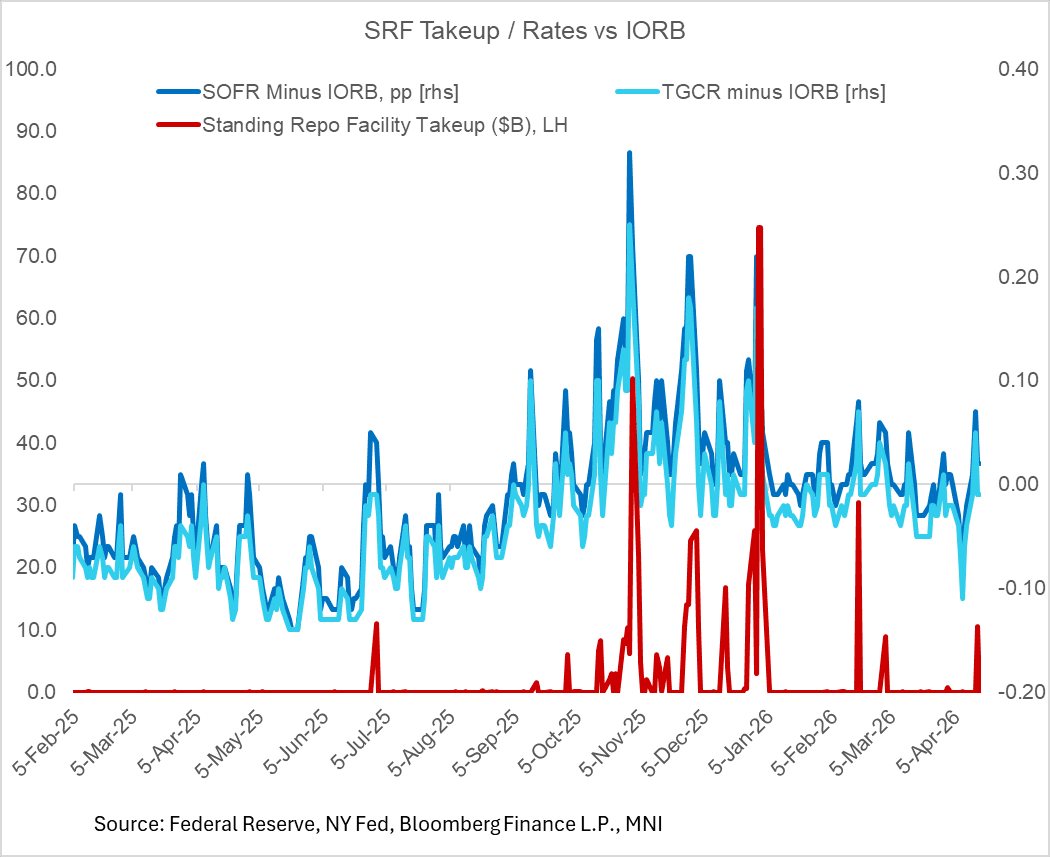

US TSYS/OVERNIGHT REPO: Secured Rates Stay Well-Behaved In Mid-Month

There were few signs of strain in secured funding markets on the key annual tax deadline of April 15 (which also coincided with $48B in Treasury auction settlements).

- SOFR rose 6bp on the day to reach 3.72%, above the 3.65% IORB, but pulled back to 3.67% on April 16, and we would expect a further pullback Friday April 17.

- It wasn't even the highest of the year, which was Feb 18's 3.73% (which was due in part to mid-quarter refunding auction settlements).

- Standing Repo Facility takeup reached just $10.5B, paltry compared with recent spikes (2026's high remains Feb 17, of $30.5B).

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 3.67%, -0.05%, $3107B

* Broad General Collateral Rate (BGCR): 3.64%, -0.06%, $1276B

* Tri-Party General Collateral Rate (TGCR): 3.64%, -0.06%, $1242B

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 3.64%, no change, volume: $85B

* Daily Overnight Bank Funding Rate: 3.64%, no change, volume: $175B

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

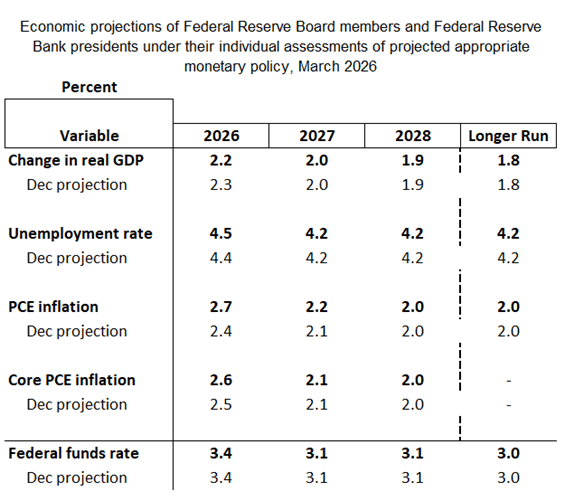

FED: Macro Projections: Tweaked But Not Overhauled Due To Mideast Uncertainty

The median macro forecasts in the March SEP are likely to be tweaked and not overhauled vs the prior edition, given major uncertainty over the Mideast situation.

- 2026 unemployment could be nudged up or remain at 4.4%, with GDP seeing a possible slight downtick but no substantive change.

- The bigger adjustments are likely to be in the inflation column, with both recent inflation stickiness and the latest energy price jump reflected in a higher headline PCE expectation (less so, for core).

- Outer year forecasts, however, are unlikely to see any significant changes.

- Analyst expectations: Opinion is slightly split on how the macro forecasts will shift vs December. Most analysts see 2026 growth revised lower, though some expect an upgrade. There is broad expectation that 2026 PCE inflation (especially headline) will be revised meaningfully higher, to reflect the latest rise in energy prices.

OPTIONS: Larger FX Option Pipeline

- EUR/USD: Mar20 $1.1350-70(E1.9bln), $1.1400(E1.6bln), $1.1450-65(E2.3bln), $1.1500(E1.3bln), $1.1645-50(E1.3bln); Mar24 $1.1400-10(E1.3bln), $1.1500(E1.4bln)

- USD/JPY: Mar24 Y155.00($1.1bln)

- AUD/USD: Mar20 $0.6900(A$1.3bln)

- USD/CNY: Mar20 Cny6.8800($1.2bln); Mar23 Cny6.8500($1.3bln)

US STOCKS: Extending Lows of the Week As Crude Rallies, Inflation Metrics Rising

- Stocks have retreated to the lowest levels of the week (SPX eminis near late Friday levels) after higher than expected PPI inflation metrics (ahead of this afternoon's FOMC policy announcement including the Summary of Economic Projections), coupled with reports that several Iranian gas fields were attacked by Israel, sapped risk sentiment early Wednesday as crude prices surged (WTI crude neared $100/bbl).

- Consumer Staples/Discretionary, Materials and Health Care sector shares underperformed ahead midday

- Despite the rise in geo-political risk, mining stocks weighed on the Materials sector as gold prices plummeted over $140 in the first half, Newmont Corp and Freeport-McMoRan trade -3-3.5% lower.

- The Health Care sector was driven by carry-over weakness in pharmaceutical shares as obesity drug expectations continued to be discounted by analysts, AbbVie and Moderna down between 3.25-3.75%.

- Consumer stocks depressed as core PPI (ex food, energy & trade services) printed 0.53% M/M, up from 0.41% prior (which was upwardly revised from 0.31% prior, though December was revised down 0.11pp to 0.16%) and above the 0.3% consensus. Dollar Tree , Monster Beverage Corp, Philip Morris International and Dollar General Corp all trade -2.6 to 3.8% lower.

- On the flipside, as has been the case since the start of the war between the US/Israel and Iran - oil and gas stocks outperformed.