MNI ASIA MARKETS ANALYSIS: Ylds Rising Ahead Headline Sep Jobs

HIGHLIGHTS

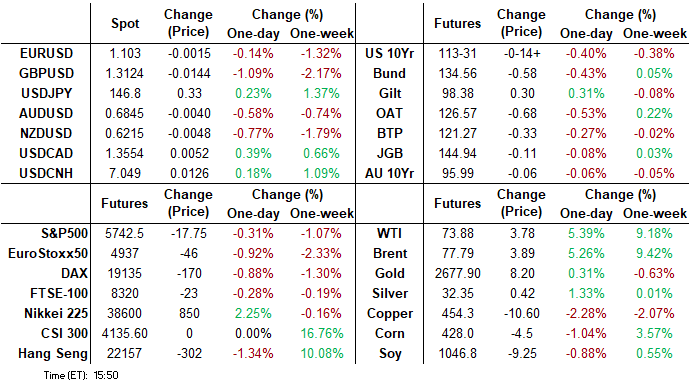

- Treasuries near lowest levels since early September ahead of Friday's headline jobs report, curves mixed with 2s10ss +.313 at 13.851.

- Projected rate cuts look steady to mildly weaker vs. this morning's levels (*): Nov'24 cumulative -33.1bp (-34.1bp), Dec'24 -67.1bp (-68.9bp), Jan'25 -94.9bp (-99.5bp).

- Weaker stocks are still not far off July's record highs while crude prices have surged near $4.0 as Mideast tensions continue to heat up.

US TSYS: Near One Month Lows Ahead September Jobs Report

- Treasuries are trading near late session lows -- levels that have not been seen since early September in the lead up to Friday's headline jobs report. The TYZ4 10y futures contract is currently trading -15 at 113-30.5, below technical support of 114-00.5 (Sep 4 low) with next level at 113-29.5 (50-day EMA).

- Rates have been under pressure since this morning's mixed data: Initial jobless claims increased to 225k (sa, cons 221k) in the week to Sep 28 after a slightly upward revised 219k (initial 218k). No sign of an impact from Hurricane Helene, which made landfall on the Florida Gulf Coast in the evening of Sep 26 to leave very little time to show in this week’s data. Florida NSA claims for example fell 1.1k to 6.45k.

- ISM Services were clearly stronger than expected with some genuinely strong readings for both prices paid and new orders but the decline in employment back into contractionary territory takes some of the gloss off an otherwise strong report. ISM Services: 54.9 (cons 51.7) in Sep after 51.5 in Aug and 51.4 in Jul for its highest since Feb’23. Prices paid: 59.4 (cons 56.0) after 57.3 – highest since Jan and back to the 59.3 averaged in 2023. Employment: 48.1 (cons 50.0) after 50.2 for what had been two months above 50. It returns close to the 47.7 averaged in a disappointing string of readings through 1H24.

- Focus on Friday's headline nonfarm payrolls where growth is seen accelerating marginally to 150k in September after the weaker than expected 142k in August, although some analysts look for an upward revision to August owing to a strong tendency to initially undercount in that month.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M -0.00578 to 4.85077 (+0.00667/wk)

- 3M -0.00852 to 4.58972 (-0.00363/wk)

- 6M -0.00900 to 4.27362(+0.01177/wk)

- 12M +0.01546 to 3.83337 (+0.05029/wk)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.92% (-0.13), volume: $2.426T

- Broad General Collateral Rate (BGCR): 4.87% (-0.05), volume: $816B

- Tri-Party General Collateral Rate (TGCR): 4.87% (-0.05), volume: $777B

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.83% (+0.00), volume: $81B

- Daily Overnight Bank Funding Rate: 4.83% (+0.00), volume: $204B

FED Reverse Repo Operation

RRP usage falls to $341.248B this afternoon from $383.398B prior. Compares to $239.386B on Monday September 16 2024 -- the lowest level since early May 2021. Number of counterparties at 57 from 67 prior.

US SOFR/TREASURY OPTION SUMMARY

Option desks report better SOFR/Treasury put options on net Thursday, underlying futures weaker, near session lows in the lead up to Friday's headline employment data for September. SOFR White pack (SFRZ4-SFRU5) currently -0.040-0.095, while projected rate cuts look steady to mildly weaker vs. this morning's levels (*): Nov'24 cumulative -33.1bp (-34.1bp), Dec'24 -67.1bp (-68.9bp), Jan'25 -94.9bp (-99.5bp). Salient trade includes:

SOFR Options:

- Block, 20,000 SFRZ4 95.37/95.50 put spds, 0.5 vs. 95.90/0.05%

- 15,000 0QX4 96.50/96.81 3x2 put spds, 15.5 net package ref 96.95 at 1159:38ET

- 5,000 2QV4 96.50/96.75 put spds, 2.0 ref 96.925

- +4,000 SFRV4 95.75/95.81/95.87 put flys, 1.0 vs. 95.975/0.03%

- +10,000 0QX4 96.50/96.81 3x2 put spreads 15.5 ref 96.94

- +10,000 SFRH5 97.75/98.75 2x3 call spds 6.0 ref 96.425

- +10,000 SFRZ4 95.81/95.93 2x1 put spds 0.5 ref 95.935

- +5,000 SFRX4 96.06/96.18/96.25/96.43 call condors, 1.5 ref 95.94

- +5,000 SFRU6 95.00 puts, 11.5 vs. 96.97/0.10%

- +4,000 SFRX4 96.12/96.25 call spd, 2.25 vs. 95.945/0.10%

- +2,500 SFRM5 96.00/96.50 put spd 4.0 over 97.75 call vs. 96.77/0.37%

- +5,000 SFRH5 96.00/96.37 put spds vs 97.50 call w/

- +5,000 SFRH5 96.25/97.25 put over risk reversals, +16.5 total db

- +8,000 SFRV4 96.12/96.25 call spds 1.25 ref 95.96

- +4,000 2QV4 97.25 calls, 1.0 ref 95.94

- Blocks, 10,000 SFRU5 96.25/96.62 3x2 put spds, 8.0 net ref 96.915

- 4,000 SFRV4 96.06/96.18 call spds ref 95.96

- 1,500 SFRF5 96.12/96.31/96.37/96.56 put condors

- 8,000 SFRV4 95.87/96.18/96.50 call flys

- Block, 4,000 SFRV4 96.12/96.18 call spds, .75 ref 95.955

- Block/screen, 11,600 SFRH5 95.25/95.75/96.00 broken put flys, 1.5 ref

- Block, 10,000 SFRX4 96.12/96.25 call spds 2.25 vs. 95.945/0.10%

- 6,100 SFRV4 96.18/96.25 call spds ref 95.955

- 1,500 SFRX4 95.43/95.75 put spds vs. 96.00/96.12 call spd ref 95.955

- 2,000 SFRZ4 95.81 puts, ref 95.955

- Treasury Options:

- 5,000 USX4 121/122 put spds, 15 ref 124-00

- 11,500 TYX4 115.5/116.5/117.5 call flys ref 114-10 to 114-04

- 3,700 TUZ4 104.5/105 call spds ref 104-01.88

- 2,000 TYZ4 113/115 strangles, 133 ref 114-09

- 3,100 wk1 TY 113.5/114 put spds

- 3,500 wk1 TY 113.75/114 put spds

- over 3,700 TYX4 115 calls

- 1,500 TYX4 112.5/114 put spds, 27 ref 114-08

- 3,000 FVX4 110.25/111.5 1x2 call spds

MNI BONDS: EGBs-GILTS CASH CLOSE: Bailey Dovishness Spurs UK Steepening

Gilts outperformed EGBs Thursday in a steepening move on the UK curve.

- The session started on a very dovish note for the UK short end as BoE Gov Bailey said in an interview that the bank could be a "bit more aggressive" and a "bit more activist" on rate cuts.

- Bailey's comments added to perceived potential for back-to-back cuts in Nov and Dec, and there are now ~44bp of reductions priced through the latter meeting vs ~37bp at Wednesday's close. (In contrast, ECB pricing was relatively unchanged.) DMP data, while it didn't garner nearly the same degree of market reaction, was notable for showing softening in realised UK employment growth. It's unlikely to signal panic on the MPC at this stage though.

- While Gilt gains would pull back from extremes, particularly in mid-afternoon on a much stronger than expected US ISM Services report, they would bounce again toward the cash close and easily outperformed EGBs on the day.

- Indeed, EGBs performed poorly with renewed OAT spread widening (10Y/Bund +2.5bp) amid heavy French and Spanish supply. The belly underperformed on the German curve, with yields up around 4-5bp throughout; periphery EGB spreads tightened slightly.

- The focus of Friday's schedule will be a morning appearance by BoE's Pill, eyed for any corroboration of Bailey's perceived dovishness. We also get some Eurozone industrial production data, and Italian retail sales/budget readings, as well as multiple ECB speakers (incl Villeroy).

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 4.1bps at 2.081%, 5-Yr is up 5.3bps at 1.974%, 10-Yr is up 5.2bps at 2.144%, and 30-Yr is up 4.7bps at 2.463%.

- UK: The 2-Yr yield is down 4.8bps at 3.969%, 5-Yr is down 3bps at 3.865%, 10-Yr is down 0.9bps at 4.016%, and 30-Yr is up 0.4bps at 4.598%.

- Italian BTP spread up 1bps at 133.9bps / Spanish down 0.5bps at 78.8bps

MNI EURIBOR OPTIONS: Late Session Put Structure Buying

- ERZ4 97.12/97.00 1x2 put spread bought for 0.5 in 7.5k

- 0RZ4 98.00/97.75/97.62 broken put fly bought for 4.25 in 5k

FOREX

FOREX OPTIONS: Expiries for Oct04 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0950-70(E814mln), $1.1000(E1.9bln), $1.1040-50(E610mln), $1.1100(E941mln)

- USD/JPY: Y146.25($880mln), Y146.50($730mln), Y148.00($818mln)

- AUD/USD: $0.6850(A$784mln)

- USD/CAD: C$1.3350-73($2.2bln), C$1.3500-05($1.2bln), C$1.3530-45($813mln), C$1.3595-00($822mln)

EQUITIES

MNI Late Equities Roundup: Weaker, But Not Far From Record Highs

- Stocks hold moderately weaker late Thursday -- the lower half of the session range as some accounts squared up ahead of Friday's headline jobs report for September. That said, current levels are not far off record highs set back in July. Not bad when considering the tepid risk sentiment heading into the data, Mideast tensions and election uncertainty.

- Currently, the DJIA trades down 230.41 points (-0.55%) at 41965.05, S&P E-Minis down 19.75 points (-0.34%) at 5740.5, Nasdaq down 47 points (-0.3%) at 17877.87.

- Energy sector continues to benefit from a surge in crude prices (WTI tapping 73.92 high today) as Mideast tensions heat up. Oil and gas shares leading gainers: Valero +5.68%, Marathon Petroleum +5.42%, Diamondback Energy +3.81%, APA +3.71%. Meanwhile, Semiconductor stocks buoyed the IT sector for the second day running: Nvidia +3.31%, Micron +1.80%, AMD +1.61%.

- On the flipside, Consumer Discretionary and Materials sectors continued to underperform in late trade: Tesla -4.18%, Borg Warner -1.78%, Aptiv -1.76%. Metals and mining stocks weighed on the Materials sector with Freeport-McMoRan -2.13%, Newmont -1.72%.

MNI EQUITY TECHS: E-MINI S&P: (Z4) Shallow Correction - RES 4: 5900.00 Round number resistance

- RES 3: 5871.77 2.0% Upper Bollinger Band

- RES 2: 5868.50 1.00 proj of the Apr 19 - Jul 16 - Aug 5 price swing

- RES 1: 5830.00 High Sep 26

- PRICE: 5741.50 @ 1413 BST Oct 3

- SUP 1: 5726.75 20-day EMA

- SUP 2: 5656.94 50-day EMA

- SUP 3: 5500.00 Round number support

- SUP 4: 5451.25 Low Sep 6 and a bear trigger

A bull cycle in S&P E-Minis remains intact and the latest shallow pullback is considered corrective. Recent gains reinforce a bullish theme and note that moving average studies are in a bull-mode setup, highlighting a dominant uptrend. Scope is seen for a climb towards 5868.50, a Fibonacci projection, and 5900.00 further out. On the downside, initial support to watch is 5726.75, the 20-day EMA. Key support lies at 5656.94, the 50-day EMA.

COMMODITIES

MNI Oil Gains On Discussions Of Iran Oil Facility Strikes

- Oil prices have gained sharply on Thursday after President Biden made a remark that suggested Israel strikes on Iranian oil facilities are under discussion.

- While not too far outside of expectations, striking Iranian oil facilities could pose risks to supplies through the Strait of Hormuz.

- WTI Nov 24 is up by 5.2% at $73.8/bbl.

- Having pierced resistance at the 50-day EMA, at $71.69, focus turns to $76.40 next, the Aug 26 high.

- In contrast, US natural gas prices rallied on Thursday, supported by higher demand forecasts over the next week and a drop in output.

- US Natgas Nov 24 is up by 2.8% at $2.97/mmbtu.

- Meanwhile, spot gold is broadly unchanged at $2,659/oz today.

- Elsewhere, copper has fallen by 2.2% to $455/lb, unwinding gains made over the previous two sessions.

- For copper, key near-term resistance is seen at $479.00, Monday’s intraday high, while key support is at $433.62, the 50-day EMA.

FRIDAY DATA CALENDAR

| Date | ET | Impact | Period | Release | Prior | Consensus | |

| 04/10/2024 | 0830 | *** | Sep | Average Hourly Earnings y/y, current month | 3.8 | 3.7 | % |

| 04/10/2024 | 0830 | *** | Sep | Average Hourly Earnings, m/m | 0.4 | 0.3 | % |

| 04/10/2024 | 0830 | *** | Sep | Average Workweek, All Workers | 34.3 | 34.3 | hrs |

| 04/10/2024 | 0830 | *** | Sep | Nonfarm Payrolls | 142.0 | 130.0 | (k) |

| 04/10/2024 | 0830 | *** | Sep | Prev Nonfarm Payrolls, Rev | -- | -- | (k) |

| 04/10/2024 | 0830 | *** | Sep | Private Payrolls | 118.0 | 110.0 | (k) |

| 04/10/2024 | 0830 | *** | Sep | Unemployment Rate | 4.2 | 4.2 | % |