MNI ASIA MARKETS ANALYSIS: Back to Work, US Gov Set to Reopen

HIGHLIGHTS

- Treasuries Hold lower levels on narrow range Tuesday, brief midday bounce (stocks extend lows) on reports of an Iranian drone being shot down as it approached USS Abraham Lincoln in the Arabian Sea, Reuters.

- The US House of Representatives passed the latest spending bill in the afternoon, ending the Gov shutdown once Pres Trump signs the measure.

- While Friday's employment report will still be delayed until Monday earliest, both US ADP and ISM Services are scheduled on Wednesday’s calendar.

- The EU is weighing a ban on Russian copper and platinum as part of new sanction package and will separately will pitch the US on a critical mineral’s partnership to counter China.

- US gov. plans to issue general licenses for companies to pump oil in Venezuela.

US TSYS

MNI US TSYS: House Passes Funding Bill, Enroute to Pres Trump for Signing

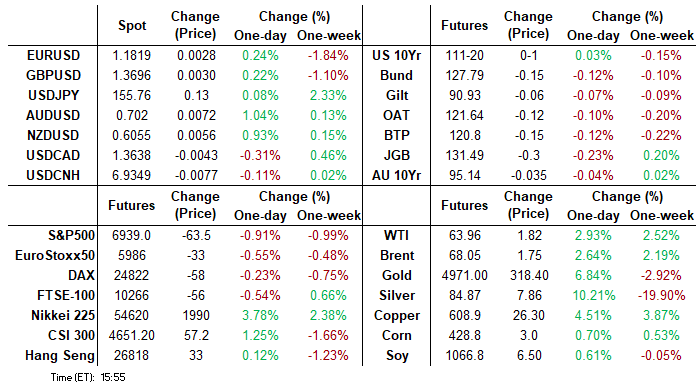

- US Treasuries look mildly mixed after the bell, off lows, curves twisting flatter (2s10s -.382 at 69.993) with the short end underperforming.

- The House approved latest funding package - sending bill to Pres Trump for signing, ending latest government shutdown.

- This morning's JOLTS data delayed due to the Gov shutdown, Friday's employment report will still be delayed until Monday earliest. However, both US ADP and ISM Services are scheduled on Wednesday’s calendar.

- TYH6 currently +1 at 111-20, next important resistance to watch is 112-07+, the 50-day EMA. A clear break of the 50-day average is required to signal scope for a stronger recovery.

- Despite a moderate dip for the dollar, the DXY is broadly consolidating the bounce from last week’s lows, which has helped USDJPY maintain a resilient profile over most of the session. The pair briefly rose to a fresh recovery high of 156.08 before fading in late US trade.

- Look ahead, S&P Global Japan PMI Composite/Services data at 1930ET, RatingDog China Composite PMI Output expected 2045ET.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.69% (+0.01), volume: $3.307T

- Broad General Collateral Rate (BGCR): 3.66% (+0.00), volume: $1.342T

- Tri-Party General Collateral Rate (TCR): 3.66% (+0.00), volume: $1.299T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.64% (+0.00), volume: $93B

- Daily Overnight Bank Funding Rate: 3.64% (+0.01), volume: $170B

FED Reverse Repo Operation

RRP usage retreats to $1.785B with 18 counterparties this afternoon vs. $10.415B Monday. Compares to December 12 low of $0.838B (lowest level since mid-March 2021); this years highest excess liquidity measure: $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury options continued to rotate around downside puts Tuesday, upside call unwinds while underlying futures look mildly mixed after the bell, off lows, curves twisting flatter (2s10s -.382 at 69.993) with the short end underperforming. Projected rate cut pricing cools vs. late Monday levels (*): Mar'26 at -2.2bp (-3bp), Apr'26 at -6.4bp (-6.9bp), Jun'26 at -17.9bp (-18.4bp), Jul'26 at -25.9bp (-26.9bp).

SOFR Options:

+8,000 SFRM6 96.43/96.56/96.62/96.75 call condors, 4.0

+40,785 2QG6 96.43/96.50 put spds, 1.5 vs. 96.56/0.13% (expires in 10 day)

over 4,300 SFRH7 98.5 calls, 2.5 ref 96.75

over 6,200 SFRU6 100 calls ref 96.70

2,000 2QH6 96.75 calls ref 96.575

-2,500 SFRJ6 96.43/96.62 call over risk reversals

1,250 SFRH6 96.37/96.43/96.50 put flys, 0.25

1,500 SFRJ6 96.43/96.50 3x2 put spds ref 96.52

+1,500 SFRH6 96.43/96.50/96.56/96.62 put condors, 0.5 ref 96.36

+2,000 SFRM6 96.43/96.56 2x1 put spds, 1.75

1,250 SFRU6 96.31/96.62 put spds ref 96.695

Treasury Options:

2,000 TYJ6 110/112.5 strangles, ref 111-10.5

-16,000 USJ6 121 calls, 9 ref 114-13 (after paper -14.2k USJ6 120 calls)

2,000 TYH6 110.75/111/111.5 broken put trees

1,500 FVJ6 108/109.25 strangles, 108-19

2,000 TYH6 111.5 puts, 23 (total volume over 16.5k)

over 9,500 TYH6 113 calls, 4 ref 111-19.5 to -16.5

-10,000 USJ6 120 calls, 12 vs. 113-27/0.06%

4,000 TYJ6 111/111.5 call spds ref 111-11

+1,000 TYH6 111.5 straddles, 47

2,500 FVJ6 108 puts, 12-12.5 ref 108-21.25

over 10,500 USJ6 109/111 put spds, 21 ref 113-30

over -8,100 TYH6 111.25 puts, 14 vs. 111-18.5/0.35%

+4,400 TYH6 111 puts, 10 ref 111-17.5

+5,000 TYH6 111.5 puts, 22

MNI BONDS: EGBs-GILTS CASH CLOSE: Supply Weighs

European yields rose modestly Tuesday.

- Bonds started on the back foot following overnight weakness in US Treasuries and a hawkish rate hike by the RBA.

- A softer-than-expected French flash January inflation helped EGBs consolidate briefly, while the ECB's Q4 BLS indicated a relatively muted credit-led growth impulse.

- Supply was a theme all day on both sides of the Atlantic, with multiple European sales (UK/ESM/Italy/German Green) and US corporate supply weighing in the early afternoon.

- Bunds underperformed Gilts which benefited from a solid 4.75% Oct-35 auction amid only limited UK-centric headlines, with most focus remaining on this week's BOE meeting.

- OATs modestly outperformed in the EGB space, following the passage of the 2026 French budget after the cash close Monday.

- Wednesday brings Italy/Eurozone flash January inflation data, with final PMIs. Attention remains on Thursday's ECB and BOE decisions. MNI's ECB meeting preview went out today - PDF here.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.9bps at 2.123%, 5-Yr is up 1.5bps at 2.463%, 10-Yr is up 2.3bps at 2.891%, and 30-Yr is up 3.4bps at 3.55%.

- UK: The 2-Yr yield is up 0.5bps at 3.708%, 5-Yr is up 1.7bps at 3.953%, 10-Yr is up 1.1bps at 4.517%, and 30-Yr is up 1.5bps at 5.288%.

- Italian BTP spread down 0.7bps at 60.7bps / French OAT down 1bps at 57.6bps

MNI EGB OPTIONS: Colossal Call Condors Feature In Rates

Tuesday's Europe rates/bond options flow included:

- RX weekly 127.50/127.00 put spread 8K given at 9 (expire Friday)

- RXH6 127p, bought for 18 up to 18.5 in 6k

- ERZ6 98.25/98.37cs, bought for 1.75 in 17.5k

- ERZ6 98.00/98.06/98.12/98.25 call condor paper paid 0.25 on 39.5K all day, desks point to flow either being linked to ECB easing bias being in play at year-end (with no cut delivered) or a dovish hedge against deterioration in economic outlook/lower-than-expected inflation.

- SFIM6 96.40/96.50/96.80/96.90c condor, sold at 6.75 in 4k

- SFIM6 96.40/96.50/96.65/96.75 call condor paper paid up to 6.25 on 35K total. short vol play, targeting pricing of a 25bp cut when it expires on June 12, just over a week ahead of the BoE's June meeting

- SFIM6 96.55/96.70/96.85 call fly, bought for 2.75 in 5k

- SFIK6 96.60/96.75 call spread vs. 96.53 paper paid 2.0 on 10K

MNI FOREX: AUD Consolidates 1% Rally Post RBA & Amid Metals Recovery

- AUD is the main outperformer on Tuesday, rising 1% against the dollar after the hawkish hike from the RBA overnight. AUDUSD has also been supported by a more stable metals backdrop, with gold prices consolidating a 6% boost on the session. Softer equity sentiment (driven by IT Services lagging) did little to hamper the renewed Aussie optimism, with AUDUSD consolidating back above the 0.7000 mark, continuing to operate between well-defined short-term technical parameters of 0.7094 (cycle highs) and 0.6846 (20-day EMA).

- AUD outperformance has been very notable in the crosses, leading AUDJPY to pierce key resistance of the 2024 highs, placing the cross at its highest level since 1990. Meanwhile, the likes of EURAUD and GBPAUD have extended their most recent selloffs, significant considering the upcoming ECB and BOE decisions on Thursday.

- There has been some regional spillover from the Aussie move, with NZD screening as the second best performer in G10 ahead of Wednesday’s NZ Q4 employment report. Meanwhile, the Swiss Franc is also bouncing back well. This has resulted in EURCHF falling to within 10 pips of yesterday’s cycle lows at 0.9140. In EMFX the likes of MXN and ZAR have rallied around 0.7%, reflective of the supportive price action for precious metals.

- Despite a moderate dip for the dollar, the DXY is broadly consolidating the bounce from last week’s lows, which has helped USDJPY maintain a resilient profile over most of the session. The pair briefly rose to a fresh recovery high of 156.08 before fading in late US trade. Overall, the recent recovery continues to erode USDJPY’s sharp January pullback, with the pair rebounding more than 50% of the impressive 4.6% selloff from the recent cycle highs. Supportive price action has led USDJPY to pierce the 50-day EMA, intersecting at 155.75. A clear break would signal a possible bullish reversal, turning the focus to the next topside level of 157.43, the Jan 19 low.

- Despite the BLS data delays, both US ADP and ISM Services are scheduled on Wednesday’s calendar.

MNI FX OPTIONS: Expiries for Feb04 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600(E1.7bln), $1.1800(E1.2bln), $1.1850(E1.7bln)

- USD/JPY: Y151.50($1.1bln), Y153.25($801mln), Y156.25($663mln)

- AUD/USD: $0.6950(A$2.0bln)

- NZD/USD: $0.5975(N$746mln)

MNI US STOCKS: Late Equities Roundup: IT Services, Discretionary Sectors Lagging

- Still weaker, stocks are trading off session lows late Tuesday, paring losses slightly after the House passed a funding bill that reopens the US Gov once Pres Trump signs it. That said, Friday's employment data produced by the BLS is unlikely to be released on time - most likely Monday or Tuesday at the latest.

- Currently, the DJIA trades down 344.81 points (-0.7%) at 49061.03, S&P E-Mini Futures down 90.75 points (-1.3%) at 6911.5, Nasdaq down 497.4 points (-2.1%) at 23092.44.

- Information Technology stocks came under heavy sell pressure earlier while indexes extended lows after Rtrs headline that an Iranian drone approached US aircraft carrier in the Arabian Sea and was shot down.

- Software and services shares continued to weigh on the tech sector: IT services company Gartner fell -22.41% after missing earnings expectations and announcing divestiture of weaker performing businesses.

- Meanwhile, EPAM Systems fell -14.79%, reportedly after Anthropic (privately held AI company) released new automation tools for the legal industry - spurring concerns that AI tools will disrupt traditional IT service models. Other laggers: Intuit -12.08%, Cognizant Technology Solutions -11.59%, Accenture -10.17% and Synopsys -8.97%.

- Elsewhere, Consumer Discretionary sector shares reversed prior session gains: Expedia Group -15.91%, Booking Holdings -9.39%, Airbnb -8.61%, Norwegian Cruise Line -5.14% and Garmin -3.62%.

MNI EQUITY TECHS: E-MINI S&P: (H6) Trend Structure Remains Bullish

- RES 4: 7141.7 1.236 proj of the Dec 18 - Jan 13 - 21 price swing

- RES 3: 7100.00 Round number resistance

- RES 2: 7080.92 0.764 proj of the Nov 21 - Dec 11 - 18 price swing

- RES 1: 6965.75/7043.00 Intraday high / High Jan 28 and bull trigger

- PRICE: 6921.00 @ 1525 ET Feb 3

- SUP 1: 6864.50 Low Feb 2

- SUP 2: 6814.50 Low Jan 21 and the bear trigger

- SUP 3: 6771.50 Low Dec 18 and a key support

- SUP 4: 6684.50 Low Nov 24

The trend in S&P E-Minis is bullish and Monday’s strong gains reinforce this theme. The move higher also suggests that the recent bear threat merely resulted in a short lived correction. Attention is on key resistance and the bull trigger at 7043.00, the Jan 28 high. A break of this level would confirm a resumption of the primary uptrend and open 7080.92, a Fibonacci projection. Key support and a bear trigger has been defined at 6814.50, the Jan 21 low.

MNI COMMODITIES: Precious Metals Rebound, Crude Rises Amid Geopolitical Tensions

- Precious metals have rebounded on Tuesday as dip buyers have returned, aided by the softer US dollar.

- Spot gold has risen by a further 5.6% to $4,920/oz, below earlier session highs near the $5,000 mark, but still almost 12% above yesterday’s lows.

- Meanwhile, silver is currently up 6.0% at $84.0/oz, 17% above yesterday’s low.

- Looking ahead, BofA expects volatility in gold and silver to remain elevated, although not at the levels seen in recent sessions as the crash has cleaned up the market somewhat in their view.

- From a technical perspective, the sharp sell-off from last week’s high in gold still highlights a potential top in the long-term trend, and from a short-term perspective, marks an unwinding of the recent extreme overbought condition.

- A clear break of the 50-day EMA at $4,564 would signal scope for a deeper retracement and open $4,274.7, the Dec 31 ‘25 low. Initial resistance is $4,999.2, a Fibonacci retracement.

- Similarly, the strong reversal in silver highlights an unwinding of the recent extreme overbought condition. Price has risen back above the 50-day EMA ($79.60), but scope remains for a deeper retracement to $70.071, the Dec 31 ‘25 low. Initial firm resistance is at $91.70, the 20-day EMA.

- Elsewhere, WTI crude is up 1.7% at $63.2/bbl as the market assesses Iran-related geopolitical risks.

- A bull cycle in WTI futures remains intact, although Monday’s impulsive sell-off highlights the beginning of a corrective phase. Attention is on support at the 20-day EMA, at $61.19. Key resistance is at $66.48, the Jan 30 high.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 04/02/2026 | 0815/0915 | ** | S&P Global Services PMI (f) | |

| 04/02/2026 | 0815/0915 | ** | S&P Global Composite PMI (final) | |

| 04/02/2026 | 0830/0930 | Riksbank Minutes | ||

| 04/02/2026 | 0845/0945 | ** | S&P Global Services PMI (f) | |

| 04/02/2026 | 0845/0945 | ** | S&P Global Composite PMI (final) | |

| 04/02/2026 | 0850/0950 | ** | S&P Global Services PMI (f) | |

| 04/02/2026 | 0850/0950 | ** | S&P Global Composite PMI (final) | |

| 04/02/2026 | 0855/0955 | ** | S&P Global Services PMI (f) | |

| 04/02/2026 | 0855/0955 | ** | S&P Global Composite PMI (final) | |

| 04/02/2026 | 0900/1000 | ** | S&P Global Services PMI (f) | |

| 04/02/2026 | 0900/1000 | ** | S&P Global Composite PMI (final) | |

| 04/02/2026 | 0930/0930 | ** | S&P Global Services PMI (Final) | |

| 04/02/2026 | 0930/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 04/02/2026 | 1000/1100 | ** | EZ PPI | |

| 04/02/2026 | 1000/1100 | *** | EZ HICP Flash | |

| 04/02/2026 | 1000/1100 | *** | EZ HICP Flash | |

| 04/02/2026 | 1000/1100 | *** | EZ HICP Flash | |

| 04/02/2026 | 1000/1100 | *** | EZ HICP Flash (2dp) | |

| 04/02/2026 | 1000/1100 | *** | Italy Flash Inflation | |

| 04/02/2026 | 1000/1100 | *** | HICP (p) | |

| 04/02/2026 | 1000/1100 | *** | Italy Flash Inflation | |

| 04/02/2026 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 04/02/2026 | 1330/0830 | *** | Treasury Quarterly Refunding | |

| 04/02/2026 | 1445/0945 | *** | S&P Global Services Index (final) | |

| 04/02/2026 | 1445/0945 | *** | S&P Global US Final Composite PMI | |

| 04/02/2026 | 1500/1000 | *** | ISM Non-Manufacturing Index | |

| 04/02/2026 | 1500/1000 | Treasury Secretary Scott Bessent | ||

| 04/02/2026 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 04/02/2026 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 04/02/2026 | 1700/1200 | Richmond Fed's Tom Barkin | ||

| 04/02/2026 | 2330/1830 | Fed Governor Lisa Cook | ||

| 05/02/2026 | 0030/1130 | ** | Trade Balance |