EM ASIA CREDIT: MNI EM Credit Market Update - Asia

Asia EM USD sovereign and agency spreads are trading in a narrow range of -3bp to +4bp, with Indonesia outperforming (INDON 10/35s -3bp) in both credit and equity markets. Indonesia’s JCI equity index rose +0.7% and appears poised for a record close as investor confidence in the economy strengthens.

In company news, Jollibee Foods reported a solid Q2, with sequentially lower leverage (positive for spreads). Vista Land’s Q2 results highlighted continued weakness in the cash ratio, with onshore financing access seen as a key challenge (negative). Lenovo delivered strong results ahead of consensus, posting an upbeat outlook for the year (positive). There was no new USD issuance this morning.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS AUCTION: 5Y Climate Transition Auction Results

Japan sold 299.8 billion yen ($2.03 billion) of Climate Transition bonds due June 20, 2030. The bonds were sold at a price of 99.53, have a yield of 1.098% and will settle on July 16.

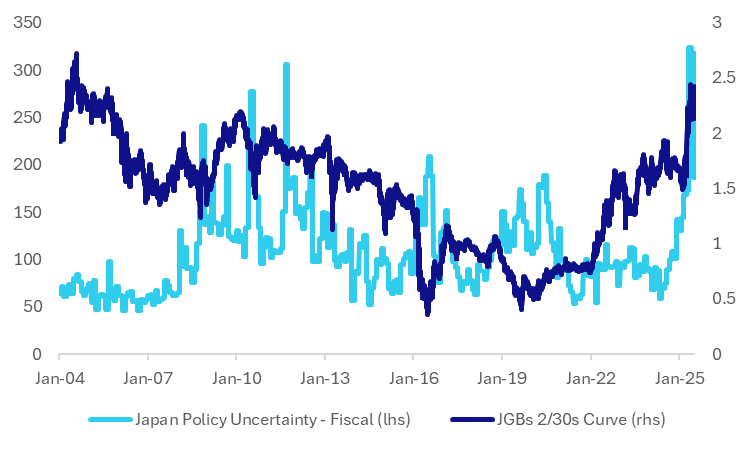

JAPAN: Long Dated Yield Surge Continues, With Election Driving Uncertain Outlook

As Japan's upper house elections approach (held July 20), focus remains on the relentless rise in longer-dated JGB yields. The 30yr is up a further +4bps today, last around 3.21%. This is a fresh high on record (since it was debuted in 1999, per BBG). The 10yr JGB yield was last near 1.60% with the 20yr around 2.64%. Concerns around fiscal slippage is a factor in the JGB sell-off. The 2/30yr JGB curve is at +241bps, just off recent highs and near multi-decade highs

- The chart below plots the JGBs 2/30s curve against a policy uncertainty index, related to fiscal policy. June saw fiscal policy uncertainty edge down per this metric (which is a monthly indicator), but it remains elevated by historical standards. The index ticker on BBG is EPUCJNFP <Index>.

- To be sure, there are lots of episodes where the JGB curve has been steep, whilst fiscal policy uncertainty is low. However, at the moment, the correlations between the two series are running at close to 80% (using the last 12 months as a sample window).

- A number of onshore media outlet are reporting that the ruling coalition is at risk of losing its majority with the upper house elections, helping fuel fiscal policy uncertainty, but with a skew towards a stronger fiscal impulse going forward.

- Rtrs adds: "All three of the leading opposition parties espouse some form of consumption tax cuts, with the populist, right-wing Sanseito party proposing a phasing out of VAT altogether. The policy has gained sway with the public as well: a recent poll by the Asahi newspaper showed 68% of voters thought a sales tax cut was the best way to cushion the blow from rising living costs."

- It quotes analysis from Barclays: "Barclays calculates that the rise in 30yr yields currently factors in about a three percentage-point cut to Japan's 10% consumption tax rate. "Even if the ruling parties retain their majority in the upper house, they would still be unable to pass budget bills, including the upcoming supplementary budget, without the cooperation of the opposition parties."

- Japan PM Ishiba has favoured cash handouts to provide cost-of-living relief so far, but it remains to be seen if this is sustained post the election result.

- Note on July 23rd we have 40y debt auction, as potentially the first litmus test after the election result.

Fig 1: JGBs 2/30yr Curve & Fiscal Policy Uncertainty Index

Source: Bloomberg Finance L.P./MNI

JGBS AUCTION: Poll: 5-Year Climate Transition JGB Auction

*JAPAN 5Y CLIMATE BOND SALE MAY HAVE CUT-OFF YIELD 1.1%: POLL - Bloomberg