MNI ASIA MARKETS ANALYSIS: Pres Trump Trolls Chair Powell

HIGHLIGHTS

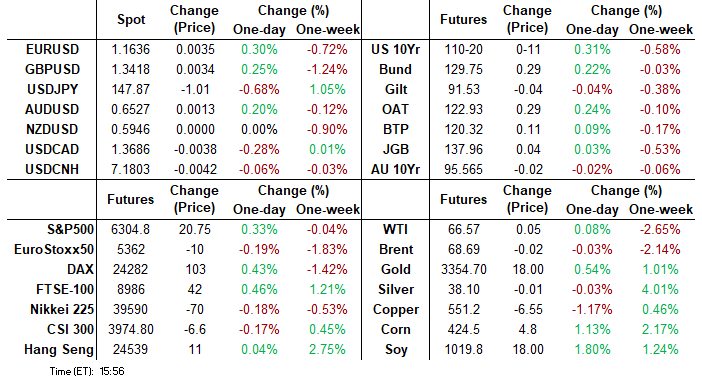

- Treasuries looked to finish near late session highs, early support after after lower than expected PPI inflation measures leavened by up-revisions for May data.

- Tsys largely ignored midmorning headlines suggesting Pres Trump would fire Fed Chair Powell - though US$ and Equities sold off on the chatter.

- Stocks rebounded, extended modest session highs after Trump denied the rumors (unless cause found under pretense of funds misuse for Fed headquarter renovation).

- Focus on Thursday's weekly claims and retail sales data, several scheduled Fed speakers ahead of late Friday's policy blackout.

US TSYS

MNI US TSYS: Curves Steepen to New 4+ Year Highs, Pres Trump Trolls Chair Powell

- Treasuries look to finish near moderate late session highs, early support after lower than expected PPI inflation measures leavened by up-revisions to May reads. The main headline reading was flat PPI % M/M (0.01% unrounded), vs expectations of a 0.2% rise (though this was offset by an upward revision to May, to 0.30% from 0.13%). That left Y/Y PPI at the softest level (2.3%) since September 2024, and down from 2.7% in May.

- Industrial production rose by 0.3% M/M in June (0.1% expected), a figure that looks even more solid when considering the upward revision to prior (May 0.0%, albeit very slightly negative unrounded at -0.03%, rev from -0.2%). Capacity utilization unexpectedly rose to 77.6% (expected unchanged at 77.4%, rev up to 77.5% in May).

- Tsys pared gains after headlines that Pre Trump asked GOP lawmakers if he should fire Fed Chairman Powell now - before the end of his term in May 2026. US$ and equities reacted more sharply, both selling off on the chatter before rebounding late morning after Trump denied reports of an imminent termination of the Fed Chair (unless cause found under pretense of funds misuse for Fed headquarter renovation).

- Currently, Sep'25 10Y contract trades +11 at 110-20 vs. 110-21.5 high. Initial technical resistance above at 111-01 (20-day EMA). Support below at 110-08.5 (Low Jul 14). Curves bounced off lows on wide ranges: 2s10s +2.641 at 56.381; 5s30s +4.649 at 102.55p vs. 107.895 high - highest intraday level since October 2021.

- Focus turns to Thursday's weekly jobless claims, Retail Sales, Import/Export Prices and TIC flows as well as several Fed speakers ahead the start of late Friday's policy Blackout.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.37% (+0.04), volume: $2.784T

- Broad General Collateral Rate (BGCR): 4.36% (+0.04), volume: $1.131T

- Tri-Party General Collateral Rate (TCR): 4.36% (+0.04), volume: $1.107T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $101B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $252B

FED Reverse Repo Operation:

RRP usage slips to $197.086B this afternoon from $198.277B yesterday, total number of counterparties at 35. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021 - compares to July 1: $460.731B highest usage since December 31.

US SOFR/TREASURY OPTION SUMMARY

With a few exceptions, SOFR & Treasury options saw better call volumes carry over from overnight, huge Green Mar'26 SOFR Call spd add (+200k/wk) and not a particularly useful buy of 100k way-out of the money TYQ5 calls at sub-cab levels. Underlying futures remain firmer/near session , projected rate cut pricing gain slightly vs this morning's pre-data (*) levels: Jul'25 at -0.6bp, Sep'25 at -15.2bp (-14.2bp), Oct'25 at -28.6bp (-27.1bp), Dec'25 at -46.8bp (-43.7bp).

SOFR Options:

+150,000 2QH6 98.00/98.25 call spds .87 (adds to +50k on Monday for 1.0)

+6,000 SFRZ5 95.87/96.06/96.18/96.31 put condors, 0.0 vs. 96.6/0.10%

Block/pit, -10,000 SFRZ5 96.25/96.50/96.75/97.00 call condors, 3.75

2,500 SFRZ5 95.62/95.75/95.87 put flys, ref 96.08

-19,750 SFRQ5 95.68/95.75 put spds 1.25 ref 95.815

Block/screen, +20,000 SFRH6 96.37/96.50 call spds vs. 96.00/96.12 put spds, 0.5 net vs. 96.31/0.15%

1,000 SFRU5 95.68/95.75/95.872x3x1 broken put flys ref 95.815

Treasury Options:

-100,000 TYQ5 115.5 calls, cab-7

over -60,000 TYU5 107/108 put spds, 5 ref 110-15.5

2,100 USQ5 111/111.5 put spds, 9 ref 112-20

2,500 TYQ5 107.5/108.5 2x1 put spds ref 110-18

9,100 TYV5 109 puts 41 ref 110-13.5

Block, 7,500 TYV5 108 puts, 25 vs. 110-14/0.20%

Block, 7,500 TYV5 108/TYX5 107.5 put spds, 3 vs. 110-16/0.56

+5,000 TYU5 113/115 1x2 call spds, 2 vs. 110-12.5/0.05%

-2,500 TUU5 103.25 puts, 5.5

+15,000 TYU5 115 calls, 3

+10,000 TYU5 115.5 calls, 3

+5,000 TYU5 108/109 put spds, 11

Block/screen over +47,000 TYU5 108.5/109.5 put spds 16 vs. 110-10/0.15%

2,500 TUU5 103.12/103.37/103.5/103.62 broken put condors, 0.5 net ref 103-17.12

-3,000 TYQ5 109.75/110.75 call over risk reversals, 0.0

4,300 TYV5 111/112 call spds ref 110-08

4,250 TYQ5 110.5 calls ref 110-12

MNI BONDS: EGBs-GILTS CASH CLOSE: Gilts Underperform Post-CPI, Pre-Labour Data

Bunds outperformed Gilts Wednesday following firmer-than-expected UK inflation data.

- Gilt yields gapped higher on the open, following UK June CPI coming in above consensus on most measures.

- But the move faded somewhat as the report was digested, with the broader scope of the report not significantly differing from the BOE's existing expectations for inflation developments (and greater focus anyhow on upcoming labour market data).

- In early afternoon trade, global core FI rallied as US PPI data came in on the soft side

- Volatility picked up toward the cash close on reports that US President Trump planned to soon fire Federal Reserve Chair Powell. This saw long-end yields rise again but Trump's denial made just before the European cash close saw Gilt and Bund yields have a final dip.

- The German curve leaned bull steeper on the day, with the UK's leaning bear flatter - the belly outperformed on both curves.

- Periphery/semi-core EGB spreads were little changed.

- Thursday's highlight is the UK labour market report - our preview is here. The main focus this month will be on a combination of private regular average earnings and the notoriously revised payrolls numbers.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 2.7bps at 1.86%, 5-Yr is down 3.3bps at 2.23%, 10-Yr is down 2.5bps at 2.687%, and 30-Yr is down 1.2bps at 3.214%.

- UK: The 2-Yr yield is up 1.9bps at 3.855%, 5-Yr is up 1.1bps at 4.042%, 10-Yr is up 1.4bps at 4.639%, and 30-Yr is up 1.1bps at 5.469%.

- Italian BTP spread down 0.4bps at 85.6bps / French OAT down 0.2bps at 69.8bps

MNI EGB OPTIONS: Slew Of Sonia Trades Between CPI And Labour Data

Wednesday's Europe rates/bond options flow included:

- RXQ5 129.50/129 put spread paper paid 17 on 3.5K

- RXQ5 129 puts at 32 vs. RXV5 127 puts at 74.5-76.5 10K trades, selling the Q to buy the V, potentially rolling an existing position down and out

- ERU5 98.1875/98.25 1x2 call spread, paper pays 1 on 3.5k

- ERH6 98.25/98.00 put spread 5K given at 10.5 vs. 98.22.

- SFIU5 96.15/96.10/96.05 put ladder paper paid 0 on 2K, 8K trades all day

- SFIZ5 95.75/96.00/96.25 call fly 5.5K given at 4.5

- SFIZ5 96.30/96.15/96.00 put fly 3K sold at 2

- SFIZ5 96.50/96.80 call spread, bought for 4.75 in 3k

MNI FOREX: Very Volatile USD Swings as Trump Headlines on Fed Chair Dominate

- Initial price action on Wednesday saw the US dollar extend its cautious recovery, underpinned by prior US inflation data which showed signs of increasing passthrough to consumer prices from tariffs. However, volatile greenback swings then ensued as headlines surrounding President Trump’s potential intentions to fire Fed Chair Powell dominated global markets.

- Initial reporting suggested that President Trump indicated to Republican lawmakers that he will "likely" fire Federal Reserve Chair Jerome Powell soon, after receiving approval from them to make the move, a senior White House official told journalists. This prompted a severe reversal lower for the dollar, with the DXY dropping as much as 1.15% as short-term greenback longs were swiftly pressured. Alongside downside pressure for both equities and front-end US yields, USDJPY rapidly sold off to an intra-day low of 146.92, around 225 pips off the overnight highs.

- However, shortly after the significant greenback selloff Trump addressed journalists in the White House - appearing alongside PM of Bahrain – where he appeared to downplay these rumours, stating he was not planning on firing the Fed Chair and that reports of drafting a letter to fire Jerome Powell aren’t true.

- The USD snapped sharply higher as a result, although the USD index remains ~0.25% lower on the session ahead of the APAC crossover amid the heightened lingering uncertainty. USDJPY settled just above the 148 mark, down ~0.5% on the session.

- EURUSD has been equally volatile, trading a 1.1563-1.1721 range. The pair currently operates around 1.1640 as markets digest the latest developments in the US. The move down in recent sessions appears corrective and trend signals continue to highlight a dominant uptrend.

- A quick mention to GBPUSD which had a very limited reaction to firmer-than-expected CPI data on Wednesday. Late currency volatility also had less of an impact on GBP, ahead of key labour market data due Thursday. A close at current levels (1.3420) would keep the focus on the most recent breach of trendline support, drawn from the January lows.

- Elsewhere, Australian employment data and US retail sales will be highlights on the global calendar.

MNI FX OPTIONS: Expiries for Jul17 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500-10(E1.9bln), $1.1525-40(E1.1bln), $1.1585-00(E1.3bln), $1.1600(E1.1bln), $1.1650-55(E1.1bln) $1.1700(E1.4bln), $1.1750-70(E1.4bln);

- USD/JPY: Y147.00($1.0bln), Y148.00($704mln), Y148.95-00($1.7bln)

- GBP/USD: $1.3425(Gbp500mln), $1.3445-60(Gbp1.2bln)

- EUR/JPY: Y171.00-20(E930mln)

- USD/CNY: Cny7.1691-05($549mln)

MNI US STOCKS: Late Equities Update: You're Fired! Just Kidding

- Stocks have fully recovered from a midday sell-off after Pres Trump denied reports of an imminent termination of Fed Chair Powell (term ends May 2026) - unless cause found under the pretext of misuse of funds for Fed headquarter renovation.

- Currently, the DJIA trades up 122.57 points (0.28%) at 44145.79 (43758.98 low), S&P E-Minis up 10.75 points (0.17%) at 6294.5 (6241.0 low), Nasdaq up 17.4 points (0.1%) at 20693.61 (20507.06 low).

- A mix of Health Care, Financial Services and Media sector shares led second half gainers: Johnson & Johnson +6.03%, Global Payments +5.15%, Warner Bros Discovery +4.70%, Omnicom Group +4.17%, Coinbase Global +3.86%, Interpublic Group +3.80%, Apollo Global Management +3.51% and Tesla +3.38%.

- On the flipside, Energy, Industrial and Consumer Discretionary sector shares underperformed in second half trade: Micron Technology -3.37%, Constellation Energy -3.34%, Universal Health Services -3.33%, Valero Energy -3.29%, Vistra -3.28%, Ford Motor -3.11%, Best Buy Co -2.95% and Phillips 66 -2.87%.

- Earnings expected after the close: Rexford Industrial Realty, Alcoa Corp, United Airlines Holdings Inc and Kinder Morgan Inc. Earning expected Thursday: PepsiCo, Marsh & McLennan Cos Inc, Abbott Laboratories, Elevance Health Inc, US Bancorp, Cintas Corp, General Electric Co, Citizens Financial, Fifth Third Bancorp, Interactive Brokers Group and Netflix.

MNI EQUITY TECHS: E-MINI S&P: (U5) Trading Closer To Its Recent Highs

- RES 4: 6402.44 1.382 proj of the May 23 - Jun 11 - 23 price swing

- RES 3: 6381.00 1.764 proj of the Apr 7 - 10 - 21 price swing

- RES 2: 6356.12 1.236 proj of the May 23 - Jun 11 - 23 price swing

- RES 1: 6343.00 High Jul 15

- PRICE: 6297.50 @ 14:35 ET Jul 16

- SUP 1: 6246.25 Low Jul 7

- SUP 2: 6218.56/6073.00 20- and 50-day EMA values

- SUP 3: 5811.50 Low May 23

- SUP 4: 5645.75 Low May 7

S&P E-Minis are trading in a range, closer to their recent highs. The trend condition remains bullish. Recent activity has resulted in a break of resistance at 6128.75, the Jun 11 high. The breach confirmed a resumption of the uptrend that started Apr 7. This was followed by a break of key resistance and a bull trigger at 6277.50, the Feb 21 high. Sights are on 6356.12, a Fibonacci projection. Key support is at the 50-day EMA, at 6073.00.

MNI COMMODITIES: Gold Rallies Amid Uncertainty On Fed Chair Powell, Crude Steady

- Spot gold has pared gains, but is still 0.8% higher on the session at $3,352/oz, as uncertainty remains over the position of Fed Chair Powell.

- Initial headlines suggested that President Trump will likely fire Powell soon, prompting a severe reversal lower for the dollar and spike in gold to $3,377.

- However, Trump later appeared to downplay these rumours, prompting the yellow metal to pare today’s gains.

- A bull cycle in gold that started Jun 30 remains intact, with sights on $3,395.1, the Jun 23 high. On the downside, first support to watch is $3,282.8, the Jul 9 low.

- Meanwhile, copper has fallen by 1.1% to $552/lb, as inventories in Asia rose ahead of the tariff deadline.

- Copper futures are holding on to the bulk of their recent gains, reinforcing the current uptrend. Sights are on a retest of $589.55, the Jul 8 high. Key short-term support has been defined at $497.25, the Jul 8 low.

- Crude markets unwound earlier losses after EIA data showed a larger than expected fall in stocks this week, down 3.9m bbl compared to the forecast 0.67m bbl.

- WTI Aug 25 is broadly unchanged at $66.5/bbl.

- WTI futures maintain a bearish tone, with support to watch at $65.54, the 50-day EMA, a clear break of which would expose $58.87, the May 30 low. Initial resistance is $71.20, the 50.0% retracement of the Jun 23 - 24 high-low range.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 17/07/2025 | 0600/0700 | *** | Labour Market Survey | |

| 17/07/2025 | 0900/1100 | *** | HICP (f) | |

| 17/07/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 17/07/2025 | - | ECB Cipollone At G20 Meeting | ||

| 17/07/2025 | 1230/0830 | *** | Jobless Claims | |

| 17/07/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 17/07/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/07/2025 | 1230/0830 | *** | Retail Sales | |

| 17/07/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 17/07/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 17/07/2025 | 1230/0830 | *** | Retail Sales | |

| 17/07/2025 | 1400/1000 | * | Business Inventories | |

| 17/07/2025 | 1400/1000 | ** | NAHB Home Builder Index | |

| 17/07/2025 | 1400/1000 | * | Business Inventories | |

| 17/07/2025 | 1400/1000 | Fed Governor Adriana Kugler | ||

| 17/07/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 17/07/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 17/07/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 17/07/2025 | 1645/1245 | San Francisco Fed's Mary Daly | ||

| 17/07/2025 | 1730/1330 | Fed Governor Lisa Cook | ||

| 17/07/2025 | 2000/1600 | ** | TICS | |

| 17/07/2025 | 2230/1830 | Fed Governor Christopher Waller | ||

| 18/07/2025 | 2330/0830 | *** | CPI |