MNI ASIA MARKETS ANALYSIS: JOLTS Jobs Jump Ahead ADP & NFP

HIGHLIGHTS

- Treasuries scaled back early Tuesday session support after higher than expected JOLTS job openings and up-revision to prior openings.

- Treasury curves flattened with the short end leading the reversal while rate cut pricing retreated with less than two 25bp rate cuts projected by year end.

- Stocks pared gains late. S&P eminis off May 29 highs after the WH announced Pres Trump will sign 50% steel & aluminum import tariffs Wednesday. Unfounded Trump-Xi Friday call rumor had buoyed stocks briefly.

MNI US TSYS: Yields Rise as JOLTS Job Openings Jump, Rate Cut Pricing Cools

- Treasuries look to finish steady (10s) to mixed Tuesday, well off early session highs after higher than expected JOLTS job openings and up-revision to prior openings.

- The JOLTS report for April was on balance one of relative stability in another look at early reaction to Trump administration policies. Job openings surprisingly increased (7391k (sa, cons 7100k) in April after a marginal upward revised 7200k (initial 7192k) in March) whilst the hire rate pushed to its highest since September although the quits rate pushed back lower again after what to us was a surprising uptick back in March.

- Reminder, ADP private employ data schedule for 0815ET tomorrow, not to mention May employment report thjis Friday at 0830ET.

- Stocks pared gains late. S&P eminis off May 29 highs after the WH announced Pres Trump will sign 50% steel & aluminum import tariffs Wednesday. Unfounded Trump-Xi Friday call rumor had buoyed stocks briefly.

- Atlanta Fed President Bostic on Tuesday reiterated his view expressed in the March Dot Plot that he expects one rate cut later this year. Meanwhile, Fed Governor Lisa Cook said the U.S. economy faces heightened risks of both higher inflation and a weaker job market, and the current level of interest rates leaves the Federal Reserve in a good place to respond if either threat materializes.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.35% (+0.00), volume: $2.771T

- Broad General Collateral Rate (BGCR): 4.32% (-0.02), volume: $1.080T

- Tri-Party General Collateral Rate (TCR): 4.32% (-0.02), volume: $1.046T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $105B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $228B

FED Reverse Repo Operation

RRP usage rebounds to $153.177B this afternoon from $135.841B yesterday, total number of counterparties at 34. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

US SOFR/TREASURY OPTION SUMMARY

Trading desks reported better downside SOFR & Treasury put flow Tuesday as underlying futures reversed early gains, trade weaker/near second half lows. Projected rate cut pricing retreats vs. morning levels (*) as follows: Jun'25 at -0.3bp (-1.2bp), Jul'25 at -6bp (-6.3bp), Sep'25 at -20.3bp (-22.2bp), Oct'25 at -33bp (-35.8bp), Dec'25 at -48.7bp (-52.6bp).

SOFR Options:

Update, +26,000 SFRZ5 95.37/95.62 put spds, 1.12-1.25 ref 96.15

+10,000 SFRU5 95.93 calls, 13.5 ref 95.92

+15,000 SFRZ5 97.00/98.00 call spds, 5.25 ref 96.16

+7,000 SFRZ5/SFRH6 95.68/95.81 put spd spd .87 net/Dec over

+20,000 SFRN5 96.75/96.87 call spds, cab

+10,000 0QM5 96.87/97.12 call spds, 1.5 ref 96.58

-5,000 0QZ5 96.75 straddles, 68.5-68.0

-6,000 SFRU5 95.81 puts 3.0 over SFRZ5 95.75 puts

+5,000 SFRZ5 95.75/95.87/96.00 put flys, 1.5 ref 96.185

-1,000 0QZ5 96.75 straddles, 68.5 ref 96.745

1,800 2QM5 96.37/96.50/96.62 put flys

+1,500 SFRZ5 96.50/96.6875/96.75 call fly, 3.0 vs 96.22/0.05%

+1,500 0QQ5 95.75/96.00 put spd, 1.5

-1,500 SFRZ5 95.62/95.68 put spd, 0.5 vs 96.245/0.05%

Block, +5,000 0QM5 96.12/96.37 put spds, 2.0 ref 96.595

2,000 0QM5 96.62/96.75/96.87 call fly, 2.0

+10,000 SFRU5 95.625 puts, 1.0

Treasury Options:

over +28,500 TYN5 110.5 puts, 37, total volume over 39,500 ref 110-18.5/0.48%

4,000 TYN5 110.5/110.75 strangle w/ 110.25/111 strangle. 1.63 net 110-19.5

3,000 TYN5 110.5 straddles, 115

+5,000 TUN5/TUQ5 104.5 call spds, 4 (Aug over) ref 103-21.88

3,000 TYQ5 109/112 strangles, 102

+2,500 wk1 Wed TY 110.25 puts, 2

1,150 FVN5 107 puts, 5.5 ref 108-06.25

+1,000 wk1 Wed TY 110.5/110.75 2x1 put spd, 1.0 vs 110-26/0.08%

+1,000 wk1 TU/wk1 Wed TU 103.87 call spds, 2.5

+1,000 wk1 TU/wk1 Wed TU 103.75 call spds, 3.5

MNI BONDS: EGBs-GILTS CASH CLOSE: Late Selloff Obscures Constructive Session

Core EGB / Gilt yields erased much of their early drop late in the session Tuesday.

- An early bid stemmed in part from a strong 10Y JGB auction overnight (recall, weak long-end Japan dynamics had weighed in previous sessions), with Dutch inflation likewise on the weak side bringing down Eurozone-wide HICP, and some pointing to the OECD's global growth forecast cuts / collapse of the Netherlands Government as supportive.

- Global FI softened throughout the rest of the day, with rising equities and oil, and EUR supply weighing.

- After looking to finish with decent gains, Bunds and Gilts sold off in the minutes before the European cash close with no clear catalyst, some identifying an (apparent) rumour that US Pres Trump was scheduled to call China's Xi on Friday.

- The German curve twist steepened, with the UK's bull flattening. One takeaway from the BOE's TSC hearing was that Deputy Gov Breeden positioned herself as a little more dovish than Gov Bailey.

- Periphery / semi-core EGB spreads closed mixed, with 10Y BTPs at the tightest closing levels to Bunds since April 2021.

- Wednesday brings final Services PMIs. The ECB decision Thursday is the week's main event - MNI's preview is here. Along with the expected 25bp cut, focus will be on any clues around the willingness or lack thereof to highlight a potential pause in July.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.3bps at 1.786%, 5-Yr is down 0.1bps at 2.082%, 10-Yr is up 0.1bps at 2.525%, and 30-Yr is up 0.5bps at 3.017%.

- UK: The 2-Yr yield is down 0.1bps at 4.028%, 5-Yr is down 2bps at 4.143%, 10-Yr is down 2.9bps at 4.638%, and 30-Yr is down 4.3bps at 5.367%.

- Italian BTP spread down 0.6bps at 97bps / French OAT up 0.6bps at 67bps

MNI OPTIONS: Selling Out Euribor Call Condor Pre-ECB

Tuesday's Europe rates/bonds options flow included:

- ERM5 97.875/98.00/98.125/98.25 call condor, sold out at 11 in 10k

- SFIQ5 95.95/95.90/95.80p ladder, bought for 1.25 in 5k

- SFIU5 95.85/95.75/95.65p fly, bought for 1.25 in 2k

- SFIZ5 96.30/96.50 call spread vs 2NZ5 96.60/96.80 call spread, paper pays 1.75 for 4k

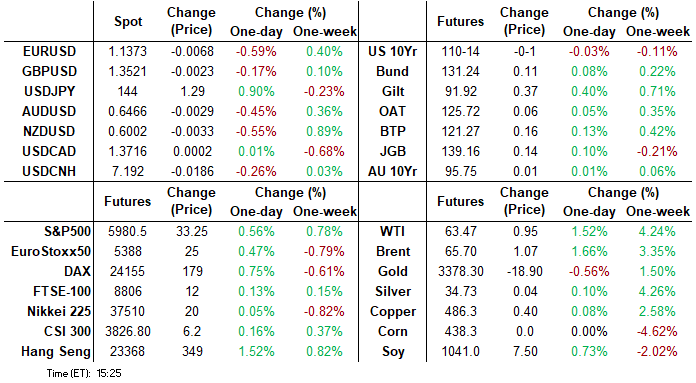

MNI FOREX: USD Bounces Back, US Data & Firmer Equities Provide Additional Tailwinds

- The USD underwent a mild corrective bounce early Tuesday, reversing a small part of the Monday underperformance as catalysts for a further phase of USD weakness dried up somewhat. Firmer US data and a constructive tone for major equity benchmarks then provided additional tailwinds for the greenback, leaving the USD index roughly 0.5% higher as we approach the APAC crossover.

- US JOLTS job openings came in above expectations, and despite the data potentially providing a stale view of the US labour market, the data spurred a more protracted intra-day recovery for the dollar. This prompted the likes of USDJPY(+0.88%) to extend its bounce to over 1% from session lows, and close back in on the 144 handle. In similar vein, USDCHF has rallied back to 0.8240 up 0.77% on the session. While the Swiss CPI data was in line with expectations, it did confirm that annual inflation slipped below the central bank’s target range at -0.1% Y/y.

- The Euro has traded on the backfoot as below expectation Eurozone inflation data may also be weighing on the single currency ahead of this week’s ECB meeting. The ECB’s June macroeconomic projections will be key in shaping the initial market reaction to Thursday’s policy statement, given a 25bp rate reduction is unanimously expected.

- EURUSD has spent the US session consolidating back below the 1.14 mark. In terms of support, the 20-day EMA provides short-term significance on a closing basis and currently intersects at 1.1316.

- After being among the best performing currencies on Monday, the likes of AUD and NZD have given up a solid portion of those advances today, as the relief rally for the greenback extends, and weighs on antipodean FX. For AUDUSD, that’s another test/rejection of the 0.6500 handle, a level spot has been unable to close above this year despite several tests of the psychological mark.

- Australian GDP highlights Wednesday’s APAC calendar, before the Bank of Canada decision later in the session. US ADP and ISM Services PMI are other notable data points.

MNI FX OPTIONS: Expiries for Jun04 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1200(E1.5bln), $1.1250(E885mln), $1.1350-55(E1.2bln), $1.1400-05(E1.1bln), $1.1450(E1.3bln)

- USD/JPY: Y143.50($698mln), Y144.15-25($580mln), Y145.00($630mln)

- AUD/USD: $0.6435-55(A$1.7bln)

- USD/CAD: C$1.3600($560mln), C$1.3735-50($1.4bln), C$1.3800($621mln)

MNI US STOCKS: Late Equities Roundup: IT & Energy Sector Shares Lead Gainers

- Stocks continue to trade in positive territory late Tuesday, paring gains after the White House announced Pres Trump will sign 50% steel & aluminum import tariffs Wednesday. Unfounded Trump-Xi Friday call rumor had buoyed stocks briefly.

- Currently, the DJIA trades up 236.32 points (0.56%) at 42541.49, S&P E-Minis up 34.75 points (0.58%) at 5982, Nasdaq up 163.1 points (0.8%) at 19405.76.

- S&P eminis had climbed to the highest level since May 29 earlier while Information Technology and Energy sectors continued to outperform. Leading gainers in the IT sector included ON Semiconductor +9.03%, Microchip Technology +5.68%, First Solar +5.29%, Enphase Energy +5.23% and Arista Networks +5.11%.

- Oil and gas shares buoyed the Energy sector as crude prices remained stronger but off highs (WTI +0.90 at 63.42): APA +5.48%, Diamondback Energy +3.56%, Occidental Petroleum +3.31% and Devon Energy +3.05%.

- On the flipside, interactive media and entertainment weighed on the Communication sector with Charter Communications -1.47%, Live Nation Entertainment -1.28% and Alphabet -0.88%.

- Meanwhile, the Consumer Staples sector was weighed down by Kenvue -6.21%, Bunge Global -2.03%, Kroger -1.70% and Archer-Daniels-Midland -1.23%.

MNI EQUITY TECHS: E-MINI S&P: (M5) Bull Cycle

- RES 4: 6124.00 High Feb 24

- RES 3: 6080.75 High Feb 26

- RES 2: 6057.00 High Mar 3

- RES 1: 6008.00 High May 29

- PRICE: 5980.00 @ 1225 ET Jun 3

- SUP 1: 5836.99/5756.81 20- and 50-day EMA values

- SUP 2: 5596.00 Low May 7

- SUP 3: 5455.50 Low Apr 30

- SUP 4: 5355.25 Low Apr 24

The trend condition in S&P E-Minis is unchanged and remains bullish. Recent gains delivered a print above 5993.50, the May 20 high and a bull trigger. The break highlights a resumption of the uptrend and maintains a price sequence of higher highs and higher lows. 6000.00 has been pierced, an extension would open 6057.00 next, the Mar 3 high. Key support lies at 5756.81, the 50-day EMA. A clear break of this average is required to highlight a reversal.

MNI COMMODITIES: Crude Rises Amid Iran Deal Uncertainties, Gold Pulls Back

- Crude front month is ending the day higher after mixed reports on an Iran deal, coupled with wildfires affecting Canadian production.

- WTI Jul 25 is up by 1.5% at $63.5/bbl.

- Iran’s foreign minister cast doubts on a US/Iran nuclear deal, resulting in crude prices finding further support on Tuesday, although Reuters later reported a NYT article saying that the US is proposing an interim step in the Iran deal to allow some enrichment.

- WTI futures are in consolidation mode but remain closer to their recent highs. A bear threat remains present and the recovery since Apr 9, appears corrective.

- Key resistance at $62.51, the 50-day EMA, has been pierced again. A clear break of it would highlight a stronger reversal and open $65.82, the Apr 4 high.

- Meanwhile, spot gold has fallen by 0.8% to $3,355/oz today, pulling back from its highest levels since May 9 around $3,392 earlier in the session.

- A bullish theme in gold remains intact, with moving average studies in a bull-mode position, highlighting a dominant uptrend.

- A continuation higher would open $3,435.6 next, the May 7 high.

- On the downside, key support and the bear trigger to watch has been defined at $3,121.0, the May 15 low.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 04/06/2025 | 0700/0900 | ** | Industrial Production | |

| 04/06/2025 | 0715/0915 | ** | S&P Global Services PMI (f) | |

| 04/06/2025 | 0715/0915 | ** | S&P Global Composite PMI (final) | |

| 04/06/2025 | 0745/0945 | ** | S&P Global Services PMI (f) | |

| 04/06/2025 | 0745/0945 | ** | S&P Global Composite PMI (final) | |

| 04/06/2025 | 0750/0950 | ** | S&P Global Services PMI (f) | |

| 04/06/2025 | 0750/0950 | ** | S&P Global Composite PMI (final) | |

| 04/06/2025 | 0755/0955 | ** | S&P Global Services PMI (f) | |

| 04/06/2025 | 0755/0955 | ** | S&P Global Composite PMI (final) | |

| 04/06/2025 | 0800/1000 | ** | S&P Global Services PMI (f) | |

| 04/06/2025 | 0800/1000 | ** | S&P Global Composite PMI (final) | |

| 04/06/2025 | 0830/0930 | ** | S&P Global Services PMI (Final) | |

| 04/06/2025 | 0830/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 04/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 04/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 04/06/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 04/06/2025 | 1215/0815 | *** | ADP Employment Report | |

| 04/06/2025 | 1230/0830 | Atlanta Fed's Raphael Bostic | ||

| 04/06/2025 | 1345/0945 | *** | Bank of Canada Policy Decision | |

| 04/06/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 04/06/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 04/06/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 04/06/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 04/06/2025 | 1430/1030 | BOC press conference | ||

| 04/06/2025 | 1800/1400 | Fed Beige Book | ||

| 05/06/2025 | - | European Central Bank Meeting | ||

| 05/06/2025 | 2330/0830 | ** | average wages (p) | |

| 05/06/2025 | 0130/1130 | ** | Trade Balance | |

| 05/06/2025 | 0145/0945 | ** | S&P Global Final China Services PMI | |

| 05/06/2025 | 0145/0945 | ** | S&P Global Final China Composite PMI |