MNI ASIA MARKETS ANALYSIS: Broad Rally As Hormuz "Opens"

MNI (NEW YORK) -

HIGHLIGHTS:

- Treasuries and equities rallied strongly Friday as it appeared the US and Iran could reach a peace deal in the coming days

- Energy prices fell sharply on Iran's announcement that the Strait of Hormuz was now open, with WTI down over 10%

- However, the diplomatic state of play remained uncertain into the weekend, and USD pared sharp losses to sit closer to flat on the day

US TSYS: Announced Opening Of Narrow Strait Brings Broad Gains

Treasuries rallied strongly Friday, led by the belly of the curve as it appeared the US and Iran were nearing an end to their conflict.

- The bulk of the gains came before the cash equity open after Iran's foreign minister announced the Strait of Hormuz is now “completely open” for commercial traffic for the remaining period of ceasefire (ending Monday) with President Trump saying talks will be held this weekend (though some reports said Monday).

- The Iranian foreign ministry later sounded more combative, saying "enriched uranium is not going to be transferred anywhere" in contrast to Trump's missives, while also claiming to be the one that determined the opening and closing of the strait.

- Markets largely shrugged off the latter uncertainty over the state of play however, with the Treasury curve leaning in a bull steepening direction on the day.

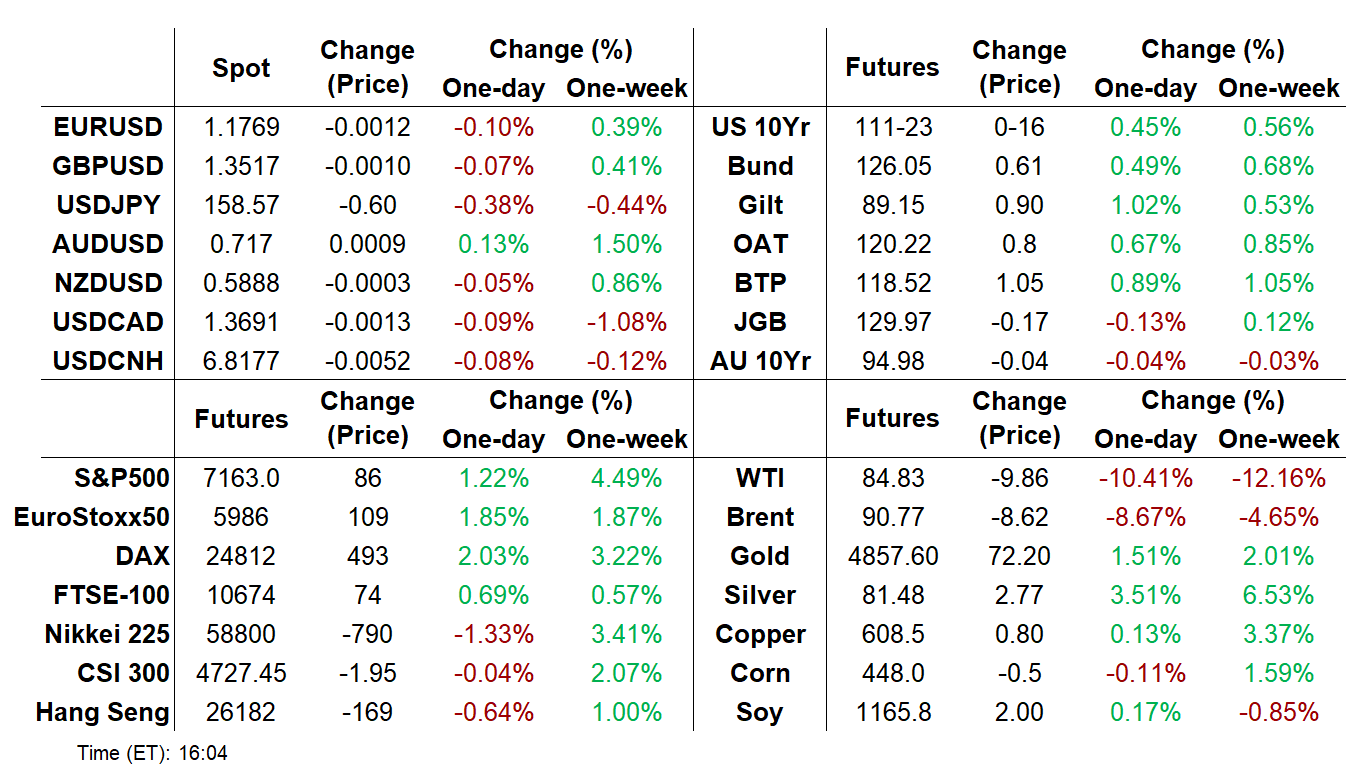

- Latest cash levels: The 2-Yr yield is down 7.6bps at 3.6977%, 5-Yr is down 8.1bps at 3.8379%, 10-Yr is down 7.1bps at 4.2401%, and 30-Yr is down 5.5bps at 4.8775%. Jun 10-Yr futures (TY) up 15.5/32 at 111-22.5 (L: 111-04 / H: 111-27.5)

- Ahead of the FOMC's pre-meeting blackout period that starts this weekend, Gov Waller sounded cautious about re-initiating cuts given the situation in the Middle East, though his comments appeared somewhat stale given the morning's headlines. Overall, rates ended the week on a dovish note, with 16bp of Fed cuts priced for 2026 vs 6bp at the end of last week.

- While weekend developments on the US-Iran front will remain very closely watched, next week's highlights include Tuesday's retail sales release for March, followed shortly Fed Chair confirmation hearing at the Senate Banking Committee for Kevin Warsh.

US OPTIONS: Friday's US rates/bond options flow included:

- SFRK6 96.43/96.56cs, bought for half in 10k

- SFRN6 96.37/96.50/96.62c fly, bought for 1.75 in 5k, done on the pit and screen

- SFRU6 96.50/96.81/97.12c fly vs 96.00/95.75ps, bought the fly for 1.5 in 2.5k

- SFRZ6 96.00p, bought for 8.25 in 5k

- TYM6 112.50 calls, paper paid 0-13 on ~10.4K all day

- TYM6 110.50p x2 vs 110p/109.5p strip x1, bought the package for 22 in 10k (20kx10kx10k)

- USM6 116.00 calls 5K given at 0-27

US TSYS/OVERNIGHT REPO: Secured Rates Stay Well-Behaved In Mid-Month

There were few signs of strain in secured funding markets on the key annual tax deadline of April 15 (which also coincided with $48B in Treasury auction settlements).

- SOFR rose 6bp on the day to reach 3.72%, above the 3.65% IORB, but pulled back to 3.67% on April 16, and we would expect a further pullback Friday April 17.

- It wasn't even the highest of the year, which was Feb 18's 3.73% (which was due in part to mid-quarter refunding auction settlements).

- Standing Repo Facility takeup reached just $10.5B, paltry compared with recent spikes (2026's high remains Feb 17, of $30.5B).

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 3.67%, -0.05%, $3107B

* Broad General Collateral Rate (BGCR): 3.64%, -0.06%, $1276B

* Tri-Party General Collateral Rate (TGCR): 3.64%, -0.06%, $1242B

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 3.64%, no change, volume: $85B

* Daily Overnight Bank Funding Rate: 3.64%, no change, volume: $175B

BONDS: EGBs-GILTS CASH CLOSE: War De-Escalation Triggers Sizeable Rally

EGBs and Gilts soared Friday as the US and Iran appeared on the verge of reaching a lasting end to hostilities, capping a week of strong gains.

- A slew of headlines pointing to further US-Iran de-escalation saw a sizeable bull steepening rally in early afternoon, punctuated by Iran announcing it would allow ships passage through the Strait of Hormuz and Pres Trump corroborating.

- Though each side's details of the conditions for Strait re-opening within the current ceasefire appeared to differ, risk assets were buoyant and energy prices fell sharply (Brent -11%, TTF gas -7%), with Pres Trump eyeing an deal to end the war within a "day or two".

- Gilts slightly underperformed peers at the short end. BoE chief economist Pill's comments Friday sounded like justification for a vote for a hike in April and MNI now considers him to be the most hawkish member on the MPC.

- Both the German and UK curves bull steepened on the day. Unsurprisingly, periphery/semi-core EGB spreads to Bunds tightened, with Italy and Greece outperforming.

- For the week, both the UK and German curves bull steepened: Germany 2Y -19bp, 10Y -10bp; UK 2Y -14bp, 10Y -7bp.

- Moody's will review Belgium's sovereign rating after hours (Current rating Aa3, Outlook Negative). Next week brings April flash PMIs and UK labour market and inflation reports.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 10.9bps at 2.408%, 5-Yr is down 8.6bps at 2.611%, 10-Yr is down 7.2bps at 2.96%, and 30-Yr is down 5bps at 3.541%.

- UK: The 2-Yr yield is down 9.8bps at 4.122%, 5-Yr is down 9.6bps at 4.248%, 10-Yr is down 8.5bps at 4.762%, and 30-Yr is down 7.4bps at 5.493%.

- Italian BTP spread down 5.5bps at 71.8bps / Spanish down 2.1bps at 42.9bps

EUROPE OPTIONS: More Call Structure Buying In Rates, With Added Put Spread Selling

Friday's Europe rates/bond options flow included:

- OEM6 115.75/116.25/116.75/117.25c condor, bought for 13 in 3.25k

- ERQ6 97.62/97.75/97.87/98.00 call condor vs. 97.18/97.06 put spread paper paid 1.0 for the condor on 4K, 14k trades all day

- ERU6 97.00/96.75ps 1x2, sold the 1 at -1.5 and -1.75 in 10k

- ERZ6 98.00/98.25cs, bought for 1 in 10k

- ERZ6 97.875/98.00/98.125 call fly, paper pays 1.75 in 10k

FOREX: Huge Risk Boost Has Moderate Impact on USD, Cross/JPY Shifts Lower

- Risk sentiment received a significant boost on Friday, as latest headlines indicate substantial progress towards peace deals in the Middle East. Energy prices have plummeted prompting an associated surge for both equities and bonds. Initially, the dollar sold off as expected, prompting the DXY to bridge the gap to Feb 27 (pre-war) closing levels, however the index is comfortably off its lows as we approach the weekend close.

- The contained price action and USD reversal has raised some eyebrows, but it could be the relatively limited appetite in currency markets has restricted the dollar from meaningfully breaking out. Cross/JPY has held the bulk of its move lower, which makes sense given the concurrent moves for both energy prices and core yields.

- Having flagged a bull channel earlier in the session, USDJPY’s swift break below 159.00 has accelerated downside momentum, which has been bolstered by a break of the 50-day EMA, which intersected today at 158.13.

- Pre-war levels remain much further down for USDJPY, perhaps a reason for the pair’s relative weakness today. Technical supports are located at 156.46 and 155.85, the March 05 and 02 lows respectively.

- The Australian dollar now remains among the strongest G10 performers on the session amid the risk optimism, setting up a very positive close for AUDUSD close to the 0.72 handle, the highest weekly close since H1 ‘22. With the bull trigger cleared this week, AUDUSD’s next technical target would be 0.7296, the top of a bull channel drawn from the Apr 9 ‘25 low.

- EURUSD rallied to a 1.1849 high before reversing the entirety of the intra-day rally, sliding back towards unchanged levels around 1,1785 as we approach the close. Initial key support to watch lies at 1.1660, the 50-day EMA.

- China LPR Decision and Canada CPI highlight the economic calendar on Monday.

FX OPTIONS: Expiries for Apr20 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600(E1.5bln), $1.1750(E1.7bln), $1.1785-00(E1.3bln)

- USD/CAD: C$1.3600($546mln), $C1.3630-35($548mln), C$1.3800($613mln)

DATA/EVENTS CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 20/04/2026 | 0600/0800 | ** | PPI | |

| 20/04/2026 | 0900/1100 | *** | EZ GDP 4th (Final) | |

| 20/04/2026 | 0900/1100 | ** | EZ Construction Output | |

| 20/04/2026 | 1230/0830 | *** | CPI | |

| 20/04/2026 | 1530/1130 | ** | BOC Business Outlook Survey | |

| 20/04/2026 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 20/04/2026 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 20/04/2026 | 1640/1840 | ECB Lagarde Keynote at Association of German Banks | ||

| 21/04/2026 | 2245/1045 | *** | CPI inflation quarterly | |

| 21/04/2026 | 0600/0700 | *** | Labour Market - AWE & Unemployment | |

| 21/04/2026 | 0600/0700 | *** | Labour Market - Payrolls & Claimants | |

| 21/04/2026 | 0600/0700 | *** | Labour Market - Payrolls & Claimants | |

| 21/04/2026 | 0600/0700 | *** | Labour Market - AWE & Unemployment | |

| 21/04/2026 | 0700/0900 | ECB de Guindos Remarks/Q&A at La Razón Event | ||

| 21/04/2026 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 21/04/2026 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 21/04/2026 | 1215/0815 | *** | ADP Employment Report | |

| 21/04/2026 | 1230/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 21/04/2026 | 1230/0830 | *** | Retail Sales | |

| 21/04/2026 | 1230/0830 | *** | Retail Sales | |

| 21/04/2026 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 21/04/2026 | 1400/1000 | ** | NAR Pending Home Sales | |

| 21/04/2026 | 1400/1000 | * | Business Inventories | |

| 21/04/2026 | 1400/1000 | * | Business Inventories | |

| 21/04/2026 | 1400/1000 | Kevin Warsh | ||

| 21/04/2026 | 1530/1130 | Fed Governor Chris Waller | ||

| 21/04/2026 | - | Central Bank of Republic of Turkiye Meeting | ||

| 22/04/2026 | 2301/0001 | * | Brightmine pay deals for whole economy |