MNI ASIA MARKETS ANALYSIS: RBA Policy Ahead, US Data on Hold

HIGHLIGHTS

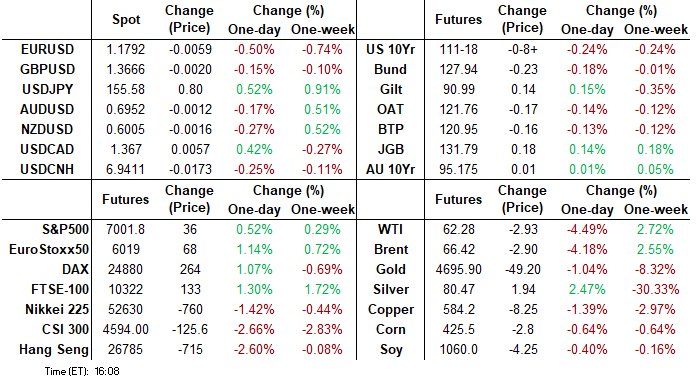

- Treasuries look to finish weaker Monday, reversing early gains to near session lows after stronger than expected ISM data for Jan jumped 4.7pts to 52.6 (highest since Aug '22, significantly above highest analyst estimate of 51.0).

- Note, due to the US Gov shutdown, Tuesday's JOLTS, Thursday's jobless claims & Friday's nonfarm payrolls (or QCEW revisions) will not be released

- US Treasury quarterly refunding estimates came out largely as expected though its cash pile to rise to $900B by end FYQ3 vs the standard $850B, raising borrowing requirements by $50B than they otherwise would have been.

- Tuesday's calendar is highlighted by the RBA decision, where a 25bp hike is expected by a majority of surveyed analysts, focus will be on how much follow up action the central bank sees as needed to ensure inflation returns to target.

US TSYS

MNI US TSYS: Delay of Data on Latest US Gov Shutdown

- Treasuries look to finish weaker, reversing early Monday gains after a surge in ISM data: far stronger than expected in January as it jumped 4.7pts to 52.6 for its highest since Aug 2022, significantly above even the highest analyst estimate of 51.0. New orders and production both surged to their highest since early 2022 - unlike the final PMI survey released shortly beforehand, it doesn’t look linked to an inventory build.

- The S&P Global US manufacturing PMI saw a sizeable upward revision in January from 51.9 in the flash to 52.4 in the final (cons 52.0) after 51.8 in Dec, for its highest since October. The press release notes strong production but also a contribution from inventory build. Highlights from the full release (link).

- Currently, TYH6 trades -8 at 111-18.5, continued weakness puts focus attention on the bear trigger at 111-09, the Jan 20 low. Conversely, the next important resistance to watch is 112-08+, the 50-day EMA. A clear break of the 50-day average is required to signal scope for a stronger recovery.

- For the Jan-Mar quarter, Treasury expects to borrow $574B (prior estimate was $578B; MNI's expectation was $575B) with a financing need of $530B.

- In terms of data it's already too late for Tuesday's JOLTS release to come out on time, and judging from the BLS's communications today, nonfarm payrolls will be postponed from Friday until an unknown future date (known only once the government is back open).

- The House Rules Committee is shortly due to begin consideration on a Senate-passed appropriations package for five government departments and a two-week funding extension for DHS. Successful passage of the measure will end a partial government shutdown that took effect at midnight on Friday.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.68% (+0.03), volume: $3.275T

- Broad General Collateral Rate (BGCR): 3.66% (+0.03), volume: $1.314T

- Tri-Party General Collateral Rate (TCR): 3.66% (+0.03), volume: $1.277T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.64% (+0.00), volume: $101B

- Daily Overnight Bank Funding Rate: 3.63% (+0.00), volume: $194B

FED Reverse Repo Operation

RRP usage inches up to $10.415B with 8 counterparties this afternoon vs. $9.629B Friday. Compares to December 12 low of $0.838B (lowest level since mid-March 2021); this years highest excess liquidity measure: $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury options leaned bullish Monday, fading the decline in underlying futures after strong ISM data. Projected rate cut pricing consolidating vs. late Friday levels (*): Mar'26 at -30bp (-4.3bp), Apr'26 at -6.9bp (-8.5bp), Jun'26 at -18.4bp (-21.1bp), Jul'26 at -26.9bp (-31bp).

SOFR Options:

+9,000 SFRH6 97.00/97.75 call strip, 0.75 ref 96.37

+10,000 SFRH7/SFRM7 97.25/97.50/97.75 call fly strip, 3.0 total

Block/SCREEN, +35,000 SFRM6 97.00 calls, 3.0 vs. 96.565/0.14%

+20,000 SFRM6 96.43/96.62/96.75 broken call trees, 3.5

+4,000 0QJ6 97.18/97.31 call spds, 1.0

Block, 5,000 0QM6 97.00/97.37/97.75 call flys, 4.0

2,500 SFRJ6 96.37/96.50 2x1 put spds ref 96.58

4,000 SFRH7 97.12/97.25 call spds ref 96.83

4,000 SFRM6 96.25 puts vs 96.62/96.87 call spds, 4.0 net ref 96.575

+4,000 0QG6 96.87/97.00 call spds, 2.5 ref

-2,000 SFRZ6 96.06/96.31/96.56 put flys, 5 ref 96.84

Treasury Options:

2,000 USJ6 117/119/120 broken call flys

3,000 TYH6 110/111 put spds

3,450 FVH6 108.5/108.75 3x2 put spds

over 25,000 FVH6 108.5 puts, 7 ref 108-23.75

+36,000 TUJ6 106.37 calls, 0.5 ref 104-07.5

20,000 FVJ6 108.5 puts, 20

Block, -5,000 USH6 114 puts, 31 vs. 115-04/0.32%

10,000 FVH6 108/108.5 2x1 put spds

3,300 TYH6 111/113 call over risk reversals, 2 net vs. 111-23.5/0.31%

+1,700 TYH6 115.75 calls, 2 ref 111-31.5

-1,600 TUH6 104.5/104.75 call spds, 1.5 ref 104-07.37/0.10%

-3,000 USH6 114 puts, 31 vs 115-07/0.37%

+2,500 tyh6 110.5/112.5 call over risk reversal, 14 vs. 112-00.5/0.43%

-2,000 TYH6 112 calls, 28 vs 112-01/0.36%

over 18,700 TYH6 111.5 puts, 14-13 ref 112-01

over 5,400 TYH6 113 calls, 10 ref 111-31.5 to 112-00

+2,150 TYJ6 113.5 calls, 14 ref 111-22.5

over +6,100 TYH6 112.5 calls, 12 ref 111-27

MNI BONDS: EGBs-GILTS CASH CLOSE: Gilts Outperform Bunds At Start Of Busy Week

Gilts outperformed Bunds at the start of a busy week for European risk events.

- EGBs and Gilts caught a bid early in a risk-off move after precious metals' price collapse Friday and equity weakness in Asia-Pac trade coming out of the weekend.

- Global bonds pulled back with US Treasuries after the day's key data point, ISM Manufacturing, had one of its largest upside surprises in decades.

- On the day, the German curve leaned bear flatter with the UK's slightly bull steeper.

- Periphery/semi-core EGB spreads were little changed, including BTPs after widening early despite Italy's ratings outlook getting revised to Positive from Stable by S&P on Friday.

- OATs, too, were largely unchanged; after the cash close France's parliament adopted a 2026 budget after no-confidence votes against the government failed (this had been expected).

- Focus remains on the January flash inflation data to come this week (including Eurozone on Wednesday) and of course the BOE and ECB decisions on Thursday.

Closing Yields / 10-Yr EGB Spreads To Germany:

- Germany: The 2-Yr yield is up 2.5bps at 2.114%, 5-Yr is up 3.1bps at 2.448%, 10-Yr is up 2.5bps at 2.868%, and 30-Yr is up 2.2bps at 3.516%.

- UK: The 2-Yr yield is down 1.5bps at 3.703%, 5-Yr is down 1.4bps at 3.936%, 10-Yr is down 1.6bps at 4.506%, and 30-Yr is down 1.2bps at 5.273%.

- Italian BTP spread up 0.1bps at 61.4bps / Spanish down 0.4bps at 36.5bps

MNI EGB OPTIONS: Euribor Call Flies Of Different Stripes

Monday's Europe rates/bond options flow included:

- SFIK6 96.60/96.75 call spread, bought for 2 in 10k

- ERK6 98.00/98.12/98.25 call fly paper paid 1 on 2.5K

- ERZ6 98.00/98.25/98.50 call fly paper paid 2.75 on 2K

- 0RZ6 97.87/98.00 call spread paper paid 4 on 11K

MNI FOREX: Firmer US Data Assists Extension of USD Rebound

- Despite some sharp moves lower for both precious metals and equities in early trade Monday, a subsequent recovery for risk has helped boost the US dollar, where sentiment has also been supported by a stellar set of US ISM manufacturing PMI data.

- The ISM manufacturing report was far stronger than expected in January as it jumped 4.7pts to 52.6 for its highest since Aug 2022, significantly above even the highest analyst estimate of 51.0. This has assisted the dollar index to extend intraday gains to around 0.5%, extending its recovery from last week’s cycle lows to over 2%.

- This has in turn weighed on EURUSD, which has today slipped back below 1.18, an impressive reversal from last week’s 1.2081 peak. Moves have met the primary objective for a pullback, that being 1.1793, the 20- day EMA. However, more meaningful support is at the 50-day EMA, which lies at 1.1729, important as we approach this week’s ECB decision and press conference.

- It’s the Swiss franc which has notably underperformed on Monday, with USDCHF (+0.95%) retaking the 0.78 handle and EURCHF rising back above 0.92. Given the de-risking that has been on display elsewhere since Friday, short-term positioning dynamics may be assisting the squeeze higher for cross/CHF, while some analysts have pointed to the depressed EURCHF levels as potentially ringing the alarm bells for the SNB.

- In emerging markets, US President Donald Trump said in a statement on Truth Social that he has agreed to lower the reciprocal tariff rate on India from 25% to 18% after agreeing a trade deal with Indian Prime Minister Narendra Modi. The announcement prompted USDINR 1-month NDFs to slip further on the session, currently down around 1.2%.

- News has crossed indicating both tomorrow’s US JOLTS data and Friday’s payrolls report will be rescheduled owing to the US Government shutdown. The calendar will be highlighted by the RBA decision, where a 25bp hike is expected by a majority of surveyed analysts.

MNI FX OPTIONS: Expiries for Feb03 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1850(E3.5bln), $1.1935-40(E2.5bln)

- USD/JPY: Y155.75($877mln)

- GBP/USD: $1.3200(Gbp835mln)

- USD/CAD: C$1.3590-00($913mln)

MNI US STOCKS: Late Equities Roundup: IT & Travel Shares Outperforming

- Stocks rebounded from early losses - drifting at or near near session highs late Monday as Consumer Discretionary and IT sector shares continued to outperform. Currently, the DJIA trades up 505.01 points (1.03%) at 49396.02, S&P E-Minis Future up 42 points (0.6%) at 7008, Nasdaq up 162.6 points (0.7%) at 23625.15.

- Leading advances in the second half include multiple hardware and semiconductor makers that rebound from last week's selling: Sandisk Corp +15.12%, Western Digital +8.90%, Intel Corp +5.94%, Seagate Technology +5.26% and Micron Technology +5.12%.

- Consumer Discretionary shares included luxury travel stocks: Carnival Corp +8.28%, Norwegian Cruise Line +7.19%, United Airlines Holdings +5.26% and Las Vegas Sands +5.16%.

- On the flipside, Energy shares led declines with crude prices off sharply (WTI -3.1 at 62.11) as middle east tensions cooled with Pres Trump's tone on Iran softening (while the carrier battle group remains in the region): EQT Corp -5.60%, Expand Energy -5.04%, ONEOK -4.17%, Diamondback Energy -3.41%, Coterra Energy -3.12% and Occidental Petroleum -3.06%.

MNI EQUITY TECHS: E-MINI S&P: (H6) Candle Patterns Highlight A Short-Term Bear Cycle

- RES 4: 7141.7 1.236 proj of the Dec 18 - Jan 13 - 21 price swing

- RES 3: 7100.00 Round number resistance

- RES 2: 7080.92 0.764 proj of the Nov 21 - Dec 11 - 18 price swing

- RES 1: 6965.75/7043.00 Intraday high / High Jan 28 and bull trigger

- PRICE: 6945.50 @ 14:25 GMT Feb 2

- SUP 1: 6864.50 Intraday low

- SUP 2: 6814.50 Low Jan 21 and the bear trigger

- SUP 3: 6771.50 Low Dec 18 and a key support

- SUP 4: 6684.50 Low Nov 24

The trend in S&P E-Minis is bullish and the pullback from last week’s high is considered corrective. However, note that a doji candle pattern on Jan 28 and a hammer candle on Jan 29, continues to signal scope for a deeper retracement near-term. Today’s initial move down reinforces the importance of these two patterns. A continuation lower would expose key S/T support at 6814.50, the Jan 21 low. The bull trigger is at 7043.00, the Jan 28 high.

MNI AMERICAS OIL: US OIL: February 2 - Americas End of Day Oil Summary: Crude Falls

WTI Oil prices fell amid a drop in Iran-related risks with negotiations between the US and Iran likely on Feb 6 in Istanbul. The underlying market narrative remains bearish due to a projected surplus, despite recent supply disruptions in the US and Kazakhstan.

- Axios reports that, according to two sources, US special envoy Steve Witkoff and Iranian Foreign Minister Abbas Araghchi will meet in Istanbul, Turkey, on Friday, 6 Feb.

- A global risk off sentiment also followed through into oil which began with the FED Chair announcement and weighing on key markets like precious metals.

- OPEC+8 as expected decided to maintain its pause in supply in March.

- Iran’s supreme leader warned of a regional war in the event of a US strike following the US miliary buildup in the region aimed at pushing Iran to negotiate on a new nuclear deal.

- Venezuela’s oil exports reached 800,000 bpd in January under US control – compared to 498,000 bpd the month prior LSEG reports.

- The next trilateral meetings between the US, Russia and Ukraine will be held on Feb. 4-5 as attacks on energy infrastructure have been paused for now.

- WTI Mar futures were down 4.7% at $62.14

- WTI Apr futures were down 4.6% at $61.76

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 03/02/2026 | 0700/0200 | * | Turkey CPI | |

| 03/02/2026 | 0745/0845 | *** | HICP (p) | |

| 03/02/2026 | 0745/0845 | Budget Balance | ||

| 03/02/2026 | 0900/1000 | ** | ECB Bank Lending Survey | |

| 03/02/2026 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 03/02/2026 | 1300/0800 | Richmond Fed's Tom Barkin | ||

| 03/02/2026 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 03/02/2026 | 1500/1000 | *** | JOLTS jobs opening level | |

| 04/02/2026 | 2200/0900 | * | S&P Global Final Australia Services PMI | |

| 04/02/2026 | 2200/0900 | ** | S&P Global Final Australia Composite PMI | |

| 04/02/2026 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 04/02/2026 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 04/02/2026 | 0145/0945 | ** | S&P Global Final China Services PMI | |

| 04/02/2026 | 0145/0945 | ** | S&P Global Final China Composite PMI |