BOJ: MNI BoJ Preview - June 2024: Steady Policy Rate, Focus On JGB Purchases

EXECUTIVE SUMMARY

- At this week’s meeting, we anticipate that the BoJ will maintain its policy rate settings (keeping the target for the overnight uncollateralized call rate at 0-0.1%) on June 14, in line with consensus. Recent economic data around prices and growth suggest this approach.

- Nevertheless, the trend towards normalisation continues. The BoJ's sensitivity to foreign exchange rates has also shifted in recent months. We expect a generally hawkish tone at the meeting, indicating the possibility of additional policy tightening in subsequent meetings, possibly as soon as July.

- The focus for the June meeting will likely be on balance sheet policy and the future pace of JGB purchases.

- It is uncertain whether the BoJ will revise its JGB purchase directive this week. However, it seems increasingly likely that the Policy Board will introduce new guidelines, as suggested by recent reports indicating a potential discussion on publishing a more specific schedule for reduced JGB purchases as early as the June meeting

- The Reuters poll showed that 63% of economists predict the BoJ will decide to start reducing bond buying at the June meeting, up from 41% in May.

- Regardless of the decision at this week’s meeting, we expect the BoJ to proceed cautiously and gradually in both hiking the policy rate and adjusting JGB purchases.

- Full preview here:

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: Asian Equities Mixed, NZ Inflation Expectations Fall

Asian equity markets are mixed today, Taiwan equities are the top performing market led by the semiconductor sector. There isn't much on the data calendar today, earlier we have NZ Food prices which increased from the month prior and Australia's NAB business survey's which show business conditions had fallen from the month prior.

- Japanese equities are little changed today, the real estate sector is the worst performing. There has been little in the way of headlines out of the region, with government officials staying surprising quiet on the currency so far today, the yen continued to slip on Friday and we currently trade little changed on the day at 155.75. The Nikkei 225 is up 4.10% from the lows on Apr 19th but has failed to break back above the 20 & 50-day EMAs and trade unchanged today, the Topix has performed slightly better over the same period up 5% and holds above all moving averages, however trades unchanged today.

- South Korean equities are lower today, earlier April household spending rose to KRW1,103.6T from KR1098.5t in March. The Kospi continues to comfortably hold above all major moving averages, while the RSI is holding above 50 and MACD indicator is holding steady, signaling buyers still remain in control, the index is down 0.32% today.

- Taiwan equities are the top performers today, flows turned positive again on Friday as investors continue buying up semiconductor stocks. It's a very quiet week on the data front for Taiwan with nothing scheduled. The Taiex opened at new all-time highs this morning, however we trade just off those levels now, up 0.83%.

- Australian equities are lower today, as investors await the federal budget that will be released on Tuesday, while earlier NAB's monthly business survey's showed that conditions eased in April, with trading, profitability and employment all back around their long-term averages. The ASX200 is down 0.25%.

- Elsewhere in SEA, New Zealand equities are down 1% with the 1yr inflation expectation falling to 2.73% from 3.22% and the 2yr falling to 2.33% from 2.50%, Indonesian equities have returned from their break and are trading up 0.10%, Philippines equities are up 1%, Malaysian equities up 0.15% and Indian equities up 0.45%

AUD: Aussie Continues Trending Lower On Weaker Risk Sentiment

Aussie continued its underperformance from Friday during today’s APAC trading driven by a risk off tone. Data on Saturday showed weaker-than-expected China lending and continued soft inflation. AUDUSD was trending lower before the April NAB survey showed a weakening in business conditions. The pair is off its low of 0.6586 but is still down 0.1% at 0.6596. The USD index is flat.

- AUDJPY is down 0.1% to 102.76 after a high of 102.96 earlier. AUDNZD is up 0.2% to around 1.0985 rising on data showing a drop in NZ inflation expectations. AUDEUR is 0.1% lower at 0.6125 and AUDGBP little changed at 0.5267.

- NAB’s measure of business confidence was stable at 1 in April but conditions eased further to 7 from 9. The main activity components moderated with employment now below the historical average, while April price/cost components lower compared with Q1. Aussie looked through the data.

- Equities are mixed with the ASX down 0.3% and KOSPI -0.3% but CSI 300 up 0.1% and Hang Seng +0.6% and Nikkei flat. The S&P e-mini is moderately lower. Oil prices are down again with WTI -0.2% at $78.11/bbl. Copper is up 0.1% and iron ore is around $115.50-116/t.

- Later the Fed’s Mester and Jefferson discuss central bank communications. In terms of data there is just US NY Fed 1-year inflation expectations for April. The Eurogroup meeting is being held and the ECB’s Buch is scheduled to speak.

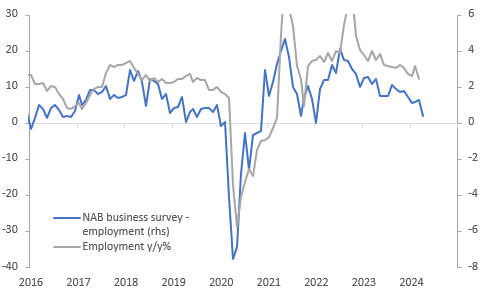

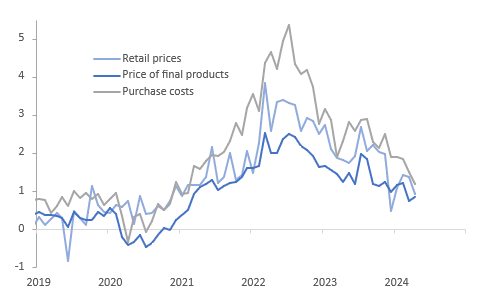

AUSTRALIA DATA: April Price/Cost Pressures Softer Than Q1

NAB’s measure of business confidence was stable at 1 in April but conditions eased further to 7 from 9, only slightly above the series average. Confidence has been fairly steady around 1 through 2024 but conditions have eased 3 points since December and 18 points since the September 2022 peak. The main activity components eased further with employment now below the historical average, while April price/cost components moderated compared with Q1.

- Employment fell 4.5 points to 1.9, which is still signalling positive labour demand but at a lot slower pace than it had been previously. It was the lowest reading since January 2022.

Source: MNI - Market News/Refinitiv

- Forward looking orders fell to -7.2 from -1.4, the lowest since the Covid-impacted August 2020. NAB says that the deterioration was due to large drops in mining, manufacturing and construction, while retail and wholesale are also negative.

- On a more positive note, capacity utilisation was unchanged and investment high.

- Labour costs moderated to 1.5% over 3-months from 1.7%, the lowest since September 2021 but still above the post-2000 average. Purchase costs eased to 1.2% from 1.5%, in line with average.

- Prices of final products rose 0.9% over 3-months up from March’s 0.7% but retail moderated 0.5pp to 0.9%. Both are below the Q1 average though signalling that the start of Q2 saw a moderation in price pressures.

- Services are facing better business conditions while retail are the “most concerning”.

- See NAB survey here.

Source: MNI - Market News/Refinitiv