US STOCKS: Midday Equities Roundup: TSMC Beat Kick Starts Chip Maker Rally

Jan-15 16:42

- Stocks are firmer Thursday, Technology sector shares leading the move off yesterday's approximate 1-week lows after Taiwan Semiconductor Manufacturing Company (TSMC) reported better than expected 35% Q4 profits while forecasting accelerated revenue growth in the near term.

- Currently, the DJIA trades up 414.34 points (0.84%) at 49,548.12 (vs. 49,633.35 record high on Jan 12), S&P E-Mini Future up 44.75 points (0.64%) at 7009.5 (vs. 7,036.25 record high on Jan 13), Nasdaq up 212.8 points (0.9%) at 23,676.65 (vs. 23,813.3 record high on Jan 13).

- As noted, the Tech sector was buoyed by semiconductor makers following TSMC's better than expected earnings, leading gainers included: KLA Corp +9.43%, Applied Materials +8.00%, Advanced Micro Devices +6.07%, Lam Research +6.04%, Qnity Electronics +5.40%, Monolithic Power Systems +5.14% and Micron Technology +3.17%.

- Industrials and Utilities sector shares followed: Comfort Systems USA +5.10%, EMCOR Group +4.12%, United Airlines Holdings +3.74%, Quanta Services +3.09% and Builders FirstSource +2.76%; ehilr Vistra +7.69%, NRG Energy +5.05%, Constellation Energy +3.99% and AES Corp +2.04% buoyed Utilities.

- Conversely, Health Care and Energy sector shares underperformed in the first half, pharmaceutical makers weighed on the former: Eli Lilly -4.87%, Viatris Inc -2.70%, AbbVie Inc -2.33%, Bristol-Myers Squibb -1.98% and Moderna Inc -1.92%.

- Oil and gas stocks weighed on the Energy sector as crude prices tumbled (WTI -2.92 at 59.10) with geopolitical tensions between the US and Iran cooling slightly: APA Corp -3.41%, ONEOK -1.92%, Diamondback Energy -1.45%, Occidental Petroleum -1.37%, Devon Energy -1.31% and Marathon Petroleum -1.19%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

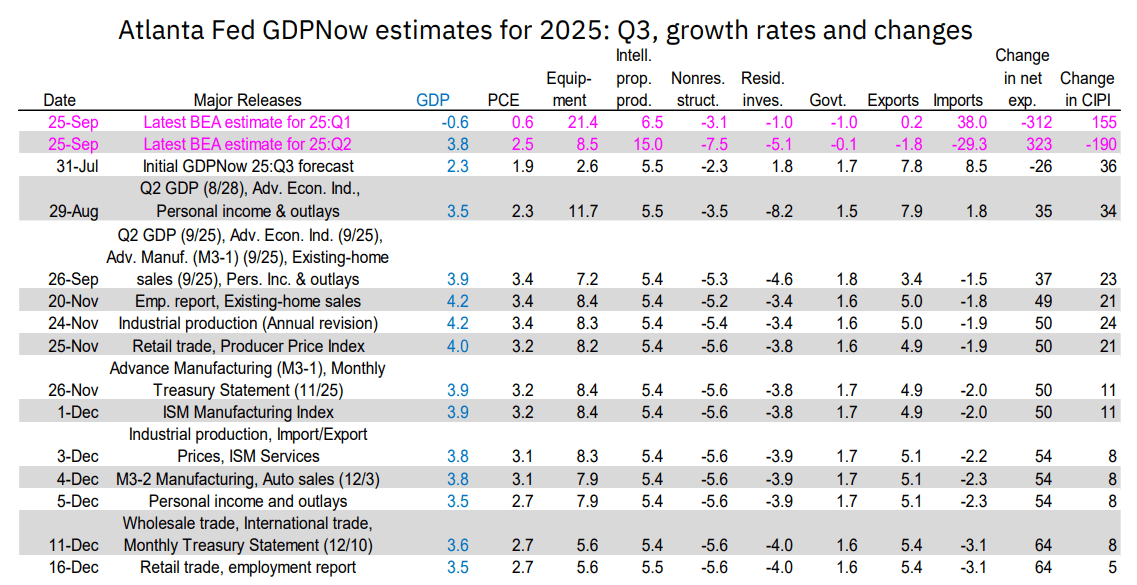

US DATA: GDPNow For Q3 Slips Slightly On Inventories, Consumption

Dec-16 16:30

The Atlanta Fed's GDPNow estimate for Q3 edged a little lower after the release of the October retail sales, September business inventories, and October/November employment reports Tuesday. The current reading of 3.47% Q/Q SAAR represents a 0.1pp downgrade from last Thursday's update and is the lowest since the September 24th nowcast.

- Of course the latest data are mostly reflective of Q4 and not Q3 dynamics, but the delayed release of business inventories for the final month of Q3 was enough to nudge the contribution of inventories to GDP by 0.05pp. The remainder of the downgrade was accounted for by weaker PCE (2.69% after 2.75%), which is the lowest estimate for the quarter's consumption since August.

- At this point, incoming delayed data are largely just refining the estimate. We only get the advance report for Q3 next week at which point GDPNow will start tracking Q4.

US TSY FUTURES: BLOCK: Mar'26 5Y Buy

Dec-16 16:21

- +5,000 FVH6 109-09, buy through 109-08.75 post time offer at 1111:55ET, DV01 $222,000.

- The 5Y contract trades 109-09.5 last (+3.75).

SOFR: BLOCK: Red Sep'27 1Y Bundle

Dec-16 16:14

- 3,000 SFRU7 1Y bundle (SFRU7-SFRM8) +0.030 at 1102:43ET, likely swap-tied selling with spds running wider at the moment.