PERU: Mining Investment Continuing To Accelerate, BCRP Seen On Hold Next Week

Oct-03 13:14

* Mining investment rose by 10.7% y/y to $2.823bn in the first seven months of the year, according...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

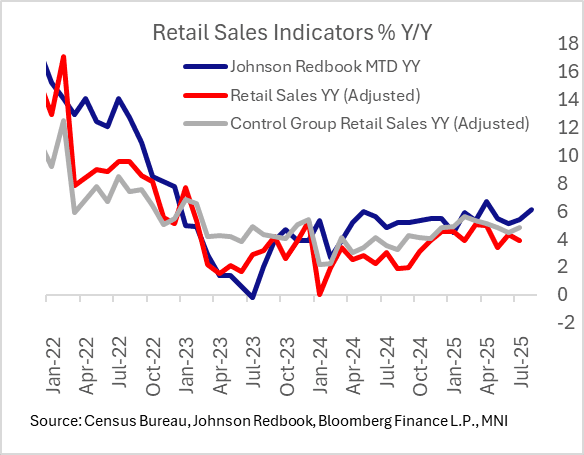

US DATA: Redbook Retail Sales Closes August Strong, "De Minimis" Noted As Factor

Sep-03 13:14

Johnson Redbook retail sales rang up a 6.1% Y/Y increase in August, following consecutive weekly 6.5% Y/Y gains to end the month. This brought sales close to retailers' targeted 6.2% gains for the month.

- The report notes a preliminary target for September of 6.3% Y/Y sales growth.

- The anecdotal portion of the report highlights potential shifts in shopping habits due to the recent elimination of de minimis exemptions on small value imports: "Most companies in our sample reported strength in back-to-school apparel categories, particularly for children's and juniors' clothing and shoes. Shoppers are prioritizing value and are increasingly shopping at warehouse clubs and discount stores. This trend has also been somewhat influenced by the loss of duty-free status for cheap imports priced at $800 or less in the United States. For most retailers, the August sales period concluded on Saturday, the 30th, which means that the bulk of Labor Day shopping will not be reflected in this week's report."

- August Census Bureau advance retail sales are only out on Sep 16th; there is no consensus yet but the Redbook report continues to point to fairly robust dynamics (on a nominal basis, at least). Y/Y Control Group printed 4.8% Y/Y in July vs 5.4% for Johnson Redbook.

GILTS: Recovery Rally Stalls

Sep-03 13:10

The recovery in gilt futures has stalled around 90.00, meaning that bulls have been unable to threaten a close of yesterday’s opening gap lower (~90.27).

- Bears remain in technical control after the contract registered a fresh cycle low and pierced initial Fibonacci support this morning.

- Bulls need to clear session highs from late August (90.84) to start turning the technical tide in their favour.

- Yields now 1-3bp lower, with the early bear steepening impetus flipping to bull flattening during the recovery.

- 5s30s still above 150bp, just, after registering a fresh closing cycle high on Tuesday, followed by a fresh multi-year intraday high (154.5bp) this morning.

- Risks remain tilted to the upside when it comes to long end yields, with curve steepening risks also remaining evident, given the ongoing fiscal headwinds that the UK faces.

- Conviction surrounding those risks has probably eased a little given current valuations and locations within multi-year/decade ranges, in addition to the degree of fiscal worry evident at present (a lot of bad news is priced in, but further fiscal deterioration/worry could drive an extension).

- A reminder that both the BoE and the DMO took a more activist approach to quelling spikes higher in long end yields earlier this year, with the BoE’s September decision (which will include a QT pace announcement) presenting the next scheduled calendar event on that front.

- The BoE Treasury Select Committee hearing will begin shortly (14:15 London).

SCHATZ: Large Schatz Roll goes through

Sep-03 13:08

Large Schatz volume goes though in the past 5 minutes, multiple clips in the Roll:

- DUU5/Z5 is bought at -8.5 in 139k total.