MNI ASIA OPEN: Tsy Curves Twist Flatter Ahead Jan FOMC Minutes

EXECUTIVE SUMMARY

- MNI BRIEF: Fed's Barr Sees Rates On Hold 'For Some Time'

- MNI FED: Goolsbee Warns On Not Tame Services Inflation But Repeats Cuts View

- MNI US DATA: Weekly ADP Employment Sees Fastest Increase Since Late November

US

MNI FED: Goolsbee Warns On Not Tame Services Inflation But Repeats Cuts View

Chicago Fed’s Goolsbee ('27 voter, generally dovish but dissented hawkishly at Dec FOMC) spoke on CNBC in which he unsurprisingly reiterated his post-CPI comments from Friday that the January report had some encouraging bits but also some concerns, with still pretty high services inflation. He again warned that services inflation remains elevated but if price hikes linked to tariffs are a one-off, it could allow policymakers room to move.

- “I do think that if this proves to be transitory, and we can show that we’re on path back to 2% inflation, I still think there’s several more rate cuts that can happen in 2026, but we’ve got to see it”.

MNI BRIEF: Fed's Barr Sees Rates On Hold 'For Some Time'

The Federal Reserve should keep interest rates on hold "for some time" until data show goods inflation receding and the job market staying stable, Fed Governor Michael Barr said Tuesday, adding the AI boom is unlikely to be a reason for lowering rates. "The prudent course for monetary policy right now is to take the time necessary to assess conditions as they evolve. I would like to see evidence that goods price inflation is sustainably retreating before considering reducing the policy rate further, provided labor market conditions remain stable," he said in remarks prepared for the New York Association for Business Economics in New York, N.Y.

NEWS

IRAN'S ARAGHCHI SAYS 'GOOD PROGRESS' ON TALKS WITH US ... NEXT ROUND OF US TALKS NOT YET DECIDED, Bbg

US TSYS

MNI US TSYS: Late Tuesday Roundup: Curves Twist Flatter Lead-Up to Jan FOMC Minutes

- Treasuries look to finish near late session lows, curves twisting flatter with bonds outperforming: 2s10s -2.524 at 61.337, 5s30s -2.810 at 105.895.

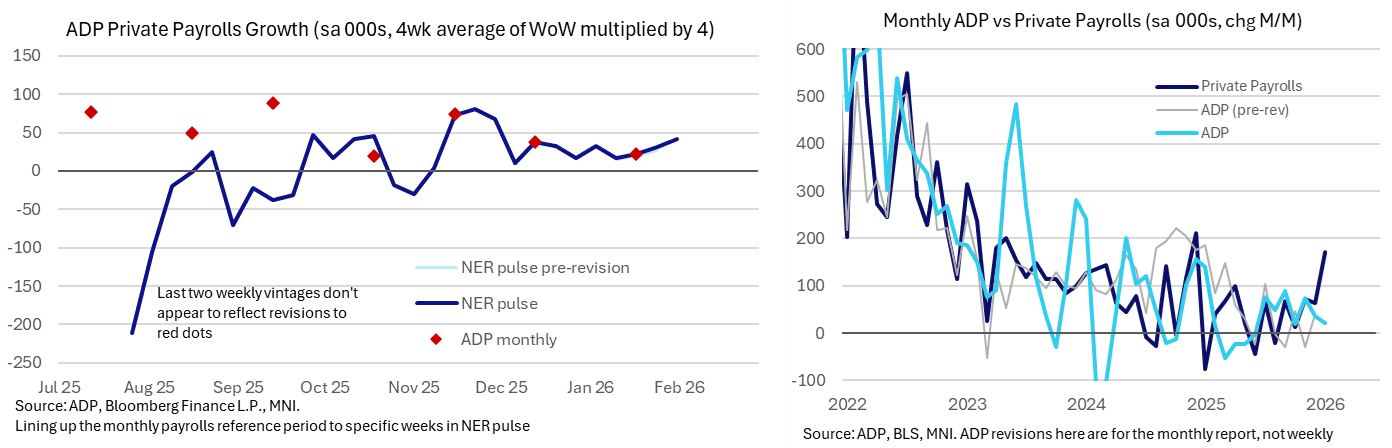

- Tsys retreated after weekly ADP employment increased an average 10.25k per week in the four weeks to Jan 31, an improvement from the upward revised 7.75k (initial 6.5k) in the previous four weeks to Jan 24. That's the fastest increase since late November in the latest vintage of data for a series that is revised from week to week.

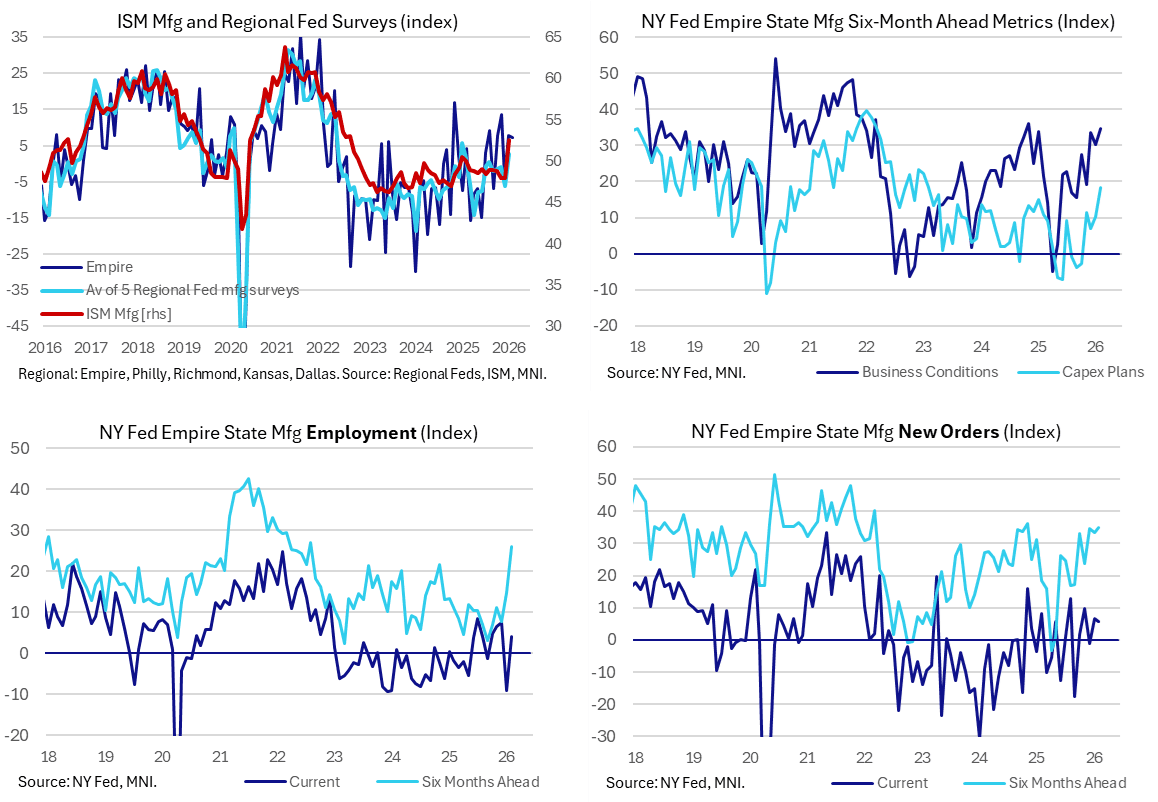

- The NY Fed's Empire State manufacturing survey was unusually steady in February for what is usually a volatile headline series. Six-month ahead metrics were more notable, with general business condition expectations at the highest since late 2021 helped by some strong improvements in both employment and capex expectations.

- The Federal Reserve should keep interest rates on hold "for some time" until data show goods inflation receding and the job market staying stable, Fed Governor Michael Barr said Tuesday, adding the AI boom is unlikely to be a reason for lowering rates.

- Chicago Fed Goolsbee reiterated that services inflation remains elevated but if price hikes linked to tariffs are a one-off, it could allow policymakers room to move.

- Looking ahead to Wednesday: Aussie wage price index data and the RBNZ decision highlight the APAC data docket, before the focus turns to UK CPI on Wednesday. Later in the session, FOMC minutes will take the spotlight.

OVERNIGHT DATA

MNI US DATA: Weekly ADP Employment Sees Fastest Increase Since Late November

Weekly ADP employment increased an average 10.25k per week in the four weeks to Jan 31, an improvement from the upward revised 7.75k (initial 6.5k) in the previous four weeks to Jan 24. That's the fastest increase since late November in the latest vintage of data for a series that is revised from week to week.

- The monthly equivalent of 41k implies an improvement from the 22k in the January reference period (the week including the 12th day of the month) for back similar to the 37k in December and 74k in November. The latter followed huge upward revisions as part of the monthly January report two weeks ago, having previously reported at -34k decline.

- Whilst latest weekly ADP data have stabilized after what were previously seen as declines in the summer to fall of 2025, they still lagged a surprisingly strong 172k increase in private payrolls in the BLS January report.

MNI US DATA: Manufacturing Firms Eye Sizeable Increase In Capex - NY Fed

The NY Fed's Empire State manufacturing survey was unusually steady in February for what is usually a volatile headline series. Six-month ahead metrics were more notable, with general business condition expectations at the highest since late 2021 helped by some strong improvements in both employment and capex expectations.

- The Empire State manufacturing index inched lower to 7.1 (cons 6.2) in February after 7.7 in January, sitting between the 13.5 back in November (highest since Nov 2024) and -3.7 in December. The new orders sub-component echoed these latest developments, dipping from 6.5 to 5.8 but still starting 2026 with an improvement compared to the -0.9 averaged throughout 2025.

MARKETS SNAPSHOT

Key market levels of markets in late NY trade:

DJIA up 70.33 points (0.14%) at 49565.02

S&P E-Mini Future up 15.75 points (0.23%) at 6865.5

Nasdaq up 58.4 points (0.3%) at 22602.3

US 10-Yr yield is up 0.4 bps at 4.0521%

US Mar 10-Yr futures are down 1.5/32 at 113-4

EURUSD down 0.0003 (-0.03%) at 1.1848

USDJPY down 0.19 (-0.12%) at 153.28

WTI Crude Oil (front-month) down $0.59 (-0.94%) at $62.30

Gold is down $114.29 (-2.29%) at $4876.90

European bourses closing levels:

EuroStoxx 50 up 42.97 points (0.72%) at 6021.85

FTSE 100 up 82.48 points (0.79%) at 10556.17

German DAX up 197.49 points (0.8%) at 24998.4

French CAC 40 up 44.96 points (0.54%) at 8361.46

US TREASURY FUTURES CLOSE

Curve update:

3M10Y +0.158, 36.823 (L: 32.942 / H: 37.721)

2Y10Y -2.733, 61.128 (L: 61.093 / H: 63.705)

2Y30Y -4.373, 124.091 (L: 123.782 / H: 128.561)

5Y30Y -2.81, 105.895 (L: 105.472 / H: 109.504)

Current futures levels:

Mar 2-Yr futures down 1.875/32 at 104-12.375 (L: 104-12 / H: 104-15.625)

Mar 5-Yr futures down 2/32 at 109-20 (L: 109-18.75 / H: 109-27)

Mar 10-Yr futures down 1.5/32 at 113-4 (L: 113-02.5 / H: 113-14)

Mar 30-Yr futures up 6/32 at 117-31 (L: 117-21 / H: 118-12)

Mar Ultra futures up 9/32 at 120-30 (L: 120-18 / H: 121-13)

MNI US 10YR FUTURE TECHS: (H6) Impulsive Bull-Wave Extends

- RES 4: 114-00 Round number resistance

- RES 3: 113-29+ High Oct 17 ‘25 high and a key M/T resistance

- RES 2: 113-22+ High Nov 22 ‘25 and a key resistance

- RES 1: 113-14 Intraday high

- PRICE: 113-11 @ 11:12 GMT Feb 17

- SUP 1: 112-31 High Dec 18

- SUP 2: 112-20 High Feb 11

- SUP 3: 112-08+ 50-day EMA

- SUP 4: 111-26 Low Feb 9

An impulsive bull-wave in Treasuries remains intact as the contract extends the reversal off the Jan 20 low. Price is through 113-04, 76.4% of the Nov 25 - Jan 20 bear leg. This paves the way for an extension towards 113-22+, the Nov 22 ‘25 high and a key resistance. Initial firm support to watch is 112-08+, the 50-day EMA. A short-term pullback would be considered corrective and would unwind an overbought trend reading.

SOFR FUTURES CLOSE

Current White pack (Mar 26-Dec 26):

Mar 26 -0.010 at 96.360

Jun 26 -0.035 at 96.555

Sep 26 -0.045 at 96.790

Dec 26 -0.045 at 96.915

Red Pack (Mar 27-Dec 27) -0.03 to -0.01

Green Pack (Mar 28-Dec 28) -0.005 to steady

Blue Pack (Mar 29-Dec 29) -0.005 to steady

Gold Pack (Mar 30-Dec 30) steady to +0.005

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.66% (+0.01), volume: $3.169T

- Broad General Collateral Rate (BGCR): 3.64% (+0.01), volume: $1.337T

- Tri-Party General Collateral Rate (TCR): 3.64% (+0.01), volume: $1.311T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.64% (+0.00), volume: $90B

- Daily Overnight Bank Funding Rate: 3.63% (+0.00), volume: $182B

FED Reverse Repo Operation

RRP usage rebounds slightly to $0.441B with 5 counterparties this afternoon vs. $.377B Friday (lowest level since early 2021). Compares to last year's highest excess liquidity measure: $460.731B on June 30.

MNI PIPELINE: Corporate Bond Update: $4B Amgen 4Pt Launched

- Date $MM Issuer (Priced *, Launch #)

- 02/17 $4B #Amgen $1B 5Y +60, $1.75B 10Y +82, $500M 20Y +90, $750M 30Y +97

- 02/17 $1B #PG&E 30.5NC5.25 6.85%

- 02/17 $600M #Eastman Chemical 5Y +92

- 02/17 $600M #Camden Property 10Y +85

- 02/17 $500M CNX Resources 8NC3 5.875%

- 02/17 $Benchmark Panama 8Y +175a, 12Y +195a

- 02/17 $Benchmark Barclays 4.25NC3.25 +75, 4.25NC3.25 SOFR+93, 6NC5 +90, 11NC10 +115

- 02/17 $Benchmark Howmet Aerospace 2Y +35, 3Y +43, 10Y +70

MNI BONDS: EGBs-GILTS CASH CLOSE: Long-End Rally Continues

European long-end yields resumed their descent Tuesday as bull flattening continued.

- UK labour market data showed quantities data weaker than expected and compensation broadly in line, very much keeping a March BOE cut in play.

- February German ZEW expectations pulled back from January's four-year highs, but this was not a market mover.

- Early gains faded over the course of the session as equities found their footing, with Gilts retracing more than Bunds.

- For the day, the German and UK curves both bull flattened, with periphery/semi-core EGB spreads narrowing very modestly.

- Wednesday brings UK inflation data for January - MNI's preview is here. We also hear from the ECB's Villeroy, Cipollone, and Schnabel.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.5bps at 2.036%, 5-Yr is down 1.1bps at 2.328%, 10-Yr is down 1.6bps at 2.738%, and 30-Yr is down 2.7bps at 3.405%.

- UK: The 2-Yr yield is unchanged at 3.587%, 5-Yr is down 1bps at 3.797%, 10-Yr is down 2.3bps at 4.376%, and 30-Yr is down 2.5bps at 5.181%.

- Italian BTP spread down 0.1bps at 61.2bps / Spanish down 0.5bps at 37.8bps

MNI FOREX: Notable GBP Weakness, USDJPY Reverses Firmly Higher

- Sterling weakness has been a key feature across the G10 FX space on Tuesday, price action that followed a softer-than-expected set of labour market data from the UK. Alongside a firmer dollar backdrop, GBPUSD is down 0.65% as we approach the APAC crossover, briefly slipping below 1.35.

- Today’s move lower has seen the pair breach the 50-day EMA, and a sustained break of this average would undermine the recent bull theme. Meanwhile, EURGBP has rallied over half a percent on the session, and in the process has pierced a key resistance point at 0.8746, the Jan 21 high. A clear break of this level would also highlight a potential trend reversal.

- Elsewhere, volatility for the Japanese yen has not abated, with USDJPY posting a 122pip range on the session. Initial strength for JGBs and waning risk sentiment prompted a move down for USDJPY to session lows of 152.70, however, the broader USD bid and eventual stabilising risk sentiment allowed the move to steadily reverse across the session, resulting in fresh highs at 153.92.

- Short-term USDJPY parameters appear well established; the January lows at 152.10 provide key support, while the post-NFP highs at 154.65 offer the most notable resistance.

- Downside momentum for EURUSD had also been steadily playing out across Tuesday’s session, with the latest weakness testing the lows from last Monday’s range, of which spot had been trading within over the past six sessions. A lower close for EURUSD today would represent a sixth consecutive session of declines. Akey support area for EURUSD combines both the Feb 06 low and the 50-day EMA, just below 1.1770.

- Aussie wage price index data and the RBNZ decision highlight the APAC data docket, before the focus turns to UK CPI on Wednesday. Later in the session, FOMC minutes will take the spotlight.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 18/02/2026 | 0700/0700 | *** | Consumer Inflation Report (1dp) | |

| 18/02/2026 | 0700/0700 | *** | Consumer Inflation Report (2dp) | |

| 18/02/2026 | 0700/0700 | *** | Producer Prices | |

| 18/02/2026 | 0745/0845 | *** | HICP (f) | |

| 18/02/2026 | 0900/1000 | ECB Cipollone at ABI's Executive Committee Meeting | ||

| 18/02/2026 | 1000/0500 | * | CREA Existing Home Sales | |

| 18/02/2026 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 18/02/2026 | 1330/0830 | *** | Housing Starts | |

| 18/02/2026 | 1330/0830 | *** | Housing Starts | |

| 18/02/2026 | 1330/0830 | ** | Durable Goods New Orders | |

| 18/02/2026 | 1330/0830 | ** | Durable Goods New Orders | |

| 18/02/2026 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 18/02/2026 | 1415/0915 | *** | Industrial Production | |

| 18/02/2026 | 1700/1800 | ECB Schnabel Panel at Berlin-Brandenburg Academy of Sciences and Humanities | ||

| 18/02/2026 | 1800/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 18/02/2026 | 1800/1300 | Fed's Michelle Bowman | ||

| 18/02/2026 | 1900/1400 | *** | FOMC Minutes | |

| 18/02/2026 | 2100/1600 | ** | TICS | |

| 19/02/2026 | 2350/0850 | * | Machinery orders | |

| 19/02/2026 | 0030/1130 | *** | Labor Force Survey |