MNI ASIA MARKETS ANALYSIS:Hassett Telegraphs Lower Job Numbers

HIGHLIGHTS

- U.S. NEC Director Kevin Hassett warned markets should expect “slightly lower” jobs numbers ahead of this Wednesday’s NFP release, although he stresses that the outcome “shouldn’t trigger panic", Bbg.

- Early uncertainty over UK PM Starmer's future, with some speculation that he could resign in the very near future - which would be considered a fiscally-negative and thus Gilt-negative development.

- NY Fed inflation expectations gauges showed a drop in 1Y to 3.09% (3.42% prior) vs analysts' expectation of a steady figure (unrounded), and a 6-month low.

- Focus turns to US retail sales data headlines Tuesday’s calendar, followed by US employment (Wed) and US CPI (Fri).

US TSYS

MNI US TSYS: Hassett on Declining Labor Force - Don't Panic

- Treasuries extended early session highs after jobs comment from U.S. NEC Director Hassett, gradually extending highs to finish modestly higher after the bell. Hassett noted that “there's a pretty big decline in the labor force because of illegals leaving the country. And so the breakeven job number is quite a bit lower than it was under Joe Biden."

- Hassett posited "you should expect slightly smaller job numbers that are consistent with high GDP growth right now, and that one shouldn't panic if you see a sequence of numbers that are lower than you're used to." explaining that "population growth is going down and productivity growth is skyrocketing.”

- Rate locks and fast$ selling for $20B Alphabet 7pt debt issuance helped keep rates contained on the day.

- Currently, TYH6 trades +2.5 at 112-06 vs. -07 high, an extension higher would undermine the bear theme and open 112.-22, the Jan 7 high. For bears, a reversal lower would refocus attention on 111-09, the Jan 20 low and bear trigger.

- The stabilisation for risk sentiment late last week had been a key factor into the recent dollar recovery stalling, and the DXY returning to the prior breakdown point around the 98.00 mark appears to have provided an attractive entry point for those looking to reengage shorts.

- Focus turns to weekly ADP NER pulse employment numbers, Import/Export Prices, several Fed speakers and a $58B Tsy 3Y note sale.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.64% (-0.01), volume: $3.195T

- Broad General Collateral Rate (BGCR): 3.62% (-0.01), volume: $1.322T

- Tri-Party General Collateral Rate (TCR): 3.62% (-0.01), volume: $1.301T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.64% (+0.00), volume: $106B

- Daily Overnight Bank Funding Rate: 3.63% (+0.00), volume: $206B

FED Reverse Repo Operation

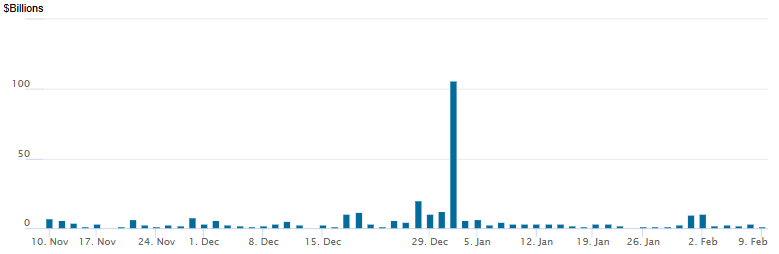

RRP usage retreats to $1.306B with 10 counterparties this afternoon vs. $3.111B Friday. Compares to December 12 low of $0.838B (lowest level since mid-March 2021); this years highest excess liquidity measure: $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury option flow continued to revolve around low delta put structures Monday, underlying futures gradually gaining through the session, curves off earlier steeper levels (2s10s currently +.660 at 71.091 vs. 73.699 high). Projected rate cut pricing looks steady to slightly higher vs. late Friday levels (*): Mar'26 steady at -4.8bp, Apr'26 at -10.1bp (-9.6bp), Jun'26 at -24.8bp (-24.1bp), Jul'26 at -34.1bp (-32.6bp).

SOFR Options:

-40,000 0QG6 97.12 calls, 0.5

+12,500 0QG6 96.75 puts, 1.0 vs. 96.865/0.10%

+5,000 0QM6 96.25 puts, 2.0 ref 96.40

1,500 SFRH6 96.37/96.50 1x2 call spds

Block, 5,000 SFRJ6 96.75/96.93 call spds, 2.5

2,000 0QG6 96.87 puts ref 96.855

-5,000 SFRH6 96.31/96.37/96.43 iron flys, 3.75 ref 96.39

2,350 SFRJ6 96.31/96.43 put spds, 1.0 ref 96.60

Treasury Options:

-5,000 FVJ6 110 calls, 11 ref 109-02

over 10,000 TYH6 113.5 calls, 3 total volume over 17.4k

2,000 USH6 113.5/117 strangles, 20

4,300 TYJ6 113 calls, 20 ref 111-30

7,500 TYH6 112 puts, 23 last ref 111-28.5

+1,000 TYH6 112 straddles, 41

-3,500 TYH6 111.75 puts, 15

+5,000 wk2 TY 110.5/111.5 put spds, 5.0 ref 112-00

+4,500 FVJ6 107.75/108.25/108.50/108.75 broken put condors, 1 vs. 109-05/0.02%

-1,800 USH6 115/116/117/119 broken call condors, 18 vs. 115-01/0.12%

2,500 wk2 TY 111.5/112.25 2x5 call spds, 23 (exp 02/13)

+1,500 TYJ6 112.5 calls 26 vs. 111-25.5/0.32%

+1,750 Wednesday wkly 10Y 111.75 puts, 11 (exp 02/11)

MNI BONDS: EGBs-GILTS CASH CLOSE: Curves Steepen, Gilts Recover Most Early Losses

UK political uncertainty continued to impact Gilts Monday.

- Gilt yields picked up throughout the morning session, peaking in mid-afternoon before falling back in the couple of hours ahead of the cash close.

- The driving dynamic continued to be uncertainty over UK PM Starmer's future, with some speculation that he could resign in the very near future - which would be considered a fiscally-negative and thus Gilt-negative development.

- Concerns peaked intraday amid reports that the Scottish Labour leader would call for Starmer to step down. Gilts regained ground late as various Labour leaders expressed support for the PM.

- In contrast, Bund yields topped out early and descended thereafter, though trade was well within last week's ranges.

- Banque de France Governor Villeroy announced that he will step down in early June, a year before his term officially ends, though this brought no discernable market reaction.

- Supply from US tech giant Alphabet appeared to weigh on long end instruments, with steepening seen through global markets.

- On the day the German curve twist steepened modestly, with the UK's bear steepening. Periphery/semi-core EGB spreads closed mixed, with BTPs outperforming.

- As we discuss in our Gilt Week Ahead (link), we hear from BOE's Mann after the cash close Monday; global focus for the week is on the latest US employment and inflation reports.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.8bps at 2.078%, 5-Yr is down 0.7bps at 2.406%, 10-Yr is down 0.2bps at 2.84%, and 30-Yr is up 1.5bps at 3.527%.

- UK: The 2-Yr yield is up 0.2bps at 3.626%, 5-Yr is up 0.3bps at 3.9%, 10-Yr is up 1.3bps at 4.527%, and 30-Yr is up 1.1bps at 5.346%.

- Italian BTP spread down 1.3bps at 61.1bps / French OAT up 0.5bps at 60.6bps

EGB OPTIONS: Notable Vol Trades In UK Rates

Monday's Europe rates/bond options flow included:

- DUJ6 106.90/106.80/106.70/106.50p condor, bought for 2.25 in 10k total now

- ERZ6 98.125/98.3125/98.4375/98.625 call condor paper paid 2.75 on 3K

- SFIH6 96.50^, bought for 5.75 in 4k

- SFIH6 96.45/96.55/96.60/96.75 call condor, paper sells for 2.75 in 12k

- SFIN6 96.60/96.80cs 1x2, bought for 5.5 in 8k

- SFIU6 96.65^, trades for 22.25 in 12k, this was done Paper to Paper, some suggest bought

- SFIU6 96.75^, bought for 20.5 in 5k

MNI FOREX: Renewed Dollar Pessimism, AUDUSD Back to Cycle Highs

- Constructive price action for precious metals and equities on Monday have facilitated a revival of the bearish dollar narrative. The stabilisation for risk sentiment late last week had been a key factor into the recent dollar recovery stalling, and the DXY returning to the prior breakdown point around the 98.00 mark appears to have provided an attractive entry point for those looking to reengage shorts.

- Renewed dollar pessimism appears to have also been bolstered by reports that Chinese officials urged banks to limit purchases of US government bonds and instructed those with high exposure to reduce their positions. The DXY is currently 0.8% lower on the session as we approach the APAC crossover, providing an interesting dynamic as we approach the plethora of tier-one US data this week.

- AUDUSD’s impressive 1.15% rally on Monday has seen spot narrow in on its respective cycle peak at 0.7094. Above this bull trigger, markets will turn their focus to 0.7158, the Feb 2 2023 high and 0.7208, a Fibonacci retracement level.

- The Swiss Franc has matched the Australian dollar as one of the best performing majors on Monday and while USDCHF has not returned to recent extremes, EURCHF has notably dipped to a fresh low of 0.9127, which represents the worst levels since the removal of the floor in 2015.

- USDJPY has posted an impressive 225 pip range following Sunday’s election in Japan. While Takaichi’s victory initially weighed on the yen as markets focused on the concerns surrounding the fiscal trajectory, subsequent remarks from officials on monitoring FX and the broader weakness have assisted the reversal to levels sub-156.00.

- US retail sales data headlines Tuesday’s calendar, while markets will then swiftly turn their focus to US employment (Wed) and US CPI (Fri).

MNI FX OPTIONS: Expiries for Feb10 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1850(E1.1bln), $1.1875(E787mln), $1.1900-10(E1.9bln), $1.1945(E567mln), $1.2000(E1.5bln)

- USD/JPY: Y157.00($884mln)

- AUD/USD: $0.6900(A$1.2bln), $0.7100(A$1.2bln)

MNI US STOCKS: Late Equities Roundup: Tech Shares Help DJIA Extend Record High Again

- Stocks are drifting modestly higher late Monday, technology stocks helping the DJIA extend record highs for the second consecutive session, SPX emini and Nasdaq indexes still shy of late January record highs.

- Currently, the DJIA trades up 56.89 points (0.11%) at 50175.99 vs. 50219.40 high, S&P E-Mini Futures up 45.5 points (0.65%) at 6998, Nasdaq up 266.8 points (1.2%) at 23297.78.

- Software services and chip maker shares led advances on the week opener: AppLovin +13.95% after CapitalWatch

issued a public apology and acknowledged that its report, published last month, contained inaccuracies linking AppLovin shareholder Hao Tang to criminal organizations, CNBC reported. - Oracle gained +10.52% after strengthening its "healthcare cloud and AI strategy, announcing the successful migration of five Ontario hospitals’ electronic health records to its cloud platform alongside the launch of a clinical AI pilot aimed at boosting clinician efficiency and system performance," Bbg reported.

- Other gainers included: Palantir Technologies +6.10%, Corning +5.84%, Broadcom +4.20% and Advanced Micro Devices +4.02%.

- Conversely, Health Care sector shares underperformed, Waters Corp shares declining over 12% "after the company closed its acquisition of a Becton Dickinson unit and gave earnings guidance below expectations," DJ reported. Other laggers included Merck -3.85%, Molina Healthcare -3.61% and Elevance Health -3.11%.

COMMODITIES

MNI OIL: Americas End of Day Oil Summary: Crude Higher

WTI Crude ended higher amid heightened US-Iran tensions after the US Maritime Administration effectively extended an advisory for US vessels that traverse the Strait of Hormuz, adding some upward pressure. US economic data remains nominally supportive though January’s delayed jobs report could show slower labor growth.

- Today’s MARAD advisory is essentially unchanged to the prior advisory, which was due to expire today, apart from a small reference to a Feb. 3 incident in the Strait. Nevertheless, crude moved to daily highs on the headlines, with markets sensitive to US-Iran tensions.

- Iran's Foreign Minister stated that uranium enrichment is "non-negotiable" and ruled out discussing ballistic missiles or regional influence, with the US demanding a comprehensive deal covering all three areas, whilst threatening sanctions.

- WTI Mar futures were up 1.2% at $64.36

- WTI Apr futures were up 1.3% at $64.16

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 10/02/2026 | 0700/0800 | ** | Private Sector Production m/m | |

| 10/02/2026 | 0700/0800 | *** | CPI Norway | |

| 10/02/2026 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 10/02/2026 | 1100/0600 | ** | NFIB Small Business Optimism Index | |

| 10/02/2026 | 1200/0700 | ** | Brazil Final CPI | |

| 10/02/2026 | - | *** | New Loans | |

| 10/02/2026 | - | *** | Money Supply | |

| 10/02/2026 | - | *** | Social Financing | |

| 10/02/2026 | 1330/0830 | *** | Employment Cost Index | |

| 10/02/2026 | 1330/0830 | ** | Import/Export Price Index | |

| 10/02/2026 | 1330/0830 | *** | Retail Sales | |

| 10/02/2026 | 1330/0830 | *** | Retail Sales | |

| 10/02/2026 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 10/02/2026 | 1500/1000 | * | Business Inventories | |

| 10/02/2026 | 1500/1000 | * | Business Inventories | |

| 10/02/2026 | 1700/1200 | *** | USDA Crop Estimates - WASDE | |

| 10/02/2026 | 1700/1200 | Cleveland Fed's Beth Hammack | ||

| 10/02/2026 | 1800/1300 | Dallas Fed's Lorie Logan | ||

| 10/02/2026 | 1800/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 11/02/2026 | 0130/0930 | *** | CPI | |

| 11/02/2026 | 0130/0930 | *** | Producer Price Index |