EUROPEAN INFLATION: Mixed Developments In German March Inflation Progress [2/2]

A mixed bag for German inflation in March, including differing Y/Y trends in services-heavy CPI subcategories.

- The mixed-weight transport category (i.e. across goods & services) was key in March at 0.88% Y/Y (state-level data had implied 0.9-1.0%) after 2.4% in Feb. It confirmed that energy (-2.77%, we saw between -2.5% to -3.0% vs -1.6% in Feb) and travel services (airfares -8.04% Y/Y vs 9.26% prior) acted in tandem here.

- Within the services-heavy CPI subcategories, there were some considerable differences in the Y/Y pace since December, as projected by MNI after state-level data. Moderation was seen in education (4.67% Y/Y, MNI saw 4.7% vs 5.0% Feb), restaurants and hotels (3.84%, we saw 3.9% vs 4.2%) and recreation & culture (1.05%, we saw 1.0% vs 1.1%). To the upside however, communications at -1.10% Y/Y (we saw -1.1% vs -1.2%) and healthcare at 2.98% (we saw 3.0% vs 2.8%).

- A material acceleration in food inflation was also confirmed, at 3.4% Y/Y (MNI saw 3.4 to 3.5%) after 2.8% in Feb.

- Categories associated with the core goods sector appear also firmer than before - clothing and footwear came in at 1.0% (we saw 1.2-1.3% after 0.5% prior) and furnishings and household Equipment at -0.25 (we saw -0.24% after -0.7%).

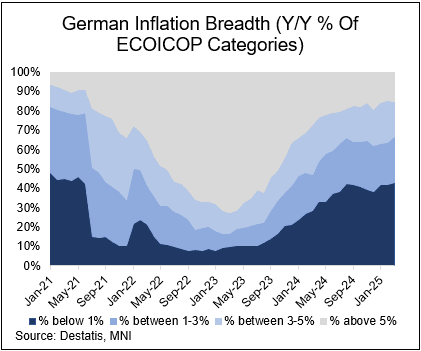

Separately, MNI’s inflation breadth tracker (see chart below) shows disinflation slowly progressing in the low-inflation categories in March, with the percentage of ECOICOP items printing below 1% Y/Y up to 43% from 42% prior. However, disinflation progress stalled in the high-inflation categories, with the percentage above 5% Y/Y holding around 15%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITY TECHS: E-MINI S&P: (H5) Has Entered Oversold Territory

- RES 4: 6178.75 High Dec 6 ‘24 and key resistance

- RES 3: 6166.50 High Jan 19

- RES 2: 5963.30 50-day EMA

- RES 1: 5757.75/5880.10 High Mar 10 / 20-day EMA

- PRICE: 5582.75 @ 07:24 GMT Mar 12

- SUP 1: 5534.00 Low Mar 11

- SUP 2: 5523.00 Low Sep 11 2024

- SUP 3: 5499.25 Low Sep 9 2024

- SUP 4: 5444.55 76.4% retracement of the Aug 5 - Dec 6 ‘24 bull leg

A bear threat in S&P E-Minis remains present and fresh cycle lows this week reinforce current conditions. MA studies are in a bear-mode set-up and this highlights a dominant downtrend and bearish market sentiment. Sights are set on the next important support at 5499.25, the Sep 9 2024 low. Note that the short-term trend condition is oversold, a corrective bounce would allow this set-up to unwind. Firm resistance to watch is 5963.30, the 50-day EMA.

UK DMO UPDATE: DMO releases first three week of April calendar

The DMO has announced its auction calendar for the first 3 weeks of April.

- On offer are the 5-year 4.375% Mar-30 gilt, 10-year 4.50% Mar-35 gilt, 30-year 4.375% Jul-54 gilt (all as we expected).

- Also on offer will be the 15-year 4.375% Jan-40 gilt and the 10-year linker (1.125% Sep-35 I/L gilt).

- The final calendar will be released on Friday at 7:30GMT.

SWEDEN: Vacancy To Unemployment Claims Ratio Posts Fresh Cycle Low

The Swedish unemployment claims rate (from the Public Employment Service) was steady at 7.0% for the fourth consecutive month in February. However, a renewed fall in vacancies (90.3k vs 98.2k prior; -21% Y/Y) signals labour market conditions are still loosening somewhat. The vacancy-to-unemployment-claims ratio fell to 0.25 (vs 0.27 prior), the lowest since May 2021.

- While the Riksbank are firmly expected to remain on hold next Thursday on the back of increased inflationary pressures, Governor Thedeen noted at yesterday’s Parliamentary Hearing that activity signals at the start of 2025 have been mixed. The labour market remains a weak point, keeping focus on Friday’s LFS data. The LFS unemployment rate is expected to pull back from January’s spike to 9.7% (cons 8.9%).

- 4,700 workers were served redundancy notices in February. That’s below January’s 5,100, but the 3mma ticked up to 5,169 (vs 5,111).

- Note, the unemployment rate quoted above includes people in job support programmes. The figure quoted on the Bloomberg calendar only includes unemployment claimants (i.e. excluding those in support programmes).