MNI ASIA MARKETS ANALYSIS: US/IRAN Sentiment Warms Slightly

HIGHLIGHTS

- Crude prices retreated after Reuters reported comments from Iranian Foreign Minister Araghchi following second round of indirect nuclear talks with the US in Geneva. Araghchi said, "We've reached an understanding on main principles with the US."

- The Federal Reserve should keep interest rates on hold "for some time" until data show goods inflation receding and the job market staying stable, Fed Governor Michael Barr said Tuesday, adding the AI boom is unlikely to be a reason for lowering rates.

- Precious metals have fallen further today, pressured by an upswing in the dollar index and some positive signals from today’s Iran/US talks.

- Aussie wage price index data and the RBNZ decision highlight the APAC data docket, before the focus turns to UK CPI on Wednesday. Later in the session, FOMC minutes will take the spotlight.

US TSYS

MNI US TSYS: Late Tuesday Roundup: Curves Twist Flatter Lead-Up to Jan FOMC Minutes

- Treasuries look to finish near late session lows, curves twisting flatter with bonds outperforming: 2s10s -2.524 at 61.337, 5s30s -2.810 at 105.895.

- Tsys retreated after weekly ADP employment increased an average 10.25k per week in the four weeks to Jan 31, an improvement from the upward revised 7.75k (initial 6.5k) in the previous four weeks to Jan 24. That's the fastest increase since late November in the latest vintage of data for a series that is revised from week to week.

- The NY Fed's Empire State manufacturing survey was unusually steady in February for what is usually a volatile headline series. Six-month ahead metrics were more notable, with general business condition expectations at the highest since late 2021 helped by some strong improvements in both employment and capex expectations.

- The Federal Reserve should keep interest rates on hold "for some time" until data show goods inflation receding and the job market staying stable, Fed Governor Michael Barr said Tuesday, adding the AI boom is unlikely to be a reason for lowering rates.

- Chicago Fed Goolsbee reiterated that services inflation remains elevated but if price hikes linked to tariffs are a one-off, it could allow policymakers room to move.

- Looking ahead to Wednesday: Aussie wage price index data and the RBNZ decision highlight the APAC data docket, before the focus turns to UK CPI on Wednesday. Later in the session, FOMC minutes will take the spotlight.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.66% (+0.01), volume: $3.169T

- Broad General Collateral Rate (BGCR): 3.64% (+0.01), volume: $1.337T

- Tri-Party General Collateral Rate (TCR): 3.64% (+0.01), volume: $1.311T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.64% (+0.00), volume: $90B

- Daily Overnight Bank Funding Rate: 3.63% (+0.00), volume: $182B

FED Reverse Repo Operation

RRP usage rebounds slightly to $0.441B with 5 counterparties this afternoon vs. $.377B Friday (lowest level since early 2021). Compares to last year's highest excess liquidity measure: $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

Heavy SOFR & Treasury option volumes Tuesday, SOFR call interest rising through midday. Underlying futures gradually retreating from early session support - curves twisting flatter: 2s10s -2.559 at 61.302, 5s30s -2.942 at 105.763. Current projected rate cut pricing consolidating vs. early morning (*): Mar'26 at -2.1bp (-2.6bp), Apr'26 at -6.6bp (-7.1bp), Jun'26 at -19.4bp (-21bp), Jul'26 at -29.1bp (-31.6bp).

SOFR Options:

Block, 40,000 SFRK6 96.37/96.43/96.56 2x3x1 broken put flys, 4.25 net ref 96.56

Update, over +51,800 0QU6 98.00 calls, 6.0 vs. 96.935/0.13%

Update, over 95,700 SFRZ6 98.00 calls, 7.5 (+70k Fri at 4.0)

+48,000 0QZ6 98.00 calls, 7.5

-10,000 0QH6 96.81 puts, 2.0 ref 96.955

+2,000 0QJ6 96.87/97.00/97.25 2x3x1 broken call flys, 5.25

2,500 SFRU6 97.25/97.50/97.62 broken call flys, 1.25

+2,000 SFRM6 96.37/96.50/96.56 put flys, 1.75

+40,000 0QM6 97.50/98.00 call spds, 4.0

+20,000 SFRZ6 96.18/96.31/96.43 put flys, 1.5

+25,000 SFRM6 97.50/98.00 call spds, 4 ref 97.00

+20,000 SFRZ6 98.00 calls, 7.5 ref 96.95 (+70k Fri at 4.0)

Block, 4,000 SFRN6 96.43/96.56 put spds, 2.75

5,250 SFRK6 96.43 puts, 1.5 ref 96.58

3,500 0QK6 96.68/96.81 2x1 put spds, 0.0

+5,000 SFRH6 96.31/96.37/96.43/96.50 put condors, 2.75

+3,000 SFRM6 96.37/96.56 put spds 5.0 over SFRZ6 97.50/97.87 call spds

-2,750 SFRK6 96.62 put 8 over 0QK6 96.68 put

+5,000 SFRM6 96.68/96.81/96.87 broken call flys, 1.75

+15,000 3QM6 96.75/97.25 call spds vs. SFRM6 97.00/97.50 call spds, 7.5

+4,000 SFRH6 96.43/96.56 call spds, 1.0

+5,000 SFRM6 96.43/96.56 put spds, 6.5

2,000 SFRM6 96.37/96.50/96.62 put flys, 1.75

2,500 SFRZ6 97.50/98.00/98.50 call trees, cab

Treasury Options:

-8,000 TYK6 113/113.5 straddle strip, 334

+15,000 TYJ6 112 puts, 15 vs. 113-00.5/0.24%

5,000 TYJ6 111.5/112/112.5 put trees, 2

5,000 TYK6 110.5/112 2x1 put spds, 9

5,600 USH6 116 calls, 162 ref 118-02

10,000 FVJ6 109.5 puts, 19.5 vs. 109-24.75

2,400 TYH6 113.25/114/114.5 call flys, 8 ref 113-04

2,600 USK6 116 puts 108 ref 117-22

5,000 TYH6 112.75 calls vs TYJ6 114 calls. 12 net/Apr over

+3,500 FVH6 109.25 straddles, 33.5 vs. 109-24/0.85%

-2,000 TYJ6 112/115 call over risk reversals, 2.0

+5,000 TYJ6 109.5 puts, 2.0 vs. 113-03.5/0.08%

+2,600 USH6 117/116 put spds vs 118-03/0.05%

+2,500 TYH6 113.75 calls, 7

+3,000 FVJ6 108.25/108.75/109.25/109.50 broken put condors, 4

+2,500 TYM6 113 puts, 62 ref 113-05/0.35%

+5,000 TYJ6 110 puts, 2 vs. 113-04/0.03%

-1,900 TYJ6 113.5 straddles, 124-125

2,000 USH6 116.5 puts, 3 ref 118-00

+2,000 TYJ6 112.5 calls, 109 vs. 113-13.5/0.69%

+2,000 TYH6 113.5/113.75/114.5 broken call trees,1

MNI BONDS: EGBs-GILTS CASH CLOSE: Long-End Rally Continues

European long-end yields resumed their descent Tuesday as bull flattening continued.

- UK labour market data showed quantities data weaker than expected and compensation broadly in line, very much keeping a March BOE cut in play.

- February German ZEW expectations pulled back from January's four-year highs, but this was not a market mover.

- Early gains faded over the course of the session as equities found their footing, with Gilts retracing more than Bunds.

- For the day, the German and UK curves both bull flattened, with periphery/semi-core EGB spreads narrowing very modestly.

- Wednesday brings UK inflation data for January - MNI's preview is here. We also hear from the ECB's Villeroy, Cipollone, and Schnabel.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.5bps at 2.036%, 5-Yr is down 1.1bps at 2.328%, 10-Yr is down 1.6bps at 2.738%, and 30-Yr is down 2.7bps at 3.405%.

- UK: The 2-Yr yield is unchanged at 3.587%, 5-Yr is down 1bps at 3.797%, 10-Yr is down 2.3bps at 4.376%, and 30-Yr is down 2.5bps at 5.181%.

- Italian BTP spread down 0.1bps at 61.2bps / Spanish down 0.5bps at 37.8bps

MNI OPTIONS: Downside Plays Favoured In Euribor

Tuesday's Europe rates/bond options flow included:

- DUJ6 106.90/107.00/107.10c fly, bought for 1.75 up to 2 in 10k

- OEH6 117c vs OEJ6 118.50c, bought the April for -4 (receive) in 2k

- ERU6 98.06/98.00/97.87 broken p ladder, bought for 2.75 and 3 in 20k

- ERU6 97.75/97.62ps, bought for half in 10k

- ERZ6 98.06/97.93ps 1x2, bought for 2 in 10k

- ERZ7 98.50/99.00 call spread, bought for 4.5 in 20k

- 0RH6 97.9375/97.8125/97.75p fly, bought for 1.25 in 8k

- SFIM6 96.45/96.35/96.25p ladder, sold at 0.25 in 15.75k

- SFIM6 96.50/96.35ps 1x1.5, bought for 1.25 in 8k

- SFIZ6 96.85/97.00cs, bought for 5 in 10k vs SFIM6 96.45/96.60cs, sold at 11.5 in 4k

- 0NZ6 97.00/97.40 call spread, bought for 5.5 in +10k

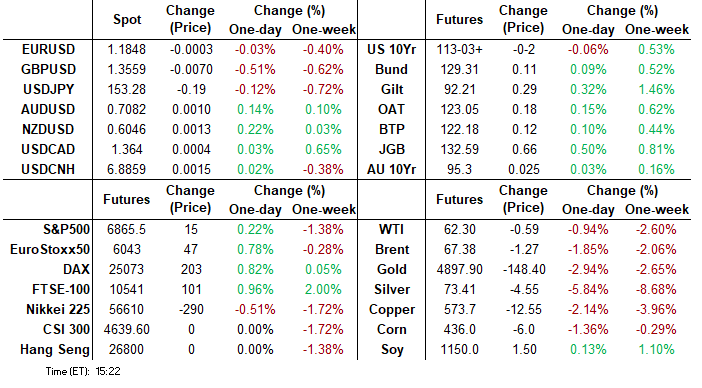

MNI FOREX: Notable GBP Weakness, USDJPY Reverses Firmly Higher

- Sterling weakness has been a key feature across the G10 FX space on Tuesday, price action that followed a softer-than-expected set of labour market data from the UK. Alongside a firmer dollar backdrop, GBPUSD is down 0.65% as we approach the APAC crossover, briefly slipping below 1.35.

- Today’s move lower has seen the pair breach the 50-day EMA, and a sustained break of this average would undermine the recent bull theme. Meanwhile, EURGBP has rallied over half a percent on the session, and in the process has pierced a key resistance point at 0.8746, the Jan 21 high. A clear break of this level would also highlight a potential trend reversal.

- Elsewhere, volatility for the Japanese yen has not abated, with USDJPY posting a 122pip range on the session. Initial strength for JGBs and waning risk sentiment prompted a move down for USDJPY to session lows of 152.70, however, the broader USD bid and eventual stabilising risk sentiment allowed the move to steadily reverse across the session, resulting in fresh highs at 153.92.

- Short-term USDJPY parameters appear well established; the January lows at 152.10 provide key support, while the post-NFP highs at 154.65 offer the most notable resistance.

- Downside momentum for EURUSD had also been steadily playing out across Tuesday’s session, with the latest weakness testing the lows from last Monday’s range, of which spot had been trading within over the past six sessions. A lower close for EURUSD today would represent a sixth consecutive session of declines. Akey support area for EURUSD combines both the Feb 06 low and the 50-day EMA, just below 1.1770.

- Aussie wage price index data and the RBNZ decision highlight the APAC data docket, before the focus turns to UK CPI on Wednesday. Later in the session, FOMC minutes will take the spotlight.

MNI OPTIONS: Expiries for Feb18 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1800-15(E1.2bln), $1.1850(E591mln), $1.1900-20(E2.1bln), $1.2000(E1.4bln)

- USD/CAD: C$1.3600($1.4bln)

- AUD/USD: $0.6980-00(A$1.4bln)

- USD/CAD: C$1.3600($1.4bln)

MNI US STOCKS: Late Equities Roundup: Late Recovery as US$ Pares Support

- US equity indexes have reversed course yet again Tuesday, with Financials and Information Technology sector shares leading advances in late trade.

- Currently, the DJIA trades up 140.4 points (0.28%) at 49640.88, S&P E-Mini Futures up 22.25 points (0.32%) at 6872.75, Nasdaq up 88.4 points (0.4%) at 22633.8.

- Bank and insurance company shares buoyed the Financial sector for the most part, tempered by weaker financial services shares as Bitcoin retreated -1.55% in late trade. IT sector shares were supported by hardware makers while weaker chip makers tempered overall sector gains.

- Energy and Materials sector shares leading the decline as crude oil and gold prices fell. Crude prices retreated after Reuters reporting comments from Iranian Foreign Minister Abbas Araghchi following the conclusion of a second round of indirect nuclear talks with the US in Geneva, Switzerland. Araghchi said, "We've reached an understanding on main principles with the US."

- Reminder, while the latest corporate earnings cycle is in it's final stretch (over 75% complete), a handful of companies are expected to report after today's close: Celanese Corp, Republic Services, Devon Energy Corp, Palo Alto Networks, Toll Brothers Inc, Caesars Entertainment and Kenvue Inc.

MNI EQUITY TECHS: E-MINI S&P: (H6) Key Support Remains Exposed

- RES 4: 7080.92 0.764 proj of the Nov 21 - Dec 11 - 18 price swing

- RES 3: 7055.42 2.0% Upper Bollinger Band

- RES 2: 7043.00 High Jan 28 and bull trigger

- RES 1: 6919.38/7011.50 50-day EMA / High Feb 11

- PRICE: 6836.00 @ 14:21 GMT Feb 17

- SUP 1: 6751.50 Low Feb 6 and key short-term support

- SUP 2: 6733.00 Low Nov 25 ‘25

- SUP 3: 6691.56 76.4% retracement of the Nov 21 - Jan 28 bull leg

- SUP 4: 6583.00 Low Nov 21 ‘25 and a key medium-term support

A sharp sell-off on Feb 12 in S&P E-Minis reinstates a potential bearish threat leaving key resistance at 7043.00, the Jan 28 high and bull trigger, intact for now. Attention turns to the key support at 6751.50, the Feb 6 low, where a break would highlight a top and a stronger short-term reversal. This would open 6691.56, a Fibonacci retracement point. Initial resistance to watch is at 6919.38, the 50-day EMA.

MNI COMMODITIES: Precious Metals, Crude Fall Amid US/Iran Optimism

- Precious metals have fallen further today, pressured by an upswing in the dollar index and some positive signals from today’s Iran/US talks.

- Spot gold is down by 2.0% at $4,894/oz, while silver has fallen by 3.7% to $73.8/oz.

- As a result, the gold/silver ratio has edged up to 66.2, rebounding further from the multi-year low of 43.4 on Jan 26.

- Analysts remain bullish on gold’s outlook, although from a technical perspective a bear threat remains present, with the sell-off from the Jan 29 high highlighting a potential top in the long-term trend.

- Initial support is at $4,655.7, the Feb 6 low, followed by $4,403.0, the Feb 2 low and bear trigger. On the upside, attention is on $5,139.9, a Fibonacci retracement level.

- Meanwhile, silver has traded through both the 20- and 50-day EMAs, signalling scope for a deeper retracement. Sights are on $61.136 next, a Fibonacci projection.

- Elsewhere, crude has fallen as the market remains focused on today’s more positive US-Iran negotiations.

- WTI Mar 26 is down by 0.8% at $62.4/bbl.

- Prices fell after Iran’s Foreign Minister Araghchi said an understanding had been reached on the main principles with the US and that there were ‘good developments’ compared to the last round of talks.

- Although a bull cycle in WTI futures remains intact, the move lower from the Jan 29 high continues to highlight a corrective phase. Support at the 20-day EMA, at $62.58, has been pierced. The 50-day EMA lies at $61.00.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 18/02/2026 | 0700/0700 | *** | Consumer Inflation Report (1dp) | |

| 18/02/2026 | 0700/0700 | *** | Consumer Inflation Report (2dp) | |

| 18/02/2026 | 0700/0700 | *** | Producer Prices | |

| 18/02/2026 | 0745/0845 | *** | HICP (f) | |

| 18/02/2026 | 0900/1000 | ECB Cipollone at ABI's Executive Committee Meeting | ||

| 18/02/2026 | 1000/0500 | * | CREA Existing Home Sales | |

| 18/02/2026 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 18/02/2026 | 1330/0830 | *** | Housing Starts | |

| 18/02/2026 | 1330/0830 | *** | Housing Starts | |

| 18/02/2026 | 1330/0830 | ** | Durable Goods New Orders | |

| 18/02/2026 | 1330/0830 | ** | Durable Goods New Orders | |

| 18/02/2026 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 18/02/2026 | 1415/0915 | *** | Industrial Production | |

| 18/02/2026 | 1700/1800 | ECB Schnabel Panel at Berlin-Brandenburg Academy of Sciences and Humanities | ||

| 18/02/2026 | 1800/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 18/02/2026 | 1800/1300 | Fed's Michelle Bowman | ||

| 18/02/2026 | 1900/1400 | *** | FOMC Minutes | |

| 18/02/2026 | 2100/1600 | ** | TICS | |

| 19/02/2026 | 2350/0850 | * | Machinery orders | |

| 19/02/2026 | 0030/1130 | *** | Labor Force Survey |