IRAN: Markets Little Changed Despite Tehran's Hardline Position on Hormuz

"*IRAN SAID TO STICK TO HARDLINE POSITION ON STRAIT OF HORMUZ" - bbg Highlights: * Iranian officia...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LOOK AHEAD: Thursday Data Calendar:Wkly Claims, Trade Bal, Home Sales, Fed Speak

- US Data/Speaker Calendar (prior, estimate). All times ET

- 02/19 0820 Atlanta Fed Bostic opening remarks banking outlook conf

- 02/19 0830 Fed VC Bowman open remarks banking conf

- 02/19 0830 Initial Jobless Claims (227k, 225k), Continuing Claims (1.862M, 1.860M)

- 02/19 0830 Imports MoM (5%, 0.1%), Exports MoM (-3.6%, 0.1%)

- 02/19 0830 Trade Balance (-$56.8B, -$55.5B)

- 02/19 0830 Advance Goods Trade Balance (-$84.7B rev, -$86.0B)

- 02/19 0830 Wholesale Inventories MoM (0.2%, 0.2%), Retail MoM (0.2% est)

- 02/19 0830 Philadelphia Fed Business Outlook (12.6, 7.8)

- 02/19 0900 MN Fed Kashkari fireside chat economic outlook

- 02/19 1000 Pending Home Sales MoM (-9.3%, 2.0%), YoY (-1.3%, 3.0%)

- 02/19 1030 Chicago Fed Goolsbee opening remarks financial crisis conf

- 02/18 1130 US Tsy $105B 4W & $95B 8W bill auctions

- 02/18 1300 US Tsy $9B 30Y TIPS auction (912810US5)

- 02/19 1430 Chicago Fed Goolsbee moderated discussion

- Source: Bloomberg Finance L.P. / MNI

FED: Analysts Eye FOMC Reinforcing Shift Toward Greater Patience (3/3)

Some sell-side outlooks for the January minutes release:

- BMO FICC: “the meeting notes stand to offer a more refined sense of the balance of opinions on the Committee. Recall that the most notable change in the policy statement was the removal of the language: "downside risks to employment rose in recent months." Moreover, at the press conference, Powell said, "many of my colleagues think, it's hard to look at the incoming data and say that policy's significantly restrictive at this time." It's with this context that we expect the Minutes to reinforce the sense that the Fed has little urgency to deliver further rate cuts.”

- Citi: “minutes are likely to reflect a number of Fed officials reading the labor market as more stable based on the data that was available ahead of the meeting. Some more hawkish Fed officials likely expressed that in their base case policy rates could remain on hold for some time. But we expect the majority of officials still viewed further cuts as appropriate at some point this year even though they are comfortable with keeping policy rates unchanged in the near term.”

- Deutsche: “We will continue to look for indications about how divided the Committee is on the policy path in 2026.”

- ING: “could be more interesting since the Fed displayed a more hawkish tinge. The minutes could reveal to what extent this was more aimed at stemming the dollar weakness at that point in time."

- MUFG: "The statement referred to “some signs of stabilization” in the unemployment rate so we should see signs of some optimism that suggests the FOMC is content for now with maintaining a level of moderate restrictiveness. We don’t expect any surprises and see limited market impact."

- Scotia: "likely to reiterate that policymakers feel rates are in a “good spot” now, allowing them time to assess economic developments."

- TD: "could help gain some clarity on the division of the committee's thinking, though recent inflation and jobs data have likely made the minutes stale"

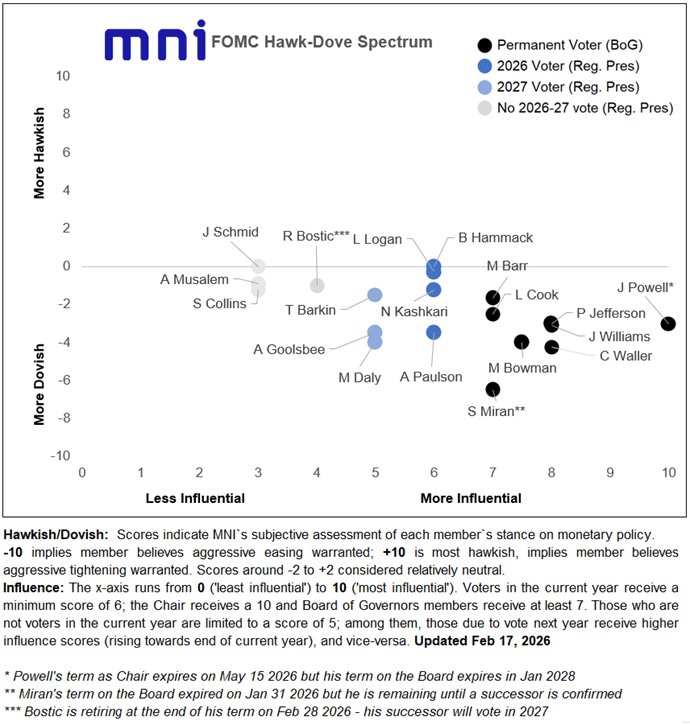

FED: Inter-Meeting FOMC Commentary Reflects Increasingly Patient Stance (2/3)

Divisions remain on the FOMC on the path forward but overall opinion has coalesced around a lack of urgency to cut rates again. Since the January meeting we’ve heard from most Committee participants, and of those, all have sounded at least as patient on future rate cuts as they did last month. In other words, if there has been any shift it has been in a more hawkish direction.

- Our Hawk-Dove Spectrum has been updated accordingly since the January meeting, with a shift across the Committee away from cut-leaning and toward a more neutral stance. Several have noted that downside risks to the labor market appear to have moderated, and that further evidence that inflation is converging to 2% will be required to support a resumption of easing.

In terms of the 12 voters in 2026, we’ve heard from 8 since the January FOMC meeting. Some key quotes, starting from 6 of the 8 Permanent FOMC voters (we haven’t heard from Powell or Williams since the meeting):

- Barr: “I would like to see evidence that goods price inflation is sustainably retreating before considering reducing the policy rate further, provided labor market conditions remain stable…Based on current conditions and the data in hand, it will likely be appropriate to hold rates steady for some time as we assess incoming data, the evolving outlook, and the balance of risks."

- Bowman: "“Since I see the current policy stance as moderately restrictive, I do think there’s room for at least 75bp of more cuts in 2026 "

- Cook: "At this time, I see risks as tilted toward higher inflation. As a result, I supported the FOMC's decision to hold the policy rate steady at our meeting last week. As I described, there is an argument for being optimistic about the path of inflation, but, until I see stronger evidence that inflation is moving sustainably back down to target, that is where my focus will be, in the absence of unexpected changes in the labor market"

- Jefferson: “The current policy stance is well positioned to address the risks to both sides of our dual mandate. I believe that the extent and timing of additional adjustments to our policy rate should be based on the incoming data, the evolving outlook, and the balance of risks."

- Miran: “I still think we need to cut interest rates substantially further from here. However, given that we’ve made some progress reducing rates, we can now proceed at a slower pace of a quarter-point per meeting.”

- Waller: "monetary policy is still restricting economic activity, and economic data make it clear to me further easing is needed ... [to closer to "neutral"] "which the median FOMC participant estimates is 3 percent, and not where we are—50 to 75 basis points above 3 percent."

Of the 4 regional presidents voting in 2026, we've only heard from two since January, and they are hawks: Hammack and Logan. We haven't heard from Kashkari or Paulson on monetary policy since the meeting, though the last we heard from them they were respectively hawkish/dovish on the 2026 rate outlook.

- Hammack: "I believe monetary policy is in a good place to stay on hold as we assess the incoming data and weigh if, and how, policy may need to adjust further... Based on my forecast, we could be on hold for quite some time."

- Logan: "We will learn in coming months whether inflation is coming down to our target and whether the labor market will remain stable. If so, this would tell me that our current policy stance is appropriate and no further rate cuts are needed to achieve our dual mandate goals. If instead we see inflation coming down but with further material cooling in the labor market, cutting rates again could become appropriate. But right now, I am more worried about inflation remaining stubbornly high. Fortunately, our policy is well-positioned to respond to risks to either of the FOMC’s dual mandate objectives."