EU REAL ESTATE: Merlin Properties: New 8yr Guidance ms+110a (+/-5)

Aug-28 11:34

• Guidance Exp. 500m 8yr Green ms+110a (+/- 5 wpir)

• Books >1.5bn - leads

• IPT: €500m expected 8yr Green ms+135a

• We saw FV ms+95 based on the current MRLSM curve and using Gecina as the main comp for a well-run office company.

• Worth highlighting that Merlin is transitioning into being primarily a Data Centre provider and EQIX/DLR do trade wider albeit with slightly lower credit ratings (half notch).

• Looking at the Guidance it would appear that investors are paying attention to the Capex needs for the data roll-out.

(MRLSM; Baa1/BBB+/NR)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OUTLOOK: Price Signal Summary - Candlestick Reversal Signal In Bunds

Jul-29 11:32

- In the FI space, Bund futures have recovered from last Friday’s 128.84 low. Friday’s activity resulted in a test of the base of a 3.5-month range at the 129.00 handle. This key support remains intact for now. A hammer candle formation on Jul 25 followed by a bullish engulfing candle yesterday signals a potential reversal.Initial resistance to watch is 129.95, the 20-day EMA. A break of the Jul 25 low is required to confirm a resumption of the bear trend.

- Gilt futures continue to trade below the Jul 22 high and the contract remains above its recent lows. A rally early last week resulted in a break of the 20-day EMA. A resumption of gains would signal scope for a climb towards 92.42 next, a 50.0% retracement of the Jul 1 - 18 bear leg. On the downside, key support and the bear trigger has been defined at 91.08, the Jul 18 low. Clearance of this level would resume the bear cycle that started Jul 1.

SONIA OPTIONS: More Upside Call spreads

Jul-29 11:16

SFIH6 96.75/96.90cs, bought for 2.25 in 8.88k.

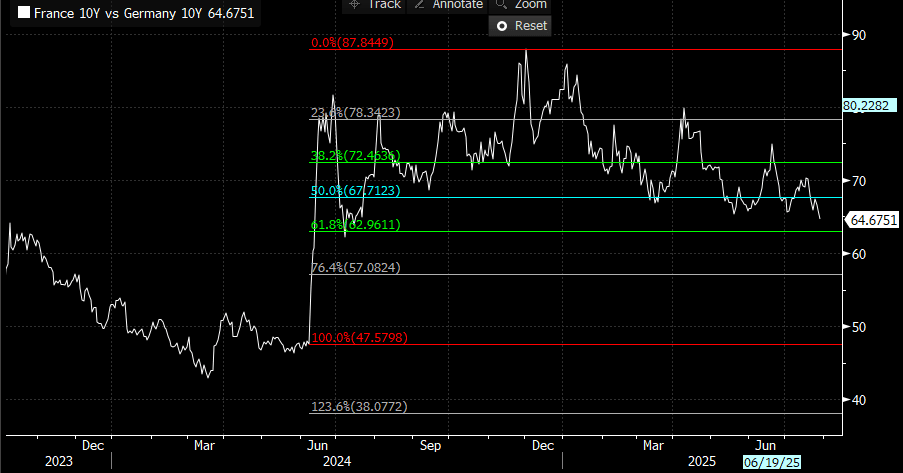

BONDS: OAT/Bund spread lowest in over a Year

Jul-29 11:05

- The OAT/Bund spread follows the BTP/Bund, and now test its tightest level in just over a Year, since the 15th July 2024.

- Next immediate support area is seen at ~63.00bps, the 61.8% retracement of Macron's sudden snap election announcement in June 2024.

(Chart source: MNI/Bloomberg).

Trending Top

Feb-06 09:27

Feb-06 09:20