PERU: MNI BCRP Preview – Oct 2025: Rate Hold Seen As Policy Near Neutral

Executive Summary

- The BCRP is widely expected to leave its policy rate unchanged at 4.25% this week, although latest softer-than-expected CPI inflation data still keep the door open to a possible further cut in the coming meetings.

- After delivering a 25bp reduction last month, the central bank said that the policy rate was now very close to neutral, and Governor Velarde has subsequently said that there is no need to be aggressive with rate cuts.

- With growth still around potential there is little urgency to move this week, but some analysts still see scope for one final cut later in the quarter.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LOOK AHEAD: Tuesday Data Calendar: BLS Survey Revision, 3Y Note Sale

- US Data/Speaker Calendar (prior, estimate)

- 09/09 0600 NFIB Small Business Optimism (100.3, 100.5)

- 09/09 1000 BLS Prelim Benchmark Revision to Establishment Survey Data

- 09/09 1130 US Tsy $85B 6W bill auction

- 09/09 1300 US Tsy $58B 3Y Note auction (91282CNY3)

ITALY AUCTION PREVIEW: On offer this week

MEF has announced it will be looking to sell the following at its auction this Thursday, September 11:

- E2.75-3.25bln of the 2.35% Jan-29 BTP (ISIN: IT0005660052)

- E1.25-1.50bln of the 4.00% Nov-30 BTP (ISIN: IT0005561888)

A reminder that "the auctions of 7-year BTPs and BTPs with a maturity longer than 10 years, scheduled for the same day will not be held due to the recent issuance through a syndicate."

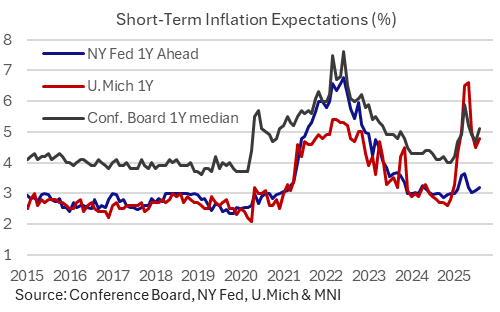

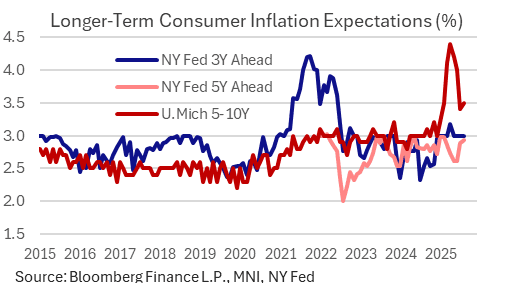

US DATA: NY Fed Consumer Survey: Inflation Expectations Looking Stubborn (1/2)

The New York Fed's Survey of Consumer Expectations leaned in a stagflationary direction in August, showing both an uptick in short-term inflation expectations and increasing pessimism on the labor market front. Overall the deterioration in the labor market outlook is likely to be the main takeaway from the FOMC going into its meeting next week, stubborn inflation expectations are unlikely to be ignored, illustrative of the Fed's current policy dilemma.

- Starting with the closely-watched inflation expectations, the survey saw a rise in the 1Y median to a 3-month high 3.20% from 3.09% prior. The 3Y median was steady at 3.00% for a 4th consecutive month, but the 5Y median ticked up to a 6-month high 2.93% (2.88% prior).

- The 1Y reading mirrors August increases in other consumer expectations surveys of 1Y inflation expectations, including UMichigan (4.80% from 4.50%) and Conference Board (6.20% from 5.70%). All are below tariff-related peaks earlier this year but appear to have bottomed out.

- We also note a subtle uptick in the UMichigan 5-10Y metric, to 3.5% from 3.4%. In both surveys, this metric appears to have stalled out above pre-2025 tariff levels.

- That said, we think most on the FOMC consider the NY Fed survey to be the most "robust" among these measures in terms of methodology. While it's shown much less dramatic swings than its counterparts, it is showing short-term/3Y pressures as being a little more elevated than in previous periods when the Fed was contemplating easing.

- Somewhat counter-intuitively, the survey's measure of median one-year ahead point predictions for various commodity price changes (eg gas, food, healthcare, education, rent, gold) were all flat to somewhat lower. The big standout on that front was for rent, for which inflation is seen running at 6.0%, down sharply since 9.1% in June and lowest since January.

- Median uncertainty over future inflation ticked a little higher though remained in recent ranges (which since the pandemic have been elevated vs the 2013-19 period,