EM ASIA CREDIT: MNI EM Credit Market Update - Asia

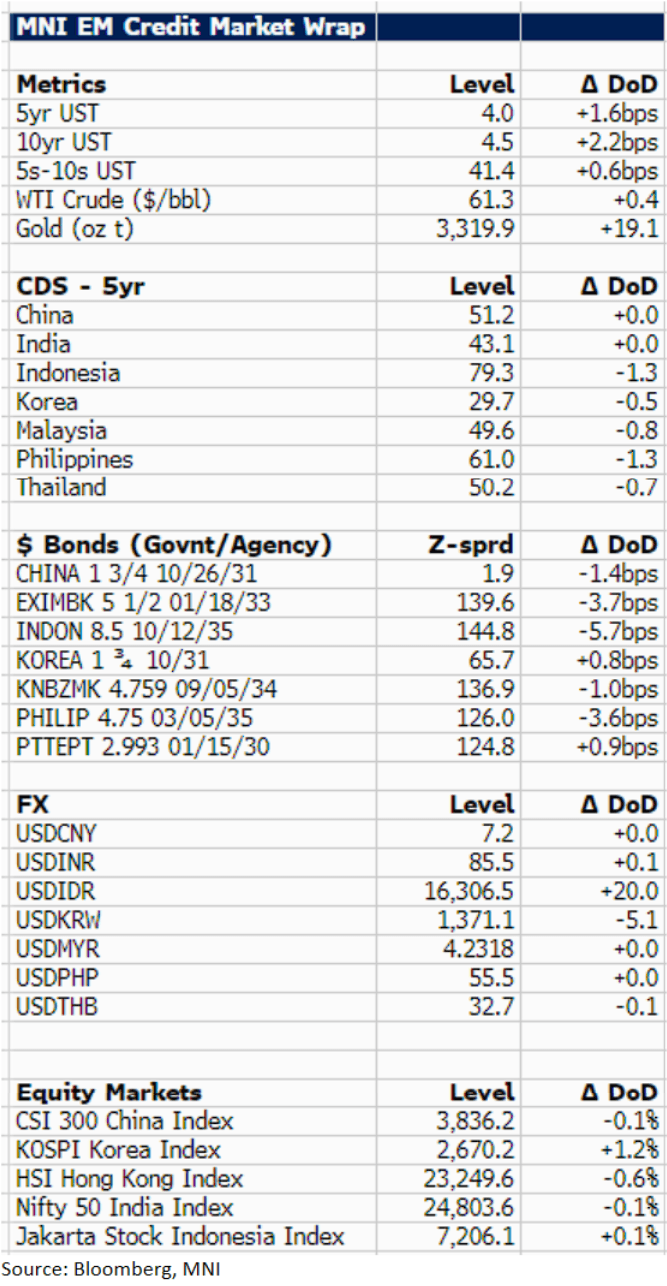

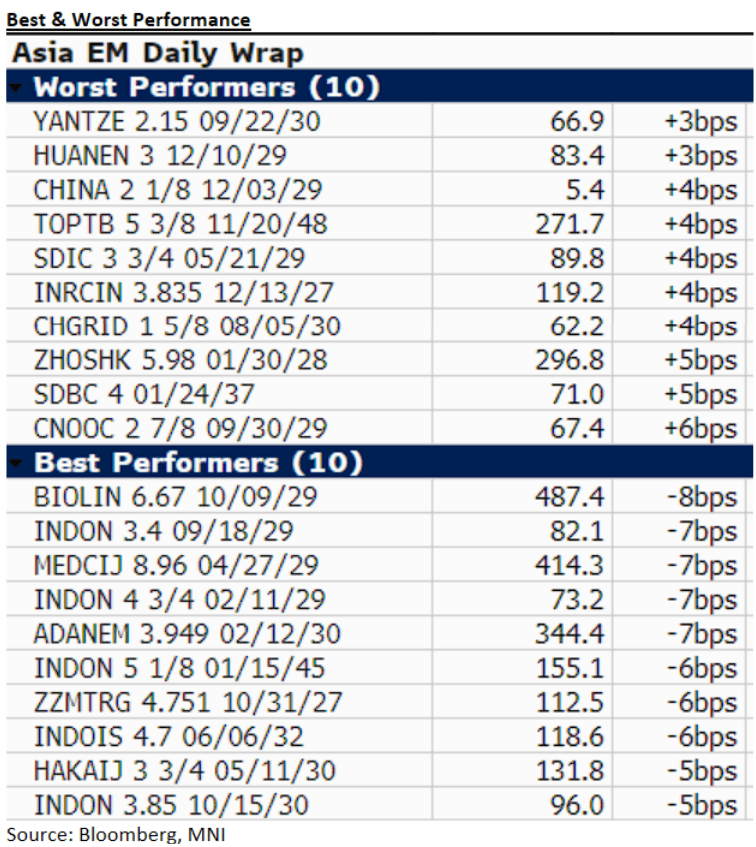

U.S. 10y treasury yields are 2bp higher today at 4.5%. Asia EM credit is mostly better, with govie/agency $ spreads tighter, Indonesia $ 10/35s the outperformer (-6bp). Korea is marginally weaker (Korea 10/31s +1bp), though not reflected in equities where the Korea KOSPI is +1%. In terms of newsflow, the Shanghai Construction 3y priced overnight at a yield of 4.6% (IPT 5.2%). Results from Malaysia's Axiata, MISC and RHB Bank were out, though ultimately not spread movers. This morning we had the debut $ deal from Malaysian bank, Affin Bank, with a $benchmark 5y deal. The IPT is T+ 135bp area, we estimate fair value at T+92bp.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: SFRM5 Blocked

Latest block trade lodged at 08:47:06 London/03:47:06 NY:

- SFRM5 1K lots blocked at 95.885, looks like a seller.

SWAPS: German ASWs A Little Narrower As Bonds Struggle

The weakness in outright bonds/uptick in European equities leaves German ASWs narrower early this week.

- Spreads vs. 3-month Euribor are 0.2-0.9bp narrower on the day, with Schatz leading the narrowing.

- However, the Schatz spread has failed to breach Friday’s low, while longer dated variants have traded through their respective Friday lows.

- Zooming out, a slightly more conducive risk tone has started to counter the widening theme seen in the second half of March/early April.

- A reminder that early March saw fresh cycle lows for long-dated spreads, following the German “whatever it takes” fiscal moment.

- That was before a lack of an immediate ramp up in issuance and the well-documented increase in global trade/U.S. policy uncertainty weighed on wider risk sentiment, helping drag ASWs away from lows.

- The impending, meaningful uptick in German issuance should continue to play into long end ASW spread dynamics over the medium-term (it should move back to the fore in H225/H126), although positioning and swings in broader risk appetite need to be accounted for as well.

SNB: Tweak to Threshold Factor is Neutral for MonPol Stance

SNB adjusts the remuneration of sight deposits, lowering the threshold factor from 20 to 18, effective as of 1st June 2025.

- This is considered neutral for monetary policy purposes, as it offsets increases to minimum reserve requirements.

Full SNB release here.

- What this effectively means is that more sight deposits are remunerated at a discount to the the SNB policy rate (rather than at the policy rate).

- The SNB is conducting this move in order to ensure monpol remains effective and the transmission mechanism isn't hampered by minimum reserve requirements rising (which they're expected to continue to do over the coming three years).

- The move follows recent previous adjustments to reduce the threshold factor that were implemented in October 2024 and February 2025.

- As such, no notable response in EUR/CHF, still below the overnight high of 0.9438.