MNI Credit Sector Overview: Bank Consumer Delinquencies

EXECUTIVE SUMMARY

Despite the angst about consumer health and bank asset quality, Regional and other banks in the IG benchmark have reported largely benign consumer credit metrics relative to pre-pandemic norms of 2018/19. This has generated both relief and disbelief, given that consumers remain pressured by inflation and a slowing jobs market.

We examine delinquency trends from consumer lenders including banks we cover, as well as the Federal Reserve’s aggregated data from all commercial banks for a fuller picture. Although parts of the broader data reveal concerning trends, we find these are not in areas where investment-grade banks typically have exposure.

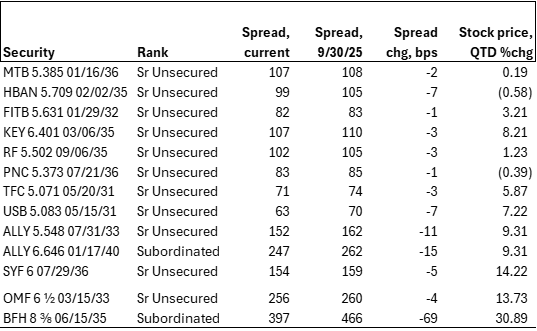

Bond spreads for this group have mostly reflected this, generally performing in-line with the benchmark recently, even on days when the regional bank equity index was volatile. Bread Financial is a notable outlier, with the BHF 8.375 2035 subs rallying ~70bps QTD, despite delinquencies that having been edging above pre-pandemic levels. Likewise, ALLY 6.646 2040 subs have outperformed despite delinquencies that exceed prepandemic levels.

Part I.

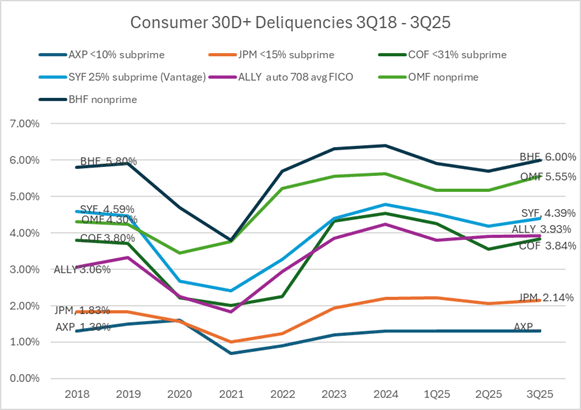

The chart above shows credit card and other consumer delinquency rates by issuer. We’ve included nonbanks like OneMain Financial (OMF) and Bread Financial Holdings (BHF) to capture the nonprime segment.

Delinquencies have been rising since the post-pandemic lows of 2021, but overall are still within 2018-19 pre-pandemic ranges. However, there are visible differences in the slope of rise, and at the high FICO end, American Express (AXP) delinquencies tracked the most muted rise, ending with a 3Q25 rate of 1.3% that’s flat to 2018-19.

Further down the FICO spectrum, Capital One (COF) and Synchrony (SYF) delinquencies spiked in 2024 to surpass 2018-19 levels by 10%+, but have since settled at 2018-19 levels of 3.85 and 4.4%. ALLY retail auto delinquencies saw a steeper rise, with its 3.93% about a quarter higher than pre-pandemic. Notably, this is the reverse of the Manheim used auto price index’s ~25% decline from its 2022 peak. At the non-prime end of spectrum, OMF and BHF have seen the steepest delinquency rises with OMF’s 5.55% now a third higher than pre-pandemic levels.

Like our sample group, most Federal Reserve Category III-IV Regional banks have continued to report fairly benign consumer delinquencies. For a more comprehensive picture, though, we turn in Part II to the Federal Reserve’s consumer delinquency data for all commercial banks.

Part II.

Here we look at card delinquency data that Federal Reserve aggregates from the commercial banks under its supervision to identify patterns in the broader universe.

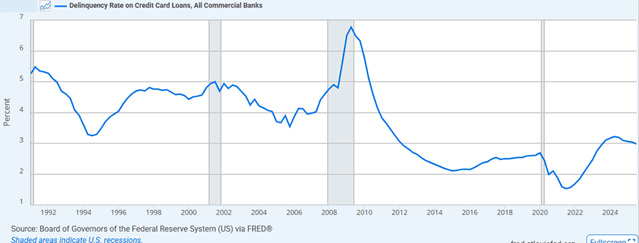

We start with this chart of 1Q1991 – 2Q2025 ‘Delinquency Rate on Credit Card loans– All Commercial Banks’. The broad group shows a pattern similar to that of the banks in Part I, with delinquencies rising from 2021 lows, but within 2018-19 range. It also looks benign compared to the full 20+ year range.

This next chart excludes the top 100 banks. Delinquencies here are more volatile, with a steeper rise since 2021, and are approaching a 20+ year high. The banks in the Barclays investment-grade index are all are Federal Reserve Category I-IV banks and thus too large for this subset. For context, though, the top 5 card issuers ( JPM, AXP, Citi, Capital One, Bank of America) have a combined 2/3rds of US credit card market share.

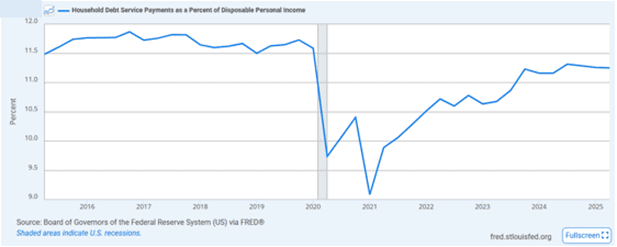

Lastly, we turn to overall consumer health by looking at debt service to income to assess consumer debt capacity. We find that the consumer is not any worse off than pre-pandemic periods though there are some risks that bear monitoring. Household Total debt service (ie, consumer + mortgage) to disposable income looks benign, stabilizing at levels modestly below pre-pandemic levels.

Unemployment, however, has ticked up YTD to 4.4%, moderately exceeding the 3.6-4% range in 2018-19, and should labor markets continue weakening that would erode the modest buffer in household debt servicing. And recent changes in student loan payment policies could also pressure it.

Part III. 4QTD Bond Spreads & Equity moves

Bank spreads have mostly moved within +/- 10 bps, fairly in line with benchmark. Nonprime, high-yield lender spreads have moved more, unsurprisingly given their higher beta. We note that Bread Financial (BFH) has rallied disproportionately on recent rating upgrades and would be cautious given their exposure to riskier borrowers in a slowing economy. We also point out that ALLY spread compression seems unjustified given its delinquency rates are now 25%+ above 2018-19 levels.