MNI BoC Preview-July 2025: Data Calls For Further Patience

Jul-29 2025 16:38By: Tim Cooper

Canada

Hidden PDF

EXECUTIVE SUMMARY:

- Data developments since the June meeting mean the Bank of Canada will maintain the overnight rate target steady at 2.75% for a third consecutive meeting on Wednesday.

- Better-than-expected labour market data and stubbornly high core inflation, combined with continued uncertainty over the US-Canada trade dispute, give the BOC impetus to wait until its next meeting in September before committing to further moves.

- While the BOC is likely to retain its easing bias, judging from market pricing, the question now is whether the BOC’s easing cycle is at an end after 225bp of cuts through March.

- We note that while most analysts still expect at least one further cut, median expectations of the terminal overnight rate as tracked by MNI have crept up to 2.25% from 2.125% since prior to the June meeting.

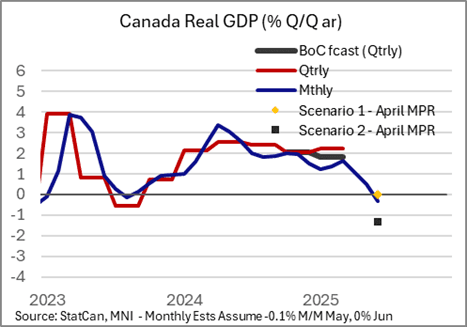

- The latest Monetary Policy Report is likely to include two tariff-related scenarios as in the previous round, with a less negative estimate for Q2 GDP and slightly higher core inflation.

- The policy statement should reflect this better-than-expected economic activity evolution as well, but once again we do not expect any firm forward guidance.