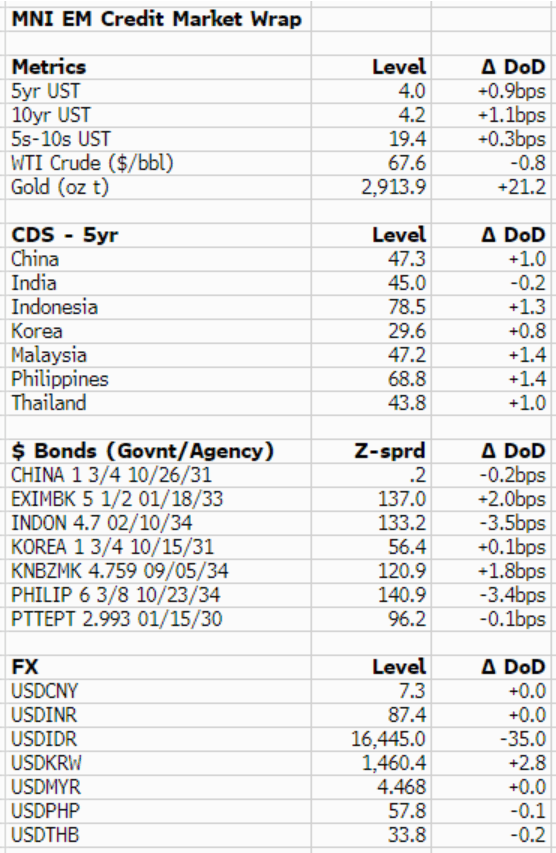

EM ASIA CREDIT: MNI EM Credit Market Wrap - Asia

** The main stories out of the region**

U.S. 10y treasury yields were 1bp higher in Asia hours. U.S. tariffs and related counter tariffs from China fuel growing concern for the global economy. In Asia emerging markets govie/agency bonds we were a bit of a mixed bag with Indonesia and the Philippines outperforming (c. 3.5bp better).

In terms of newsflow, late in the session S&P downgraded LG Chem to mid BBB, stating that leverage is expected to be higher for longer. Negative for spreads. Reliance Industries, after announcing a legal win recently, today said that the case was overturned and the claim has risen to $2.8bn. The company will appeal. Finally, CSSC Shipping signed a contract for $2.6bn to build containerships, but this is somewhat mitigated by U.S. plans to rebalance shipping manufacture to U.S. shipyards.

We also had a couple of new issues, including a Hysan $benchmark perp. non-call 5.5 year. The IPT was 7.6%, and we see fair value around 7.1%. Knowledge City, a government related entity, which is involved in urban development of the Knowledge City area in Guangzhou city also announced a 3y $ benchmark bond with IPT c. 5.8% area.

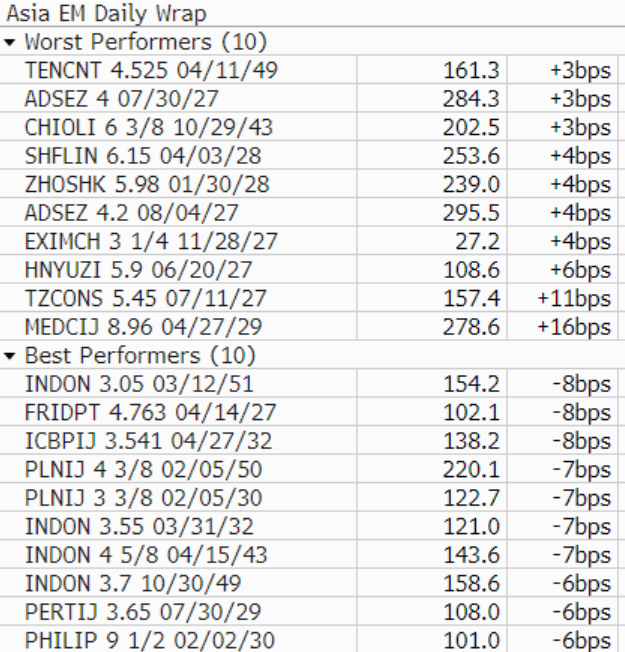

Best & Worst Performers (zsprd, bp)

Source: Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: Powell To Deliver Semi-Annual Testimony In Mid-Feb

The House Financial Services Committee's website confirms that Fed Chair Powell will deliver his semi-annual Monetary Policy Report on Wednesday Feb 12 at 1000ET.

- The Semi-annual testimony will be closely eyed as Powell's first scheduled appearance since the January FOMC - and the House testimony on the 12th is the same day as the release of January CPI (and the week after nonfarm payrolls and benchmark revisions) so will be of particular interest.

US OUTLOOK/OPINION: Nonfarm Payrolls, Revisions Highlight Next Week In US Macro

Friday’s nonfarm payrolls for January highlights the US macro week. It's a highly anticipated report that could alter recent trends considering it will include annual benchmark revisions along with seasonal factors and an updated birth-death model.

- The preliminary estimate for the benchmark revision pointed to the level of payrolls being some 818k lower than currently reported for back in March 2024. There’s a broad expectation from what we can gather that the hit seen next week won’t be as large but it could still be significant. We also watch the seasonal revisions closely, as whilst they should have a zero-sum impact over the calendar year, we’ve noted some particularly favorable seasonal factors in recent months that have biased seasonally adjusted jobs growth higher.

- With these considerations in mind, the early days of the Bloomberg consensus points to nonfarm payrolls growth of 150k after a solid three-month average of 170k. Note that the unemployment rate from the separate household survey won’t be affected by these revisions, having already seen its own seasonal factor revisions last month. A population control will complicate month-on-month changes in the levels of employment and unemployment but shouldn’t be significant for the rate, which is seen unchanged at 4.1% having surprised lower with 4.09% in December. The recent high is technically 4.23% in November having first popped to 4.22% back in July.

- Two other special mentions for the week are: 1) rare remarks from FOMC Vice Chair Jefferson speaking on the economic outlook and monetary policy late on Tuesday with both text and Q&A, having last spoke on Oct 9. 2) ISM services on Wednesday after its priced paid series jumped 5.9pts to 64.4 in December for the highest since Feb 2023.

- Away from macro but still material, the coming week brings the US Treasury's quarterly refunding process - our preview is here.

MACRO ANALYSIS: MNI US Macro Weekly: Uncertainty Vindicates Fed’s Patience

In a largely positive week for economic activity data, including in core durable goods and MNI Chicago PMI, the Q4 GDP accounts stood out by showing a very strong end to 2024 for the consumer.

- As we go to press, though, President Trump has confirmed that tariffs would be imposed on Canada, Mexico, and China beginning this weekend – while also threatening further action against the likes of the European Union and across various import categories.

- The combination of solid growth and policy uncertainty, along with stubborn “supercore” PCE inflation for December, seemingly vindicated the Federal Reserve’s “hawkish hold” at its January meeting.

- A March rate cut is still a possibility but the bar for such an outcome has been set high.

- That gets us to the first key release between now and then: Friday’s nonfarm payrolls for January is the highlight of the US macro week, and could alter recent trends considering it will include annual benchmark revisions along with seasonal factors and an updated birth-death model.

- Other highlights in the upcoming week include ISM Services and the Treasury’s quarterly Refunding announcement (Wednesday), while FOMC Vice Chair Jefferson delivers commentary on the economic outlook and monetary policy Tuesday.

PLEASE FIND THE FULL REPORT HERE: