ASIA STOCKS: Middle East Tensions Weigh Heavy on Stocks

Most major bourses were down today as stories suggest that President Trump has approved US attacks on Iran, a move seen to further escalate the middle east conflict. With limited key data out in the region and financial markets waiting for the Federal Reserve decision on rates, the path of least resistance was lower.

- The Hang Seng led China's bourses lower for a third straight day falling by -2.00%. The CSI 300 followed falling by -0.78%, Shanghai Comp was down -0.86% and Shenzhen fell -1.27%.

- The KOSPI has been a standout of late in delivering gains but this could not hold up today as slipped only marginally by -0.08%.

- The FTSE Malay KLCI fell -0.58% and is down over -1.5% in its last five trading days.

- The Jakarta Composite fell heavily by -1.3% following the Central Bank's decision yesterday.

- The FTSE Straits Times fell by -0.28% and the PSEi in the Philippines eked out minor gains of +0.18% ahead of the decision by the BSP on rates.

- The NIFTY 50 in India is barely in the positive in morning trade, up just +0.08%

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: Asia FX Wrap - Risk Sees Some Reversion, The USD Holds Steady

The BBDXY has had a range of 1224.40 - 1226.87 in the Asia-Pac session, it is currently trading around 1225. China Prime Rates Lowered As Expected: The 1 and 5 year Loan Prime Rates were reduced in line with expectations. The move lower by 10bps for each sees the 1-year LPR to 3.00% and the 5-year LPR to 3.50%, the lowest they have been since inception. CATL’s huge listing on the Hong Kong exchange produced an early jump for the shares, which is lifting the Hang Seng Index as the trading debut will also encourage more IPOs to list in the city on attractive valuations.(BBG)

- EUR/USD - Asian range 1.1218 - 1.1251, Asia is currently trading 1.1245.The market is still expected to use dips as a buying opportunity with dips back towards 1.09/1.10 well supported.

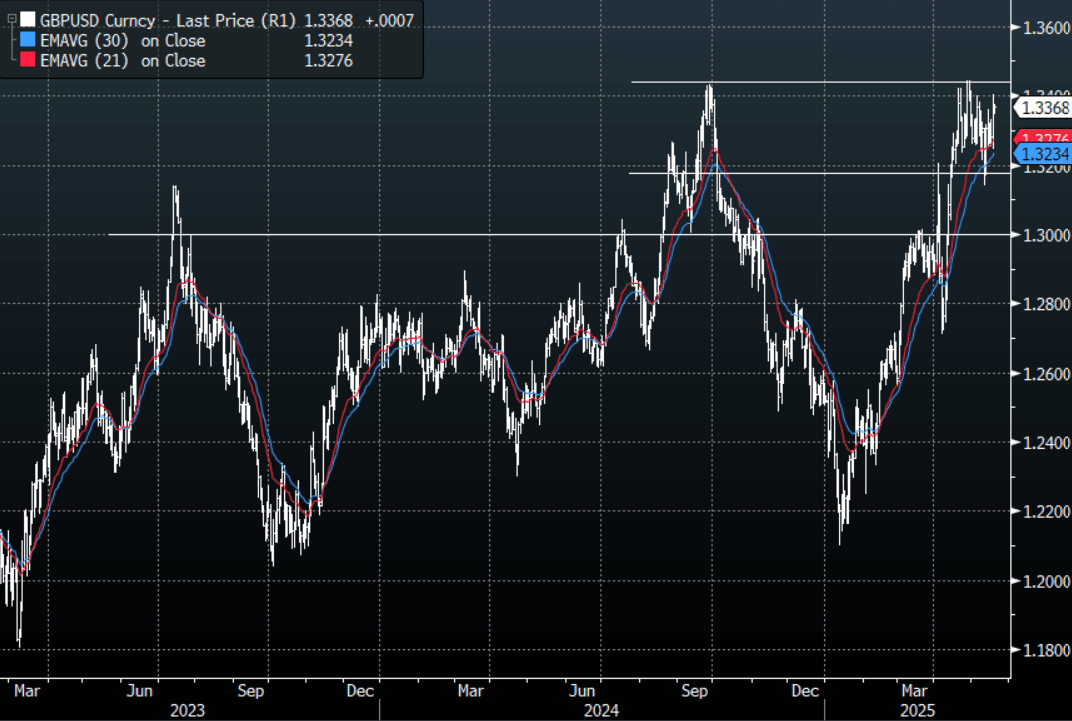

- GBP/USD - Asian range 1.3345 - 1.3376, Asia is currently dealing around 1.3370. Decent demand for GBP sub 1.3200 has seen it bounce back and it looks likely to test the upper bounds of its range above 1.3400. Like the EUR the market prefers to buy on dips.

- USD/CNH - Asian range 7.2128 - 7.2263, the USD/CNY fix printed 7.1931. Asia is currently dealing around 7.2230. Sellers should be found on a bounce back towards 7.24/25 again.

- Cross asset : SPX -0.3%, Gold $3215, US 10-Year 4.45%, BBDXY 1225, Crude oil $62.72

Data/Events : Ger PPI, EZ Current A/C, EZ Construction Output, EZ Consumer Confidence, Philly Fed nonmanufacturing survey

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg

AUD: Asia Wrap - AUD Lower As RBA Lowers Inflation & Growth Forecasts

The AUD/USD has had a range of 0.6423 - 0.6459 in the Asia- Pac session, it is trading around 0.6425. The RBA lowered rates by 25 basis points as expected to 3.85% and lowered inflation and growth forecasts.

- The AUD has come off as the RBA lowers inflation and growth forecasts: “ The Board judged that the risks to inflation have become more balanced. Inflation is in the target band and upside risks appear to have diminished as international developments are expected to weigh on the economy. With inflation expected to remain around target, the board therefore judged that an easing in monetary policy at this meeting was appropriate.”

- "AUSTRALIA NATIONAL PARTY LEADER LITTLEPROUD: ENDING COALITION WITH LIBERAL PARTY, NATIONAL PARTY WILL SIT ALONE ON A PRINCIPLE BASIS - [RTRS]"

- The AUD/USD has found demand around 0.6400 again overnight, expect buyers to be around on dips while the support in the AUD holds, a close back below 0.6300/50 would start to challenge the newly formed uptrend.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6350(AUD367m May 20), Upcoming Strikes : 0.6375(AUD483.6m May 23), 0.6550(AUD480.3m May 23)

- AUD/JPY - Today's range 93.02 - 93.84, it is trading currently around 93.05. Decent demand seen towards the 93.00 area where it holds again overnight. A sustained close back below 91.50/92.00 is needed to turn the focus back towards the lows again. If stocks continue to press higher AUD/JPY could drift back towards the 96.00 area.

RBA: RBA Cuts, Trims Inflation & Growth Forecasts, AUD & OIS Softer

The RBA cut rates as expected by 25bps and left a dovish first impression in terms of the statement, by trimming its inflation (trimmed mean) and growth forecasts slightly. In the bond space, futures are ym +4 xm+3. OIS is flat to -5, with late 2025 leading. AUD/USD is back to 0.6430/35 (post decision lows were at 0.6426). We were near 0.6440/45 prior to the outcome. More details to follow.