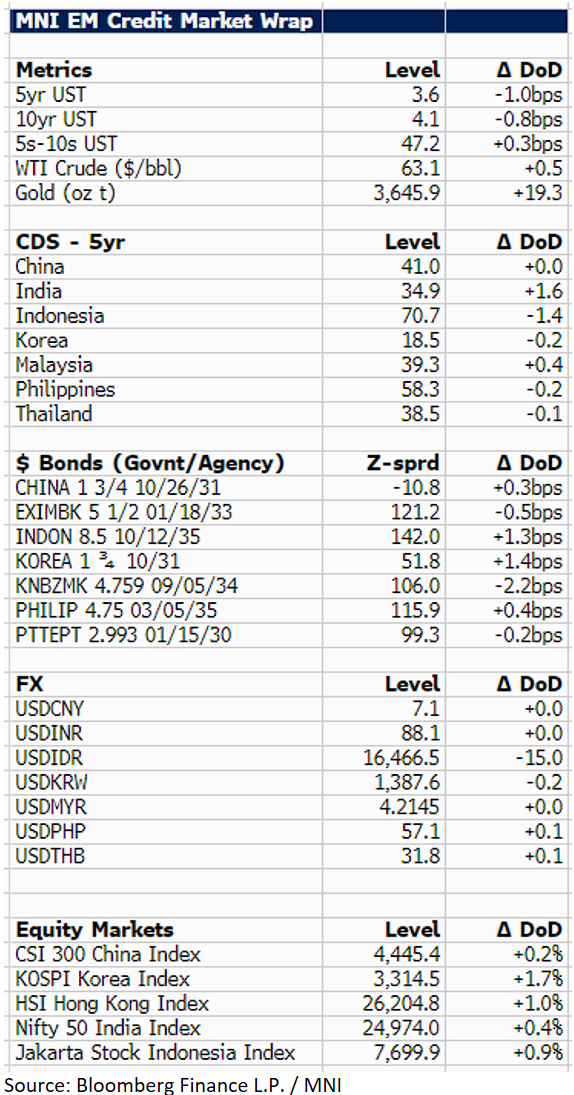

EM ASIA CREDIT: MNI EM Credit Market Update - Asia

US Treasury yields are 1bp lower at 4.1% during the Asia session. We followed LATAM, where benchmark bond spreads were generally 4-7bp tighter but there were some outliers, including those from Argentina and Pemex. In Asia, EM USD sovereign and agency spreads traded in a -2bp to +1bp range, with Malaysia the outperformer. Our Malaysia USD proxy (KNBZMK 34s) is around 2bp tighter, otherwise the bias is wider in Asia. Regional equities are higher, with Indonesia's JCI +1%, a rebound following yesterday's reaction to a change in Finance Minister.

In other news we are hearing India Prime Minister Modi and US President Trump making positive overtures about future talks. Outside of Asia, news that Russian drones entered Polish airspace will be closely monitored by investors.

In corporate news, LG Energy has reportedly halted construction of US plants in response to Korean workers being repatriated after immigration raids, though as of the time of writing deportations were stalled. We also saw a mixed bag in China real estate with Longfor reporting August sales down 27% YoY, while China Jinmao was up 46% in the month. CATL is also reported to be restarting lithium mining operations, which is expected. Korean Telecom is the subject of an investigation into hacking of micropayments, for now its not clear the scale of the breach. Finally, we see a new 5Y USD deal from Korea Housing Finance.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Bull Flattening As Bonds Rally & REC Jobs Report Remains Soft

Gilts rally alongside global peers, with equity indices away from highs and some focus on the potential deflationary impact surrounding this week’s Trump-Putin meeting in Alaska.

- A reminder that Ukrainian President Zelenskiy has pushed back against the idea of land concessions in any peace deal with Russia, seemingly leaving the two sides very much at odds when it comes to pre-requisites surrounding any ceasefire agreement.

- Gilts also benefit from the latest KPMG-REC report on jobs, which pointed to an ongoing slowing of the UK labour market, with wage growth seemingly restrained as businesses react to tax hikes.

- Futures rally to 92.37. Initial resistance of note located at the August 5 high (92.84). Bulls look to regain momentum after a close below the 20-day EMA/

- Yields 4-5bp lower, curve biased a little flatter.

- 2s and 10s move back into the lower half of the ranges witnessed since early June, 2s last 3.86%, 10s last 4.55%.

- 2s10s and 5s30s continue to trade around 70bp & 140bp, respectively.

- Dovish extension in GBP STIRs given the rally in the long end. SONIA futures showing flat to +4.0, BoE-dated OIS pricing 18bp of easing through year-end and 28bp through February (vs. 17bp & 27bp ahead of the gilt open).

- Little of note on the UK calendar today, with tomorrow’s labour market report headlining the weekly schedule (expect our full preview of that release later today).

UK DATA: UK Labour Supply Growing "Sharply", Second Fastest Pace in Near 5 Years

- Ahead of tomorrow's headline labour market data, the release of the KPMG-REC Report on Jobs for July is also significant in providing any clue if a continually softening UK labour market - a necessity for another quarterly cut in November - is materializing.

- The report showed that the supply of labour continued to expand "sharply", with the rate softening only slightly from June for the second-fastest reading of that subcomponent since December 2020. Permanent placements meanwhile continue their "steep" decline due to "weak confidence around the economic outlook and greater pressure on budgets due to recent increases in payroll cost".

- Wage increases continued to remain on the softer side with the report noting that starting salary wage growth fell to its lowest level since March 2021.

- Vacancies also continued to fall, now at the fastest rate in three months in July.

- Overall, there is little in this report to provide any real positive signs. With the MPC continuing to place strong emphasis on the labour market (and non-headline ONS data) this is another dovish leaning report. Our preview of tomorrow's ONS data will be released later today.

USDCAD TECHS: Shallow Bounce Off Lows

- RES 4: 1.4111 High Apr 10

- RES 3: 1.4019 38.2% retracement of the Feb 3 - Jun 16 bear leg

- RES 2: 1.3920 High May 21

- RES 1: 1.3879 High Aug 1

- PRICE: 1.3763 @ 08:26 BST Aug 11

- SUP 1: 1.3557 Low Jul 03

- SUP 2: 1.3540 Low Jun 16 and the bear trigger

- SUP 3: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 4: 1.3473 Low Oct 2 2024

USDCAD remains subdued, despite the shallow bounce Friday following weaker-than-expected jobs data. The pair remains notably lower on the week on the back of last Friday’s USD weakness. Initial firm support has been breached at the 1.3737 20-day EMA, a break below which would resume the correction off the early August high at 1.3879. On the recent run higher, price traded through the 50-day EMA at 1.3744, which aided the rally. This week’s price action, however, has cancelled that bullish threat and returned focus lower. The 100-dma becomes a key pivot point at 1.3824 last.