EM ASIA CREDIT: Mineral Resources: Solid Q1 operations

(MINAU, Ba3-neg/NR/BB-neg)

"*Mineral Resources: On Track to Meet FY26 Volume, Cost Guidance" - BBG

"*Mineral Resources Says Net Debt-to-Ebitda Continues to Reduce" - BBG

1Q operations on track, leverage falling, positive bias for credit.

MinRes released its September-quarter (1Q26) activity report, confirming volume and cost guidance across all divisions. Mining Services production reached 81Mt for the quarter, up 19% YoY, driven by the ramp-up of Onslow Iron toward nameplate capacity (35Mt per annum). FY26 guidance remains for 305–325Mt.

From a credit standpoint, liquidity stood at AUD1.1bn and net debt at AUD5.4bn. The company indicated leverage is trending lower, supported by expected cash flow growth from Onslow Iron, though no detailed metrics were provided (financial results due Jan '26). As of FY25-end, net debt to underlying EBITDA was 5.9x.

Earlier this week, MinRes announced a AUD200m inflow from Morgan Stanley Infrastructure Partners following achievement of project milestones at Onslow Iron, which will support deleveraging.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: AUD Crosses - AUD Looks To Build Upward Momentum Again

US equities stalled just ahead of their all-time highs as the market started to ask why a shutdown was good for equities ? This morning US futures have opened slightly lower on our open, E-minis(S&P) -0.05%, NQZ5 -0.10%. The AUD is looking to rebuild momentum higher in the crosses after a period of consolidation.

- EUR/AUD - Overnight range 1.7824 - 1.7891, Asia is currently trading around 1.7830. The pair topped out after multiple failures to extend above 1.7900. Price is still in the middle of its recent 1.7600 -1.8100 range. Expect sellers to fade bounces while price remains below 1.8000, a move below 1.7750 would signal a test of the bottom of the range.

- GBP/AUD - Overnight range 2.0399 - 2.0488, Asia is trading around 2.0420. The pair has seen supply return on every look above 2.0500, I suspect rallies back to 2.0550/0650 will continue to be met with supply. The price action of the pair is looking potentially exhaustive but a sustained break sub 2.0300 is needed to open up a deeper pullback towards 1.9800/2.0000.

- AUD/JPY - Overnight range 97.53 - 97.82, Asia is trading around 97.75. The pair found solid demand back towards 97.00 and bounced last week with the help of the AU CPI print. While above 97.00 the focus will remain on September’s highs toward 98.50.

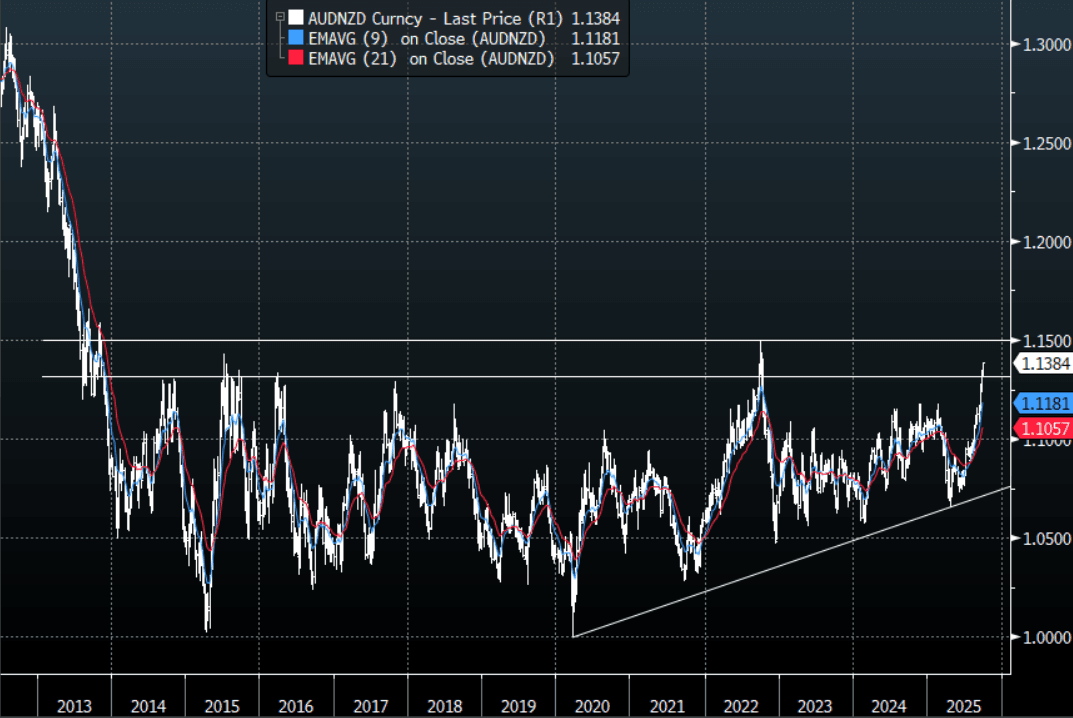

- AUD/NZD - Overnight range 1.1338 - 1.1386, the cross is dealing in Asia around 1.1385. The Cross has broken above the multiple highs around the 1.1200 area and has accelerated up towards 1.1400. I would think this 1.1400/1.1500 would initially be met with sellers and expect some work to be done up here before another extension higher.

Fig 1: AUD/NZD spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

LNG: Gas Within Recent Ranges As Supplies Solid

European natural gas fell 2.1% to EUR 32.00 on Monday but is still up 1.2% in September and remains in the range that it has traded in this month (31.36/33.44) given uncertainties around the Russian outlook. It reached a high of EUR 32.43 before falling to EUR 31.95. Storage refilling ahead of the heating season has continued with it reaching 82.5% full. This and softer demand from China have kept gas prices subdued.

- Europe is looking to bring forward its plans to end Russian gas consumption by a year to end 2026. While pipeline flows are minimal, imports of Russian LNG have increased. With the war in Ukraine continuing, further sanctions seem likely with President Zelenskyy stating they could be announced this week.

- There have been minimal supply disruptions with Gulf gas rigs so far avoiding storms and Norwegian output returning as expected after scheduled maintenance.

- US gas rose 1.8% to $3.275 on Monday to be down 1.7% in September. It reached a monthly low of $3.055 on 23 September and has trended higher since then. There are forecasts for warmer weather in early October and thus expectations of increased cooling demand. NatGasWeather also said that there could be increased demand for LNG output.

- US lower-48 gas production was up 6.5% y/y on Monday while demand rose 4.6% y/y. Estimated flows to LNG export facilities rose 8.8% w/w, according to BNEF gas data.

- Kpler data is indicating that China’s LNG imports fell more than 20% y/y in September. However, it continues to take shipments from Russia’s sanctioned Arctic LNG 2 facility.

US STOCKS: S&P - Stalls Back Towards All-Time Highs

The S&P(ESZ5) overnight range was 6696.25 - 6736.00, SPX closed +0.26%, Asia is currently trading around 6708. The stock market stalled just ahead of its all-time highs as the market started to ask why a shutdown was good for equities ? This morning US futures have opened slightly lower on our open, E-minis(S&P) -0.10%, NQZ5 -0.10%. The stock market continues to look way overdone and is in what is supposed to be a difficult seasonal period, the last 2 weeks of September in particular. In saying that, if that was the extent of the pullback last week it was very shallow ! The market is clearly still in an uptrend and dips continue to be supported for now.

- Daily Chartbook on X: "Traditional measures show U.S. equity valuations are above average. Where they settle will depend on how the economic transformation underway plays out. We believe AI-led productivity gains could boost earnings growth." - @BlackRock

- Bloomberg - “S&P 500 Has a Proven Record of Resisting the Drag of Shutdowns. In past instances of either an actual or threatened shutdown, the S&P 500 did get hit momentarily. Yet any impact tends to be short-lived and has hardly stopped the index from eventually reaching all-time highs.”

- Unusual whales on X: “Global equities are likely to extend a rally into the year end given a resilient US economy, supportive valuations and a dovish pivot from the Fed, per Goldman Sachs.”

- Lance Roberts on X: “Returns in Q4 tend to be the strongest of the year. With professionals underweight, the return of buybacks, and strong momentum, a push higher into year-end will not be surprising.”

- Daily Chartbook on X: "Retail investors — often dismissed as the 'dumb money,' late to act and quick to overreact — have repeatedly been ahead of the curve this cycle ... Their current retreat from the market’s frothiest corners may again be a signal worth heeding." - @isabelletanlee @VildanaHajric. See Graph Below

Fig 1: Retail Taking Profit

Source: MNI - Market News/@dailychartbook/Bloomberg Finance L.P