OPTIONS: More Call Structure Buying In Rates, With Added Put Spread Selling

Friday's Europe rates/bond options flow included:

- OEM6 115.75/116.25/116.75/117.25c condor, bought for 13 in 3.25k

- ERQ6 97.62/97.75/97.87/98.00 call condor vs. 97.18/97.06 put spread paper paid 1.0 for the condor on 4K, 14k trades all day

- ERU6 97.00/96.75ps 1x2, sold the 1 at -1.5 and -1.75 in 10k

- ERZ6 98.00/98.25cs, bought for 1 in 10k

- ERZ6 97.875/98.00/98.125 call fly, paper pays 1.75 in 10k

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US 10YR FUTURE TECHS: (M6) Monitoring Resistance

- RES 4: 113-07+ High Mar 3

- RES 3: 113-03 High Mar 4

- RES 2: 112-10/112-24+ 20-day EMA / High Mar 10

- RES 1: 112-07 High Mar 18

- PRICE: 111-25 @ 16:49 GMT Mar 18

- SUP 1: 111-11 Low Mar 13 and the bear trigger

- SUP 2: 111-08+ Low Feb 3

- SUP 3: 111-06+ Low Jan 20 and a key support

- SUP 4: 111-00 Round number support

A bear cycle in Treasuries remains intact and this week’s recovery appears corrective - for now. Initial firm resistance to watch is 112-10, the 20-day EMA. A clear breach of it would signal scope for a stronger bounce. For bears, a resumption of the downtrend would open the next key support at 111-06+, the Jan 20 low. Clearance of this level would highlight an important medium-term bearish development.

FED: Statement: War Re-Raises Uncertainty (1/2)

Going paragraph by paragraph through the previous (January) statement in italics for potential areas of change in the March edition:

- The Statement’s opening paragraph on recent economic developments could be tweaked to reflect a slightly more moderate underlying pace of economic growth, with the language on employment and inflation also in line for edits.

- In particular, we will be interested to see how they handle the strong January payrolls vs the weak February edition (with downward revisions), as well as the expected downward benchmark revisions to 2025. They may simply acknowledge that average job growth has been flat in recent months, but nonetheless the unemployment rate has remained relatively “stable”. This would leave unsettled the FOMC’s debate over the supply vs demand dynamics in the labor market.

- On inflation, the data have been volatile but sticky with some distortions lingering from the BLS shutdown in late 2025, so the FOMC will probably agree that price pressures remain “somewhat elevated”.

- In the 2nd paragraph: “uncertainty” certainly “remains elevated”, and even moreso now given the Middle East conflict.

- In March 2022, the first meeting after the beginning of the Russia-Ukraine war, the Statement added: “The invasion of Ukraine by Russia is causing tremendous human and economic hardship. The implications for the U.S. economy are highly uncertain, but in the near term the invasion and related events are likely to create additional upward pressure on inflation and weigh on economic activity.”

- Similar language could be introduced this month, at least in terms of the implications being “highly uncertain”, though we are doubtful the FOMC will agree on making clear conclusions on the macro impact (ie “upward pressure on inflation” and “weigh on economic activity”), and won’t make a reference to “hardship”.

- That being said, the Statement will probably retain its reference to risks to “both sides” of the dual mandate.

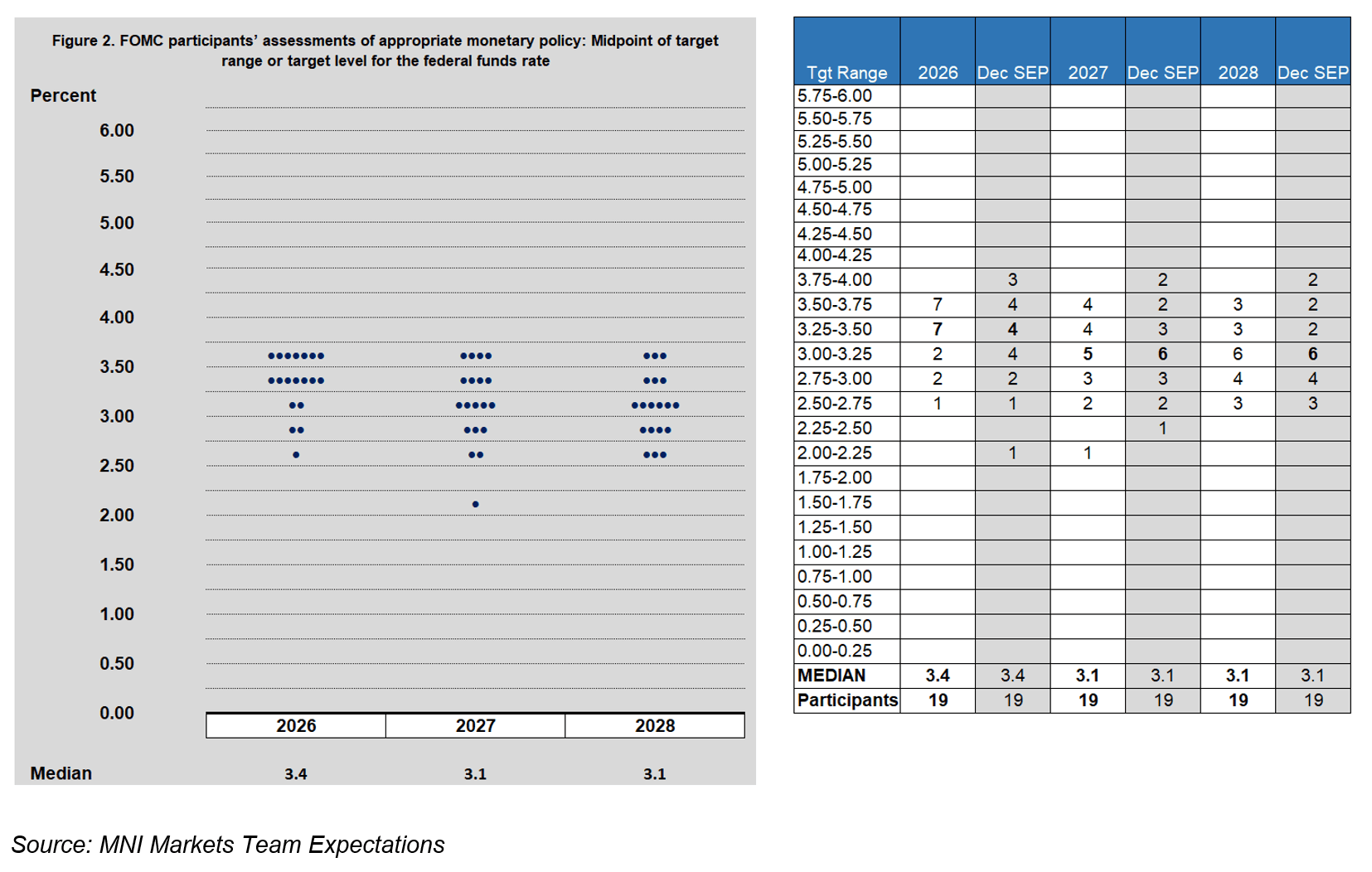

FED: Rate Dot Plot: Standing Pat For Now

We don’t expect any changes to the medians for the 2026-2027-2028 end-year Fed funds rate dots in March’s Dot Plot December’s edition. However a more hawkish distribution of dots looks likely overall and risks are to the upside in terms of projected rates. As usual our Instant Answers look for end-year medians and the current year’s distribution. See image below; more detail is available in our PDF preview.

- Analyst Expectations: Expectations are overwhelmingly that the rate dot medians in the new SEP will remain unchanged (implying the median FOMC member still sees 1 rate cut this year and another in 2027). We saw only one analyst (ING) expect the 2026 dot to be revised to show no implied cuts. Two analysts (BofA and Deutsche) expect the longer-run dot to be nudged up to 3.1% from 3.0%.