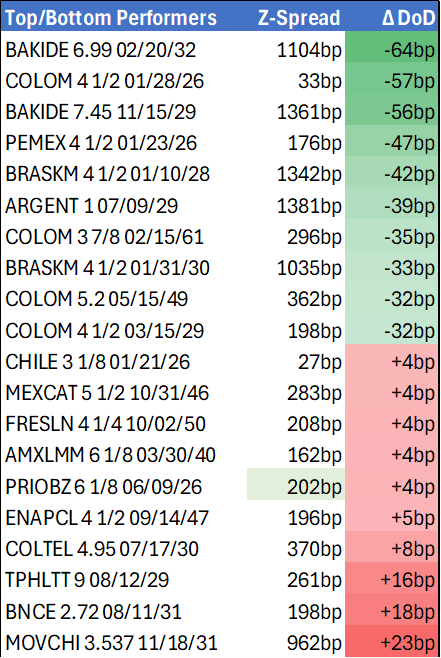

· Colombia sovereign USD bonds were top performers today tightening 15-35bp across the curve. Six major banks announced an offer to buy USD bonds maturing from 2027 to 2061 in anticipation of executing total return swaps (TRS) with the Republic in the future.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Pierces The 50-Day EMA

- RES 4: 1.4016 High May 12 / 13

- RES 3: 1.3920 High May 21

- RES 2: 1.3862 High May 29

- RES 1: 1.3798 High Jun 23 and a key near-term resistance

- PRICE: 1.3771 @ 19:05 BST Jul 29

- SUP 1: 1.3679/3557 20-day EMA / Low Jul 03

- SUP 2: 1.3540 Low Jun 16 and the bear trigger

- SUP 3: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 4: 1.3473 Low Oct 2 2024

A short-term correction in USDCAD remains in play. However, note that price has traded through the 50-day EMA at 1.3728. A clear breach of this average would highlight a stronger short-term reversal, exposing 1.3798, the Jun 23 high. Clearance of 1.3798 would strengthen a bullish condition. On the downside, 1.3540, the Jun 16 low, marks key support. A break of this level would resume the downtrend.

US TSYS: Treasuries Bid Ahead FOMC, Strong 7Y Sale, JOLTS Jobs Recede

- Treasuries look to finish near late session highs, TYU futures back at last week's highs on July 22 as markets consolidate ahead of tomorrow's FOMC rate annc.

- A strong 7Y note auction helped rates extend highs after the $44B note sale (91282CNR8) stopped through again: 4.092% high yield vs. WI of 4.120%; bid-to-cover 2.79x from 2.46x prior. Peripheral stats: Indirect take-up retreats to 62.26% vs. 76.74% prior; Direct take-up climbed to new high at 33.68% vs. 11.62% prior; Dealers fell to new low of 4.06% vs. 11.64% prior.

- First half support: Tsys extended highs briefly after lower than expected JOLTS openings, quits level lower (prior down-revised), layoffs broadly lower than expected. Prior to JOLTS, little react to Advance Goods Trade Balance, import decline and less negative goods export. Wholesale inventories slightly higher than expected, retail inventories in-line.

- Tsy Sep'25 10Y contract trades +19 at 111-11.5 vs. 111-12.5 high; nearing initial technical resistance at 111-14.5 (High Jul 22). A clear break would highlight a stronger reversal and open 111-28, the Jul 3 high. Key support remains intact at 110-08+, the Jul 14 and 16 low. A move through this support would reinstate a bearish theme.

- Curves bull flatten: 2s10s -3.051 at 44.734, 5s30s -3.148 at 95.557.

- Cross asset: Bbg US$ index firmer but off highs: BBDXY +1.65 at 1209.76 (1212.47 high); stocks moderately lower (SPX eminis -19.75 at 6403.0); gold firmer +9.30 at 3323.91.

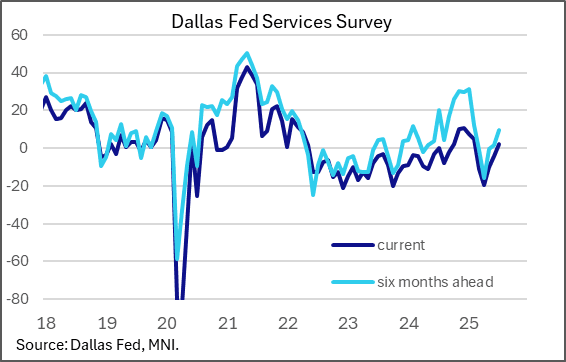

US DATA: Dallas Fed Regional Services Sentiment And Prices Pick Up

The Dallas Fed's Texas Service Sector Outlook Survey has bounced from weak readings in Q2, suggesting a pickup in regional activity to more normal levels after a tariff-related fall in sentiment albeit amid stubborn price pressures.

- General Business activity rose to 2.0 in July from -4.4 prior, marking the first positive reading since February. In tandem, the 6-month outlook rose to 9.8 from 1.5, for the highest reading also since February. Various key metrics improved including revenue, employment, and hours worked, with uncertainty falling to around the longer-term average.

- This echoes improvement in July's Philadelphia, NY, and Richmond services/non-manufacturing surveys (Kansas City was an outlier), as well as the rise in the July flash S&P Global PMI index.

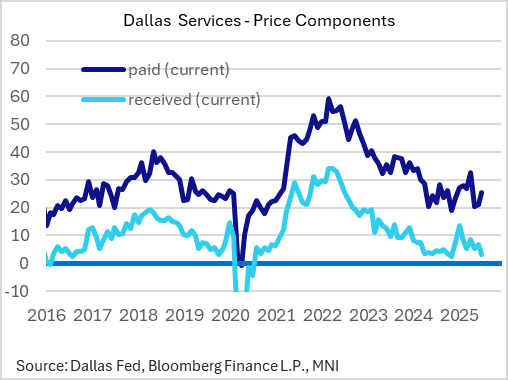

- One area of concern was a renewed pickup in current prices paid, to 25.3 from 21.3 prior for a 3-month high, even as prices received dropped to 3.3 from 6.8 prior, marking an 8-month low. That potentially points to margin pressures for regional services firms.

- Overall services prices paid looked to have steadied/risen in July based on regional Fed surveys - we will preview the ISM Services reading for July ahead of release on August 5.

- Within the survey, Texas retail sales were flat, albeit at 0.8, the sales index was a strong improvement from -29.5 prior.