MNI ASIA OPEN: US Data Continues To Soothe Tariff Nerves

MNI (NEW YORK) -

EXECUTIVE SUMMARY

- MNI INTERVIEW: Risk Rising Of Sub-2% ECB Rates-Malta's Demarco

- US DATA: Consumer Confidence Surprisingly Bounces, Helped By China Trade Deal

- US DATA: Core Durable Goods Giving Back Q1 Gains, But Sharp Q2 Dropoff Not Clear

- JGBS: MOF Holding Primary Dealers Meeting June 20: Nikkei

NEWS:

JAPAN (MNI/Nikkei) Nikkei reports: "Japan's Finance Ministry will hold a meeting for primary dealers of Japanese government bonds on June 20, Nikkei has learned, and what may be on the agenda is spurring speculation over cutbacks to the ultralong-term bond supply." That's of potentially heightened interest given Reuters earlier reporting the MOF will consider skewing the composition of its current issuance programme away from super-long-end instruments (which saw a strong JGB rally overnight).

ECB( MNI INTERVIEW): Uncertainty surrounding international trade increases the risk of lower growth and well-below target inflation over the medium term which could justify European Central Bank rates below 2%, Bank of Malta acting Governor Alexander Demarco told MNI. “If headline inflation in the medium term is expected to remain persistently well below 2% then it is more likely that there is room for interest rates to fall below 2%,” he said in an interview, stressing that this would also depend on medium-term inflation expectations remaining well-anchored and on other key indicators “behaving in a manner conducive to the attainment of our price stability objective.”

ECB (MNI BRIEF): The European Central Bank is on the path to 2% inflation, but high levels of economic and geopolitical uncertainty, coupled with more sensitive inflation expectations, mean nothing has been decided ahead of the ECB’s next decision, Joachim Nagel said in a speech on Tuesday. (see MNI SOURCES: Risks Tilt To Downside As ECB Mulls Path Below 2% )

CANADA (MNI): King Charles played up Canada's sovereignty in a Throne Speech in Ottawa Tuesday, backing Prime Minister Mark Carney's rejection of Donald Trump's comments about using economic force to bring trade concessions followed by turning America's northern neighbor into the 51st State. "The Government will discharge its duty to protect Canadians and their sovereign rights, from wherever challenges may come at home or abroad," according to the text of the King's speech to Parliament.

HUNGARY (MNI NBH WATCH): The National Bank of Hungary left key interest rates unchanged on Tuesday, with the disinflationary effects of lower oil prices, government profit-margin caps and lower telecoms and bank prices seen offset by strong market services prices and the upward effect on inflation expectations of possible trade tariffs. (See MNI EM NBH WATCH: Another Rates Hold As Expectations Stay High) As expected, base rate was left unchanged at 6.5%.

BRAZIL (MNI INTERVIEW): The Brazilian government’s spending freeze in its 2025 budget announced last week was a positive sign on the fiscal front, despite market “noise” created by an increase in the Tax on Financial Transactions (IOF), the director at the Independent Fiscal Institution (IFI), an independent public body, told MNI.

US TSYS: Bull Flattening In Return From Long Weekend

The cash Treasuries curve bull flattened Tuesday in the return to trading after the Memorial Day weekend.

- Global core FI was roundly boosted by soaring long-end JGBs on an overnight Reuters report that the Japanese finance ministry was considering shifting its issuance profile away from long-dated paper.

- Data broadly confirmed the narrative of US economic stabilization, with durable goods orders softer but not necessarily falling off a cliff in April, and Conference Board consumer confidence surprisingly bounced in May (though the so-called labor differential weakened in a possible warning sign for the labor market).

- In supply, the 2Y Note was well digested (1bp trade-through was the best since February), helping consolidate Treasury gains through the afternoon session.

- The June/September futures roll picked up where it left off last week, with most contracts now around two-thirds complete.

- Latest cash levels: The 2-Yr yield is down 1.9bps at 3.9723%, 5-Yr is down 5.1bps at 4.0298%, 10-Yr is down 7.1bps at 4.4397%, and 30-Yr is down 9.2bps at 4.9459%. The Jun 25 T-Note future is up 12/32 at 110-14.5, having traded in a range of 109-24.5 to 110-18.

- Wednesday's calendar includes more regional Fed surveys (Richmond services/manufacturing, Dallas services) and an appearance by FOMC's Kashkari, with supply including 2Y FRN and 5Y Note. We then get the minutes of the May FOMC meeting in the afternoon.

MARKET SNAPSHOT: Below gives key levels of markets in afternoon NY trade:

- DJIA up 693.64 points (1.67%) at 42298.64

- S&P E-Mini Future up 110.75 points (1.9%) at 5928

- Nasdaq up 417.7 points (2.2%) at 19154.56

- US 10-Yr yield is down 7.3 bps at 4.4377%

- US Jun 10-Yr futures (TY) are up 12.5/32 at 110-15

- EURUSD down 0.005 (-0.44%) at 1.1337

- USDJPY up 1.41 (0.99%) at 144.26

- WTI Crude Oil (front-month) down $0.59 (-0.96%) at $60.94

- Gold is down $38.49 (-1.15%) at $3305.44

Prior European bourses closing levels:

- EuroStoxx 50 up 20.12 points (0.37%) at 5415.45

- FTSE 100 up 60.08 points (0.69%) at 8778.05

- German DAX up 198.84 points (0.83%) at 24226.49

- French CAC 40 down 1.34 points (-0.02%) at 7826.79

US 10YR FUTURE TECHS: (M5) Corrective Bounce

- RES 4: 112-20+ High May 1 and a bull trigger

- RES 3: 112-01+ High May 2

- RES 2: 111-22 High May 7

- RES 1: 110-21+ High May 16 and a key near-term resistance

- PRICE: 110-15 @ 17:16 BST May 27

- SUP 1: 109-13 Low May 22

- SUP 2: 109-08 Low Apr 11 and key support

- SUP 3: 108-26+ 76.4% retracement of the Jan 13 - Apr 7 bull cycle

- SUP 4: 108-21 Low Feb 19

A bear cycle that started early May in Treasury futures remains in play for now, and short-term gains are considered corrective. The recent breach of 110-01+, 76.4% of the Apr 11 - May 1 bull leg, strengthened a bearish theme and has exposed key support at 109-08, the Apr 24 low and a bear trigger. Key near-term resistance has been defined at 110-21+, the May 16 high. A clear break of this level is required to signal a potential reversal.

OVERNIGHT DATA

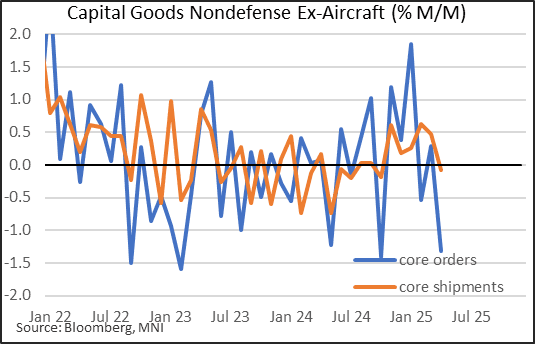

US DATA: Core Durable Goods Giving Back Q1 Gains, But Sharp Q2 Dropoff Not Clear

April's Advance Report on Durable Goods Manufacturers' Shipments Inventories and Orders was broadly weak, with headline durable goods orders contracting sharply (-6.3% M/M) as expected in a reversal of March's strong gains (+7.6%), but with capital goods orders coming in on the weak side.

- Ex-transport orders for durables rose 0.2% (-0.2% prior), illustrating the high sensitivity in the headline figure to aircraft orders (Nondefense aircraft and parts fell 51.5% M/M after +158.5% in March), while the closely-watched core (nondefense, ex-aircraft) capital goods orders fell 1.3% (+0.3% prior).

- This is a slightly more complex read-through for results vs analyst consensus on monthly growth - the Census Bureau in mid-May re-benchmarked all of the data going back to 2012, meaning that March's "final" figures were revised (eg durable goods orders looked like a substantial downward revision to 7.6% vs 9.2% in March's report, but this was only up 0.1pp from 7.5% in the latest benchmark release for March).

- But the broader readthrough is one of weakness. the fall in core capital durable goods was the biggest in 6 months, and the 2nd most in 26 months. This brought down momentum, with the 3M/3M annualized rate at 2.2% in April, after 9.2% in March; on a Y/Y NSA basis, core capital goods orders are up just 0.6%. Core shipments fell 0.1% for the first decline in 6 months, and while still running at a 4.6% quarterly clip, this is merely lagging the strong orders in earlier months.

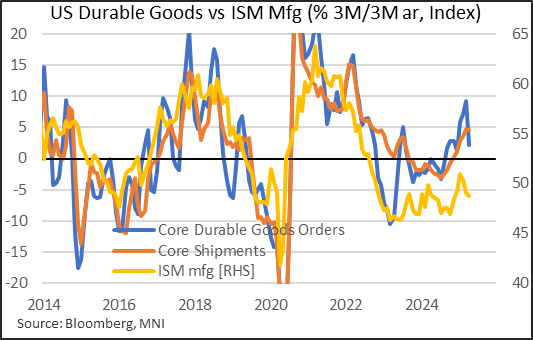

- Of course, tariffs (and front-running thereof) have to be mentioned as a possible catalyst for the pullback - for instance, motor vehicles and parts orders fell 2.9% M/M after strong growth in both March and February. And the orders numbers mirror the ISM manufacturing survey showing new orders have contracted for three consecutive months amid a headline index below 50.0 in the last two (Mar-April), with tariffs a key theme.

- But it's not so clear-cut looking at the underlying durables data: for example, computers and electronic products orders grew in April after contracting in March, while machinery and fabricated metal products orders also accelerated, suggesting that business fixed investment isn't showing clear evidence of falling off a cliff in Q2.

- Going forward it looks as though Q1 was indeed illusory in terms of underlying upside momentum for equipment investment, but it's not yet clear whether Q2 activity - while clearly slowing - will see quite as dramatic a drop-off as suggested by sentiment indicators.

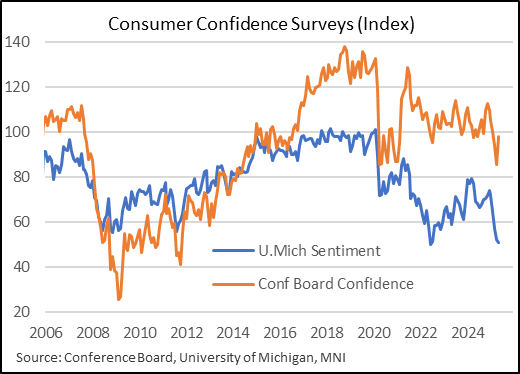

US DATA: Consumer Confidence Surprisingly Bounces, Helped By China Trade Deal

- The Conference Board consumer survey saw much stronger than expected consumer confidence in May at 98.0 (cons 87.1) after a marginally downward revised 85.7 (initial 86.0) in April.

- The improvement was led by the expectations index (from 55.4 to 72.8) although the present situation also improved (from 131.1 to 135.9).

- Whilst an improvement in overall confidence, the 98.0 is still below the 104.5 averaged in 2024 for example, having recently peaked at 112.8 in Nov 2024 in the month of the presidential election.

- The press release on how US-China de-escalation on May 12 shaped results: "About half of the responses were collected after the May 12 announcement of a pause on some tariffs on imports from China.”

“The rebound [in confidence] was already visible before the May 12 US-China trade deal but gained momentum afterwards. The monthly improvement was largely driven by consumer expectations as all three components of the Expectations Index—business conditions, employment prospects, and future income—rose from their April lows." - Recall that the separate U.Mich preliminary survey for May was conducted Apr 22-May 13, “two days after the announcement of a pause on some tariffs on imports from China." It had added that "many survey measures showed some signs of improvement following the temporary reduction of China tariffs, but these initial upticks were too small to alter the overall picture”.

- As noted below, a further decline in the labor differential offered a more negative take on what was otherwise a reasonable report.

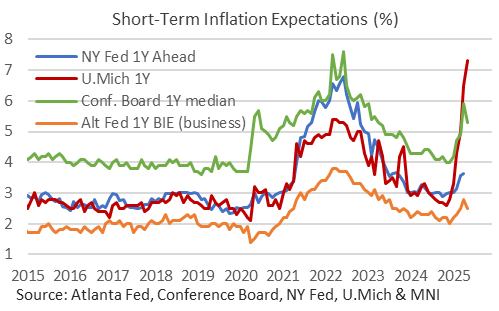

US DATA: Conference Board Inflation Expectations Edge Lower In May

- Within the Conference Board consumer survey, 1Y inflation expectations dialled back in May after the further push higher in April.

- With a survey up to May 19 as opposed to May 13 in the preliminary U.Mich equivalent, it gives an idea of the possible direction of travel when the finalized U.Mich survey for May is published this Friday.

- The average response for the 1Y ahead eased to 6.5% in May from 7.0% in April whilst the median fell back to 5.3% from 5.9%.

- Putting these figures into perspective though, excluding April the latest average would still be the highest since Jan 2023 and the median the highest since Apr 2023.

- The modest ease in inflation expectations echoed a finding from the Atlanta Fed’s Business Inflation Expectations survey from last week.

US DATA: Conf. Board Labor Differential Weakens Despite Confidence Beat

The labor differential within the Conf. Board consumer survey was in firm contrast to the surprise strength in the headline metrics.

- The differential fell further to 13.2 from a downward revised 13.7 (initial 15.1) for its lowest since Sep 2024 and before that Mar 2021.

- The small deterioration on the month came from jobs being perceived as hard to get rising from 17.5% to 18.6%, a joint high with Sep 2024 and last seen higher in Feb 2021.

- That chimes a bit more with the relatively small increase in the overall present situation reading (135.9 after 131.1) compared to the expectations index jumping from 55.4 to 72.8.

US DATA: Texas Manufacturing Activity And Prices Steadier In May

May's Texas Manufacturing Outlook Survey showed an improvement from April and overall steady activity in the month, with the production index, "a key measure of state manufacturing conditions... indicating flat output this month after modest growth in March and April", per the Dallas Fed.

- Indeed, production fell 4.2 points to 0.9. But the general business activity index rose 20.5 points to -15.3, a three-month best, with 6-month ahead production up 16.3 points to 31.1, highest in 4 months. New orders picked up 11.3 points to -8.7, which apart from March's 29-month low would have still been the weakest since November 2024. Employment rose 7 points to 3.5.

- From an inflation perspective, prices paid pulled back 7.7 points to 40.7, with prices received up 0.2 to 15.1 - both still elevated. There was a bit more of a deceleration in 6-month ahead expectations, with prices paid down 7.8 points (39.8, 5-month low) and received ticking 1.4 points lower (28.2).

- The majority of anecdotal comments in the Dallas report mentioned "tariffs", mostly in a negative way though a couple respondents noted that confidence would improve if and when deals were struck. Indeed there was scarce mention of the May 12 US-China tariff climbdown (survey data were collected May 13–21) and even then the confidence seemed tentative (a firm in Computer and electronic product manufacturing: "I would say the uncertainty has decreased in the very short term (up to 90 days) based on the U.S.–China tariff rollback").

- The most tangible impact on the survey was in the 34.4 point drop in the Outlook Uncertainty index, to 12.7.

- We get the Richmond Fed's manufacturing survey Wednesday, which will help shore up the degree to which confidence improved after the May 12 tentative "deal". Improvements so far have been seen in Philadelphia, Dallas, and Kansas, with Chicago activity and NY Fed's Empire State current conditions indices lower vs April.

US DATA: A Surprising, And Rare, Dip In House Prices In March

House prices were surprisingly soft back in March, with both the FHFA and S&P CoreLogic 20-city measures recording their first simultaneous seasonally adjusted decline since Aug 2022. It comes as existing home sale relative supply has recently increased to its highest for the time of year since 2016 although these FHFA /S&P Corelogic series still see reasonable Y/Y increases.

- FHFA house prices surprisingly dipped -0.05% M/M (sa, cons 0.1%) in March after a downward revised 0.02% (initial 0.14%), for its first monthly decline since Aug 2022.

- S&P CoreLogic 20-city -0.12% M/M (sa, cons 0.2%) in March after an unrevised 0.40% M/M, its first monthly decline since Jan 2023.

- Recent run rates are still reasonable considering the build in relative supply of inventories to sales in both existing and new home sales data. Whilst new home sales relative supply has been high for some time, existing home sale inventory has recently increased with the 4.0 months of sales back in March the highest for that month since 2016, a trend that held more recently in April at 4.4 months.

- The S&P Core Logic 20-city measure is still up 4.1% Y/Y, and with a 3m/3m run rate a touch stronger at 4.4% annualized, although the FHFA series is a little softer at 3.7% Y/Y and 3.1% 3m/3m annualized.

- A reminder that these metrics are 53% (S&P) and 55% (FHFA) higher than pre-pandemic levels.

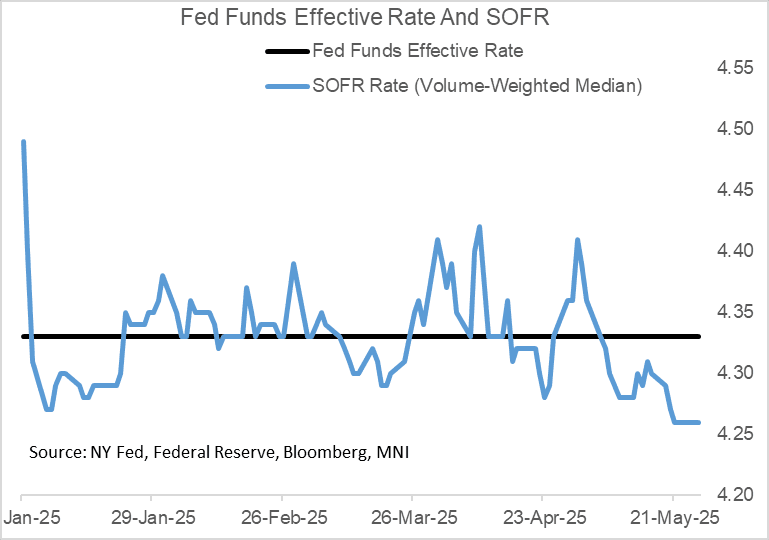

US TSYS/OVERNIGHT REPO: SOFR Remained Subdued Last Week, But Should Pick Up

Secured rates remained soft on Friday, with SOFR unchanged vs Thursday at 4.26%. SOFR was softer than most had anticipated last week, with GSE cash inflows appearing to weigh down rates for an extended period, but that effect should start to dissipate with rates picking up this week.

- Upside pressures will be exacerbated by Friday's month-end dynamics, with Thursday seeing $46B in net new cash raised via coupon auction settlements, though Wednesday's rates could be subdued in the meantime by $29B in net bill paydown.

- As usual, Fed funds rates remained at 4.33%.

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 4.26%, no change, $2542B

* Broad General Collateral Rate (BGCR): 4.26%, no change, $1048B

* Tri-Party General Collateral Rate (TGCR): 4.26%, no change, $1013B

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 4.33%, no change, volume: $123B

* Daily Overnight Bank Funding Rate: 4.33%, no change, volume: $305B

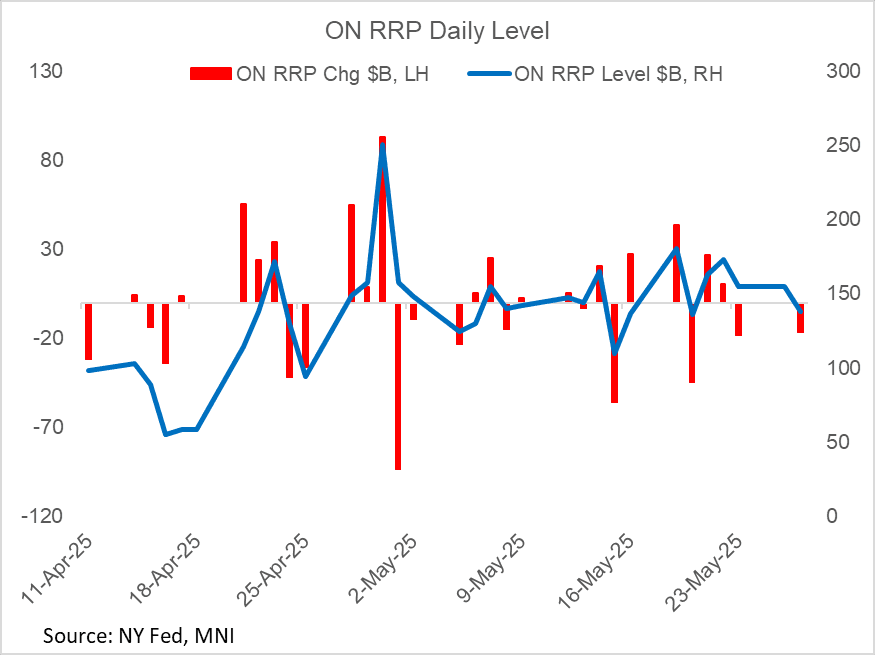

US TSYS/OVERNIGHT REPO: Reverse Repo Takeup Dips, Within Recent Ranges

Takeup of the Fed's overnight reverse repo facility fell $16.7B to $138.1B Tuesday, in the return from the Memorial Day weekend.

- That's the lowest level since May 20, with the pullback in facility usage since the start of last week ($180B high) potentially reflecting a pullback of GSE cash from markets.

- Takeup is next expected to rise at the end of the week, reflecting end-month dynamics.

BONDS: EGBs-GILTS CASH CLOSE: Long-Ends Outperform

European yields were mixed Tuesday, with long-end bonds outperforming.

- Yields dropped in early trade following a large Japanese government bond rally overnight, with longer-end US and German instruments outperforming for the day.

- From the morning lows though, yields edged higher through the session as equities gained.

- In particular, Gilt yields caught up after Monday's holiday with a broader risk-on sentiment coming out of the weekend, following US President Trump's decision to postpone new tariffs on the EU (from an originally announced June 1 date) pending talks.

- French flash May inflation was much softer than expected, helping EGB short-end outperform the UK; the EC's May confidence surveys saw an improvement in May following the US/China tariff de-escalation (but pre-EU/US back-and-forth).

- In ECB-speak, Lane noted the ECB will cut rates further if it sees signs of further falling inflation; Nagel didn't explicitly lean towards a June ECB cut or hold.

- The German and UK curves both curve twist flattened. EGB periphery / semi-core spreads were flat/slightly tighter.

- Wednesday's calendar includes an appearance by BOE's Pill, and the ECB CPI expectations survey.

Closing Yields / 10-Yr EGB Spreads To Germany:

- Germany: The 2-Yr yield is up 0.9bps at 1.791%, 5-Yr is down 0.6bps at 2.093%, 10-Yr is down 2.8bps at 2.532%, and 30-Yr is down 6.3bps at 3.002%.

- UK: The 2-Yr yield is up 3.7bps at 4.02%, 5-Yr is up 2.2bps at 4.152%, 10-Yr is down 1.5bps at 4.666%, and 30-Yr is down 4.5bps at 5.435%.

- Italian BTP spread down 0.9bps at 98.5bps / Portuguese down 0.9bps at 49.4bps

FOREX: USD Index Trades with More Constructive Tone, JPY Underperforms

- The greenback trades on a firmer footing on Tuesday alongside the step lower for long-end core yields and the prevailing optimism for major equity benchmarks. As noted, long-end JGBs are outperforming after Reuters sources suggested the MOF will consider skewing the composition of its current issuance programme away from super-long-end instruments.

- This dynamic has helped USDJPY extend its intra-day recovery to around 1.65% on the session, narrowing the gap to the initial resistance zone at 144.40, last Thursday’s high and the 20-day EMA. Above here, the 50-day EMA currently intersects at 145.73.

- NZD and AUD also sit among the worst performers in G10 on Tuesday, shrugging off the more optimistic tone for global equities and taking its cues from the broader dollar rebound. Today’s 0.95% selloff has seen NZDUSD gravitate back below 0.6000 handle, as a cluster of US election related highs between 0.6025/38 continue to cap the topside for the pair.

- GBPs more modest 0.45% dip lower stands out in G10, and underpins the prevailing bullish/resilient theme for GBPUSD. The break of 1.3444 (Apr 28 / 29 high) remains significant here, confirming a resumption of the technical uptrend. This allowed the pair to print fresh cycle highs of 1.3593 on Monday, narrowing the gap substantially to 1.3605, a Fibonacci retracement. Moving average studies continue to highlight a dominant uptrend. First support lies at 1.3351, the 20-day EMA.

- Spillover USD buying is, in turn, meeting a weaker EUR after this morning's soft French CPI print and the resultant losses for EUR/USD are closing the gap with the 1.13 handle support and sizeable option strikes set to roll off at tomorrow's NY cut (which also happens to be value date month-end).

- Australia CPI and the RBNZ (expected to cut 25bp to 3.25%) decision will take focus on Wednesday. Later in the session, the FOMC minutes are also scheduled.

DATA/EVENTS CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 28/05/2025 | - | Reserve Bank of New Zealand Meeting | ||

| 28/05/2025 | 0130/1130 | *** | CPI Inflation Monthly | |

| 28/05/2025 | 0130/1130 | *** | Quarterly construction work done | |

| 28/05/2025 | 0200/1400 | *** | RBNZ official cash rate decision | |

| 28/05/2025 | 0600/0800 | ** | Retail Sales | |

| 28/05/2025 | 0600/1400 | ** | MNI China Money Market Index (MMI) | |

| 28/05/2025 | 0645/0845 | ** | PPI | |

| 28/05/2025 | 0645/0845 | *** | GDP (f) | |

| 28/05/2025 | 0645/0845 | ** | Consumer Spending | |

| 28/05/2025 | 0700/0900 | ** | Economic Tendency Indicator | |

| 28/05/2025 | 0755/0955 | ** | Unemployment | |

| 28/05/2025 | 0800/0400 | Minneapolis Fed's Neel Kahkari | ||

| 28/05/2025 | 0800/1000 | ** | ECB Consumer Expectations Survey | |

| 28/05/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 28/05/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 28/05/2025 | 1400/1000 | ** | Richmond Fed Survey | |

| 28/05/2025 | 1430/1030 | ** | Dallas Fed Services Survey | |

| 28/05/2025 | 1500/1600 | BOE's Pill on monetary policy panel at Austria National Bank / SUERF | ||

| 28/05/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 28/05/2025 | 1700/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 28/05/2025 | 1800/1400 | FOMC Minutes | ||

| 28/05/2025 | 1800/1400 | *** | FOMC Minutes | |

| 28/05/2025 | 0000/2000 | New York Fed's John Williams | ||

| 29/05/2025 | 0130/1130 | * | Private New Capex and Expected Expenditure |