EM LATAM CREDIT: MNI EM Credit Market Wrap - LATAM (03 Jun)

Source: BBG

Measure Level Δ DoD

5yr UST 4.03% +2bp

10yr UST 4.46% +2bp

5s-10s UST 43.0 -0bp

WTI Crude 63.5 +1.0

Gold 3354 -27.5

Bonds (CBBT) Z-Sprd Δ DoD

ARGENT 3 1/2 07/09/41 857bp -5bp

BRAZIL 6 1/8 03/15/34 259bp -5bp

BRAZIL 7 1/8 05/13/54 365bp -5bp

COLOM 8 11/14/35 398bp -8bp

COLOM 8 3/8 11/07/54 487bp -9bp

ELSALV 7.65 06/15/35 443bp -6bp

MEX 6 7/8 05/13/37 269bp -6bp

MEX 7 3/8 05/13/55 336bp -4bp

CHILE 5.65 01/13/37 149bp -3bp

PANAMA 6.4 02/14/35 326bp -7bp

CSNABZ 5 7/8 04/08/32 580bp +5bp

MRFGBZ 3.95 01/29/31 280bp -2bp

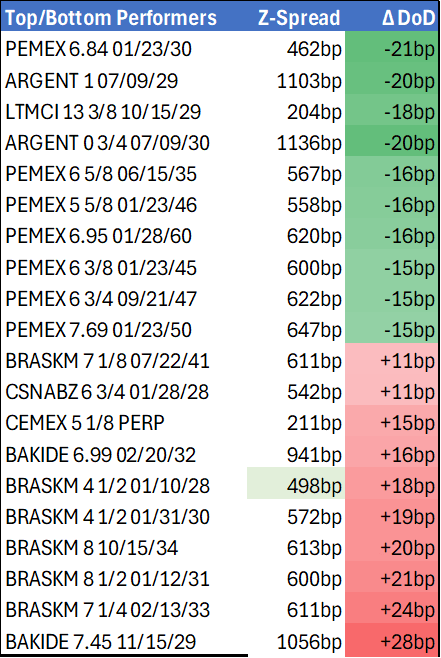

PEMEX 7.69 01/23/50 647bp -14bp

CDEL 6.33 01/13/35 213bp -4bp

SUZANO 3 1/8 01/15/32 204bp -5bp

FX Level Δ DoD

USDBRL 5.64 -0.04

USDCLP 940.55 +1.26

USDMXN 19.2 +0.01

USDCOP 4109.41 -50.02

USDPEN 3.62 +0.00

CDS Level Δ DoD

Mexico 116 (1)

Brazil 156 (3)

Colombia 223 (5)

Chile 57 (1)

CDX EM 97.04 0.09

CDX EM IG 101.04 0.05

CDX EM HY 92.96 0.16

Main stories recap:

Comments

· Rally in U.S. stock indexes and minor sell off in U.S. Treasuries as JOLTs employment data was reported stronger than expected.

· The EM primary market was active with two new issues in Asia and three in CEEMEA. LATAM was quiet today, but three new mandates were announced yesterday so we would expect new issues to be announced tomorrow.

· EM Asia secondary spreads were barely changed while CEEMEA benchmark spreads were mostly 2-5bps tighter. LATAM benchmark spreads were about 3-5bps tighter in low beta and 5-10bps tighter in higher beta bonds.

· Pemex outperformed with spreads moving 15 bps tighter, possibly due to press reports about Mexican billionaire businessman Carlos Slim’s growing investment and influence at the company.

· Ecuador (ECUA; Caa3/B-neg/CCC+) bonds outperformed as well, moving 2 points higher across the curve as the recently appointed finance minister suggested the sovereign could issue bonds in 2026 following or in conjunction with some multilateral support.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Hits Bear Trigger, New Cycle Low

- RES 4: 1.4415 High Apr 1

- RES 3: 1.4296 High Apr 7

- RES 2: 1.4087 50-day EMA

- RES 1: 1.3906/3935 High Apr 17 / 20-day EMA

- PRICE: 1.3793 @ 17:00 BST May 2

- SUP 1: 1.3760 Low Apr 21 and the bear trigger

- SUP 2: 1.3744 76.4% retracement of Sep 25 ‘24 - Feb 3 bull run

- SUP 3: 1.3696 Low Oct 10 2024

- SUP 4: 1.3643 Low Oct 9 ‘24

The trend set-up in USDCAD deteriorated further Friday, with prices slipping through the bear trigger to narrow the gap with next support. The fresh cycle low reinforces the bear cycle and signals scope for a continuation near-term. Potential is seen for a move towards 1.3744, a Fibonacci retracement. Moving average studies are in a bear mode position, highlighting a dominant downtrend. First resistance to watch is 1.3943, the 20-day EMA.

AUDUSD TECHS: Consolidation Phase

- RES 4: 0.6550 61.8% retracement of the Sep 30 ‘24 - Apr 9 bear leg

- RES 3: 0.6528 High Nov 29 ‘24

- RES 2: 0.6471 High Dec 9 ‘24

- RES 1: 0.6470 High May 2

- PRICE: 0.6445 @ 16:59 BST May 2

- SUP 1: 0.6344/6316 Low Apr 24 / 50-day EMA

- SUP 2: 0.6181 Low Apr 11

- SUP 3: 0.6116 Low Apr 10

- SUP 4: 0.5915 Low Apr 9 and key support

AUDUSD remains inside a consolidation phase, having traded either side of the 0.6400 level for 10 consecutive sessions. The underlying trend remains bullish and the pair is trading close to recent highs. Price has recently breached a key resistance at 0.6409, the Dec 9 ‘24 high. This breach reinforces bullish conditions and signals scope for a continuation higher near-term. Sights are on 0.6471 next, the Dec 9 2024 high. Initial key support to monitor is 0.6316, the 50-day EMA. A clear break of this EMA would be a concern for bulls.

US TSYS: Rates Retreat, Sentiment Improved Though Trade Risk Remains

- Treasuries look to finish near late Friday session lows after trading firmer on the open, higher than expected Nonfarm payrolls at 177k (sa, cons 138k) of which private contributed 167k (sa, cons 125k) triggered the early reversal.

- However, two-month revisions of -58k offset the 39k beat for nonfarm payrolls, with a similar story for private (a 42k surprise vs -48k two-month revision).

- Stocks are back near four week highs - pre-"Liberation Day" levels as hopes of some trade deal being made improved sentiment.

- The Wall Street Journal reports that "Beijing is considering ways to address the Trump administration’s gripes over China’s role in the fentanyl trade... potentially offering an off-ramp from hostilities to allow for trade talks to start." The Journal notes that "discussions remain fluid" and China "would like to see some softening of stance from President Trump".

- Currently, the Jun'25 10Y contract trades -20 at 111-07.5 vs 111-02 low -- initial technical support (50-dma) followed by 110-16.5/109-08 (Low Apr 22 / 11 and the bear trigger). Curves bear flattened, 2s10s -3.480 at 48.002, 5s30s -4.911 at 86.807.